Aug 2013 SA155 Short-Term Forecast of the Japanese Economy

(2013/7-9—2015/1-3)

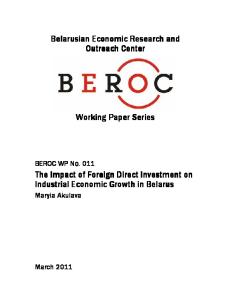

Be Prepared for Zero Growth in FY 2014 - “Good inflation” will take time - The government needs to press ahead with plans to increase the consumption tax rate Nobuyasu Atago Chief Forecaster, Japan Center for Economic Research •High growth expected for FY 2013, with exports and domestic demand both solid •Tax hike and high prices may affect consumption more than anticipated •Postponing the consumption tax hike will lose market confidence Gross domestic product grew by an annualized rate of 2.6% during the April–June period, continuing positive growth from the previous quarter. This suggests that the Japanese economy is recovering well, but these figures do not fully reflect the effects of the supplementary budget for fiscal 2012 (April 2012 to March 2013) or the last-minute demand in housing construction prompted by the impending consumption tax hike in April next year. Although these factors will continue to push up growth in the July– September quarter and beyond, what happens after the consumption tax rate increases in fiscal 2014 remains to be seen. Our forecast is that the Japanese economy will continue to expand at an annual rate of over 3% in the immediate term, and we expect GDP to grow by 2.7% in fiscal 2013, owing to three factors: (1) recovering external demand, (2) the boost received from the fiscal 2012 supplementary budget, and (3) last-minute demand before the consumption tax hike. However, we expect this to slow to around 0.2% in fiscal 2014 as the rebound from factors (2) and (3) leads to almost zero growth. 【Forecast of Real GDP Growth Rate and Its Breakdown】 3.0

q/q % chg.; Contributions to changes in real GDP Forecast

2.0 1.0 0.0 -1.0 -2.0 -3.0

Net Exports Public Demand Private Demand Ex. Influence of consumption tax rate rise Real GDP 2011:2 11:3 11:4 12:1 12:2 12:3 12:4 13:1 Source: Cabinet Office, "National Accounts"

Quarterly 13:2

13:3

13:4

14:1

14:2

14:3

14:4

15:1

http://www.jcer.or.jp/

-1-

Japan Center for Economic Research Aug 2013

The 155th Quarterly Forecast of the Japanese Economy

This forecast does not consider a supplementary budget for the current fiscal year. Some researchers are predicting higher growth for fiscal 2014 in the expectation that a supplementary budget will be passed in fiscal 2013. Market predictions average 0.6%, apparently higher than ours. However, if a supplementary budget on a similar scale to fiscal 2012 is passed, we will revise our forecast up by around 0.6%. Accordingly, our forecast is not substantially different from market predictions. The details of the forecast are as follows. The international economy, so crucial for Japanese exports, is expected to continue its steady recovery. This recovery will be led by the United States. Real GDP growth has been stagnant since the second half of last year because of austerity policies, but consumption is holding steady. Sales of new cars have returned to levels last seen in early 2008. The housing market is also showing clear signs of growth. We expect the real GDP growth rate to strengthen to between 2.5% and 3%. There are also indications that the slump in Europe has bottomed out. Real GDP in the Eurozone increased during the April–June period. This was the first increase for seven quarters. Concerns remain over the political situation in southern European countries, but we nevertheless expect a return to positive growth in 2014. In China, on the other hand, there is an increasing risk of an economic downturn. The authorities are concerned about the risk of a bubble caused by shadow banking system, and their priority is now to bring an inflated money supply down to an appropriate level rather than to encourage further growth. Real growth is likely to slow to a rate somewhere between 7.0% and 7.5%. In the currency markets, we expect the tendency toward a slightly cheaper yen to continue. Japan will continue its program of qualitative and quantitative easing, while in the United States the third round of quantitative easing (QE3) will be reduced in size in the near future, perhaps as early as this year. The gap between US and Japanese interest rates is likely to widen. Based on this, exports should continue their modest increase. But it is domestic demand that will play the most important role in determining economic developments from now on. First, we expect an increase and recovery in stagnant capital spending. Corporate earnings should improve thanks to a cheaper yen, and ordinary profits for listed companies are expected to be up by around 25% for fiscal 2013. The climate for capital investment is improving too. The diffusion index provided in the Tankan (Short-term Economic Survey of Enterprises in Japan) issued by the Bank of Japan for June describes the production capacity of large non-manufacturing enterprises as “insufficient.”

http://www.jcer.or.jp/

-2-

Japan Center for Economic Research Aug 2013

The 155th Quarterly Forecast of the Japanese Economy

There should also be a considerable increase in consumption and investment in housing as a result of last-minute demand before the consumption tax rate goes up. This surge in demand will lift consumption’s contributions to real GDP growth for fiscal 2013 by 0.5% and housing investments by 0.2%. The fiscal 2012 supplementary budget will also contribute a boost of around 0.6%. However, a rebound in fiscal 2014 will shrink real growth by around 1% for consumption and housing investment; the rebound from the effects of the supplementary budget will shrink growth by a further 0.3%.

