150 140 130 120 110 100 90 80 70 60 50

Iron and Steel

Mining and manufacturing

150 140 130 120 110 100 90 80 70 60 50

General-purpose, production and business oriented machinery

Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

Import penetration rate Production

Production capacity

150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity

150 140 130 120 110 100 90 80 70 60 50

150 140 130 120 110 100 90 80 Import penetration rate 70 Production 60 Production capacity URL of the 50

Ceramics, stone and clay products

Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

Electric machinery

150 140 130 120 110 100 90 80 70 60 50

2007 2008 2009 2010 2011 2012 2013 (Year)

Transport equipment

Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

Electronic parts and devices

2007 2008 2009 2010 2011 2012 2013 (Year)

150 140 130 120 110 100 90 80 70 60 50

150 140 130 120 110 100 90 80 70 60 50

Fabricated metals

Trends of the import penetration rate, and the indices of production and production capacity by industry sector and goods Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

150 140 130 120 110 100 90 80 70 60 50

Non-ferrous metals

150 140 130 120 110 100 90 80 Import penetration rate 70 Production 60 capacity Analysis ofProduction All Industrial Activities :50

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

Chemicals

240 230 220 210 200 190 180 170 160 150 140 130 120 110 100 90 80 70 60 50

Information and communication electronics equipment Import penetration rate Production Production capacity

Released on November 27, 2014 Economic Analysis Office Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year) 2007 2008 2009 2010 2011 2012 2013 (Year) 2007 2008 2009 2010 2011 2012 2013 (Year)(ENGLISH) http://www.meti.go.jp/english/statistics/bunseki/index.html

(JAPANESE) http://www.meti.go.jp/statistics/toppage/report/bunseki/index.html

2007 2008 2009 2010 2011 2012 2013 (Year)

• Japan’s import penetration rate (the percentage of imports to the overall supply from mining and manufacturing, on a quantity base) is continuing an upward trend. • Although the yen has substantially depreciated since 2012, there is no sign of turnover of the import penetration rate. • Are these tendencies commonly observed in all industry sectors of manufacturing industry in Japan? Or do they differ depending on the industry sector or the type of goods? * In this report, “the indices of industrial production” and “the indices of production capacity of manufacturing industry” are shortened to “production” and “production capacity” respectively. 1

• We will look at the trends of the import penetration rate from 2007, before the Lehman crisis, to 2013. • We will check the trends of the import penetration rate, and the indices of production and production capacity, and sort them by industry sector and the type of goods. • We will focus on the industry sectors which showed characteristic changes, and closely look at their trends.

2

Trends of the import penetration rate (1) • •

During 2007 to 2013, the import penetration rate shifted upward. After 2011, imports have been increasing while domestic production and the overall supply have been stagnating. Changes in the Import Penetration Ratio, and Overall Supply, Domestic Production, and Imports (%) 24

(2010 = 100) 120 Import Penetration Rate

Overall supply Domestic production Imports

115

23

110 105

22

100 21

95 90

20

85 80

19 2007

2008

2009

2010

2011

2012

2013 (Year)

2007

2008

2009

2010

2011

2012

2013 (Year)

(Note) 1. Of the weighting of 10041.61 for the overall supply from mining and manufacturing, domestic production comprises 7938.44, and imports comprise 2103.17. 2. Import penetration rate = (Import index × Import weight) / (Overall supply index × Overall supply weight) × 100 3. The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”. 3

Trends of the import penetration rate (2) • •

When analyzing factors of changes in the import penetration rate from the previous year, the “factor of increase in imports” contributed in a positive way from 2010. Although the “factor of decrease in domestic production” reversed its direction of contribution, the degree of contribution was reduced. Factorial Analysis of the Import Penetration Rate (Compared to the previous year)

(Compared to the previous year, %, % points) 0.3 Imports: Increase Domestic production: 0.2 Decrease

Factor of decrease in domestic production Factor of increase in imports Import penetration rate

0.1 0.0 -0.1 Imports: Decrease Domestic production: Increase

-0.2 2008

2009

2010

2011

(Note) The 2008 figures, changes from the previous year, are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

2012

2013 (Year) 4

Trends of the import penetration rate (3) Goods that contributed to increase in imports (on a quantity basis) from 2010 2010 12.4%change from the previous year Type of goods Contribution ratio to imports

Items that contributed to increase

2011 5.7% change from the previous year

(3)

(1)

Capital goods

Construction goods

Durable consumer goods

1.62% points (3)

0.17% points

1.37% points

Semiconductor products machinery, Notebook computers, Analytical instruments, Steel ship

Lumber, Pipe fittings (made of steel pipes and tubes), Ordinary plywood, System kitchens