14 12 10 8 6 4 2 0 -2

【Fig.1 Household Savings Rate】

(%)

Forecast

Fiscal Year 94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

Note: Household Savings Rate=(1-(Final consumption expenditure of households/Net nominal disposable income)×100 Source: Cabinet Office, "National Accounts", "Quarterly Estimates of GDP"

13

14

The consumer price index core (excluding fresh food products) looks set to increase in fiscal 2013, but it is expected to be stagnant at 0.5% in fiscal 2014, discounting the effect of the consumption tax hike. As Figure 1 shows, when consumer prices grew by around 2% annually in the past, inflation was similar across all categories and consumer prices increased across the board. Recent price increases, by contrast, have been tilted to energy. “Electricity charges” in the “fuel, light, and water” category and “gasoline” in the “transportation and communication” category are the main areas where prices have gone up. A cycle of “good inflation” driven by “a virtuous cycle of production, income, and spending” is still some time away. There is a risk of a further downturn in fiscal 2014. Our estimates of the likely effect of last-minute demand, the rebound effect, and subsequent recovery are calculated based on the previous hike in the consumption tax rate in April 1997. But household budgets and income patterns are quite different today. The proportion of both low-income households and elderly households has increased, and household savings are practically zero. We are transitioning to a stage in which household consumption eats into people’s assets. (See Fig. 2.) Temporary employment now makes up a large proportion of the job market, and wage increases are harder to achieve. These factors mean that household budgets are tight and there is little cash to spare. If real disposable income or actual net assets shrink as a result of the consumption tax rate increase or higher prices, there is a possibility that the negative impact on consumption will be more severe than anticipated.

http://www.jcer.or.jp/

-3-

Japan Center for Economic Research Aug 2013

The 155th Quarterly Forecast of the Japanese Economy

Despite this, the government should not postpone the consumption tax increase. Long-term interest rates have been kept low in spite of huge government debts because the markets take the view that the government still has options available for restoring fiscal health, including room to increase the consumption tax rate. If the government goes back on its previous decision and postpones the tax hike, the markets will lose confidence and questions will be raised about the government’s decisiveness and ability to collect taxes. Some people have proposed increasing the tax rate to 10% in annual 1% increments. In purely logical terms, this proposal is not without merit. This would have the effect of reducing the impact of last-minute demand and the subsequent rebound on consumer non-durables. A surge in demand is already being seen in housing, and for expensive consumer durables the real growth rate for fiscal 2013 would hardly be affected, since people are already shopping with the 10% rate in mind. But the rebound in fiscal 2014 would be eased by around 0.2%. Realistically, however, the impact on the government’s credibility and the administrative costs involved make it impractical to suddenly change the details of the proposed tax rate increase.

Another important factor is the growing significance of assets in household budgets. There is also the example of the United States, where consumer spending budgets have been unaffected by the scrapping of payroll tax breaks thanks to a buoyant stock market. The government needs to win the confidence and support of the market by showing that it is committed to its growth strategy and restoring the country to fiscal health.

http://www.jcer.or.jp/

-4-

Japan Center for Economic Research Aug 2013

The 155th Quarterly Forecast of the Japanese Economy

Fig 2. The Outlook for Japan's Economy Forecast FY2012 1st Qtr Real gross domestic expenditures (qtr.-to-qtr.)

FY2013 2nd

3rd

4th

1st Qtr

FY2014 2nd

3rd

4th

1st Qtr

2nd

3rd

4th

-0.2

-0.9

0.3

0.9

0.6

0.8

0.9

1.2

-2.1

0.5

0.5

0.2

Real gross domestic expenditures (year-on-year)

3.8

0.3

0.4

0.3

0.9

2.7

3.4

3.7

0.9

0.6

0.1

-0.9

Private final consumption (qtr.-to-qtr.)

0.1

-0.4

0.5

0.8

0.8

0.0

0.1

2.0

-3.8

1.2

1.0

Private housing investment (qtr.-to-qtr.)

2.1

1.6

3.6

1.9

-0.2

5.6

4.0

-0.3

-7.4

-6.2

-0.3

-3.2

-1.4

-0.2

-0.1

2.3

1.9

1.5

0.2

Public fixed capital formation (qtr.-to-qtr.)

5.1

3.5

3.0

1.1

1.8

3.5

1.0

-0.5

Domestic demand (contribution)

0.0

-0.2

0.3

0.5

0.5

0.8

0.8

Net exports of goods and services (contribution)

-0.2

-0.7

-0.1

0.4

0.2

0.0

Exports of goods and services (qtr.-to-qtr.)

-0.2

-4.5

-2.7

4.0

3.0

Imports of goods and services (qtr.-to-qtr.)

1.3

-0.0

-2.0

1.0

Nominal gross domestic expenditures (qtr.-to-qtr.)

-0.8

-0.9

0.1

Indices of Industrial Production (qtr.-to-qtr.)

-2.2

-3.2

4.4

FY2011

FY2012

FY2013

FY2014

Actual

Actual

Forecast

Forecast

0.3

1.2

2.7

0.2

0.3

1.6

1.6

2.2

-0.8

-4.7

3.8

3.7

5.3

9.7

-10.3

0.4

0.5

0.5

4.1

-1.4

1.3

3.6

-4.5

-4.0

-3.5

-3.0

-2.2

15.0

8.2

-8.7

1.2

-2.4

0.3

0.3

0.1

1.3

2.0

2.2

-0.5

0.1

0.1

0.3

0.2

0.2

0.1

-1.0

-0.8

0.4

0.6

1.5

1.8

1.4

1.3

1.5

1.5

1.5

-1.6

-1.2

5.8

6.0

1.5

1.7

1.2

1.2

-0.6

0.5

0.6

1.4

5.3

3.8

3.5

2.3

0.6

0.7

0.4

0.6

1.1

-0.8

0.5

0.3

0.4

-1.4

0.3

1.9

1.1

-1.9

0.6

1.5

2.1

1.0

1.8

-2.1

0.9

0.7

0.6

-0.7

-2.9

2.7

1.4

4.3

4.2

4.2

4.0

4.0

3.9

3.9

3.9

3.9

3.9

3.9

4.5

4.3

4.0

3.9

-0.4

0.1

-0.7

-0.0

0.9

0.7

0.8

0.4

0.3

0.2

0.3

0.3

0.6

-0.3

0.7

0.3

Newly issued government bonds yield 10-years (%)

0.879

0.789

0.749

0.702

0.731

0.807

0.861

0.915

0.969

1.004

1.039

1.073

1.049

0.781

0.829

1.021

Nikkei Stock Average (yen)

9,026

8,886

9,209 11,458 13,629 14,245 14,660 14,877 14,145 14,872 15,161 15,421

9,183

9,612

14,353

14,900

Yen : Dollar exchange rate (yen / dollar)

80.1

78.6

81.0

92.4

98.8

99.8

100.3

100.7

101.1

102.3

102.9

103.6

79.0

82.9

99.9

102.5

WTI Crude oil price (dollar / barrel)

93.4

92.2

88.2

94.4

94.2

100.0

97.7

96.5

95.2

94.3

93.5

93.0

97.2

92.0

97.1

94.0

Domestic corporate goods price index (year-on-year)

-1.1

-2.0

-0.9

-0.3

0.6

2.5

3.2

2.7

5.1

3.9

3.4

3.2

1.4

-1.1

2.2

3.9

Consumer price index (excluding fresh food ; year-on-year)

0.0

-0.2

-0.1

-0.3

0.0

0.5

0.5

0.7

2.8

2.6

2.6

2.6

0.0

-0.2

0.4

2.6

Current account / Nominal GDP (%)

1.3

0.8

0.9

0.7

1.8

1.0

0.9

1.0

1.6

1.7

1.7

1.7

1.6

0.9

1.3

1.9

Real GDP of U.S.A. (qtr.-to-qtr.)

1.2

2.8

0.1

1.1

1.7

2.4

2.6

2.3

2.9

3.0

2.9

3.0

Private non-residential investment (qtr.-to-qtr.)

Unemployment rate (%) Compensation of employees (year-on-year)

1.8 (C.Y.)

Real GDP of China (year-on-year)

7.6

7.4

7.9

7.7

7.5

7.2

7.2

7.3

7.3

7.4

7.4

7.4

9.3 (C.Y.)

2.8 (C.Y.)

7.8 (C.Y.)

1.5 (C.Y.)

7.4 (C.Y.)

2.6 (C.Y.)

7.3 (C.Y.)

[Notes] 1. Figures are shown in percentage change, and contribution means contribution to real GDP growth. 2. Figures for GDP components are at chained (2005) yen. 3. Figures for domestic corporate goods price index and consumer price index are at 2010 year basis. 4. Figures for indices of industrial production are at 2005 year basis. 5. Figures for GDP components, Compensation of employees, unemployment rate, indices of industrial production and current account are seasonally adjusted. 6. Figures for real GDP of U.S.A. are seasonally adjusted annual rate, at chained (2005) dollars. 7. Japan's fiscal year is April 1 to March 31. 8. Figures for Long-term interest rate, Stock price, Oil price, Exchange rate, and Unemployment rate are shown in average term for corresponding period.

Copyright (c) Japan Center for Economic Research. All Rights Reserved

http://www.jcer.or.jp/

-5-