Flat-screen television, Cellular telephone, Small passenger cars, Notebook computers

(2)

Type of goods

Capital goods

Construction goods

Durable consumer goods

Contribution ratio to imports

1.09% points

0.31% points

1.29% points

Items that contributed to increase

2012 3.7% change from the previous year

Notebook computers, Semiconductor products machinery, Desktop computers, Radiation instruments

Lumber, Pipe fittings (made of steel pipes and tubes), Structural steel frames, Fluorescent luminaries

Cellular telephone, Notebook computers, Flatscreen television, Large passenger cars

(3)

Type of goods

Capital goods

Construction goods

Durable consumer goods

0.68% points

0.01% points

0.15% points

2013 3.0% change from the previous year

Notebook computers, Lumber, Fluorescent Degital transmission luminaries, Tiles, Ordinary equipment, Large passenger hot-steel pipes and tubes cars, Steel ship

(1)

(3)

Construction goods

Durable consumer goods

Contribution ratio to imports

1.33% points

0.16% points

0.53% points

Water closet, Alminum exterior, Asphalt, Gypsum board

Notbook computers, Cellular telephone, Large passenger cars, Electric vacuum machines

Mining 2.30% points (2)

(1)

Non-durable consumer goods Producer goods (excl. mining)

1.14% points Drugs and medicines, Woven fabrics outwears, Cigarettes, Fish paste products

2.06% points Refined sugar, Internal conbustion engines for industry, Benzene, pure, Sodium hydroxide

0.81% points

Mining 0.21% points

Natural Gas

(1)

Non-durable consumer goods Producer goods (excl. mining)

(3)

Capital goods

Notbook computers, Analytical instruments, Desktop computers, Power conversion equipment

5.80% points (1)

(2)

Electrolytic silver, MOS Ics Drugs and medicines, (Logic), MOS Ics (Memory), Coal, Natural gas, Crude oil, Leather boots and shoes, Switching power supply Limestone Sausage, Fish paste products units

Cellular telephone, Notebook computers, Large Drugs and medicines, passenger cars, Video Sausage, Ham, Cheese camera

Type of goods

Items that contributed to increase

0.92% points

(2)

Contribution ratio to imports

Items that contributed to increase

Non-durable consumer goods Producer goods (excl. mining)

0.65% points

Mining 1.11% points

High speed steel cutting Natural gas, Crude oil, tools, Photo film, Diamond Limestone tools, Terephtalic acid, pure

(2) Non-durable consumer goods Producer goods (excl. mining)

0.44% points Drugs and medicines, Knitted fabrics outwear, Woven fabrics outwear, Leather boots and shoes

0.69% points MOS Ics (Logic), Drive, transmission and control parts, Benzene, pure, Electrolytic silver

Mining -0.10% points

Natural gas, Limestone

(Note) 1. The numbers (1) - (3) are placed in the descending order of the contribution rate by goods. 2. Notebook computers and large passenger cars are purchased by both households and corporations, so they are classified as durable consumer goods when purchased by a household, and capital goods when purchased by a corporation. Source: Created based on “ METI: Indices of Industrial Domestic Shipments and Imports”

5

Trends of the import penetration rate by industry sector and goods (1) • • •

During 2007 to 2013, the import penetration rate for many industry sectors and goods increased. The increased width of Information and communication electronics equipment industry was great, recording 48.7% in 2013, which was close to the level of Textiles industry. The level of the import penetration rate varies significantly depending on industry sector and the type of goods. Changes in the Import Penetration Rate by Industry Sector and Goods Industry Textiles Information and communication electronics equipment

Non-ferrous metals Mining and manufacturing (overall)

Chemicals Electronic parts and devices Electrical machinery Petroleum and coal products General-purpose, production and business oriented m achinery

Ceramics, stone and clay products Fabricated metals Pulp, paper and paper products Plastic products Iron and Steel Transport equipment

2007 46.6 21.1 29.2 19.7 19.3 23.8 16.9 14.4 11.5 8.5 7.5 6.1 5.3 5.5 5.1

2008 48.4 23.4 33.6 20.1 18.4 22.6 16.8 14.3 11.6 8.9 7.2 6.1 5.4 5.2 4.7

2009 52.1 25.4 27.6 21.0 17.6 22.0 17.1 13.7 13.2 8.6 6.5 7.4 6.0 4.6 4.2

2010 51.1 28.3 31.5 20.9 17.1 22.3 15.9 14.5 12.4 8.8 7.7 7.4 6.6 5.4 4.5

2011 53.2 35.6 30.5 22.7 19.9 20.2 16.7 16.6 13.5 9.8 9.0 8.4 7.4 6.5 5.1

2012 53.5 41.1 30.4 22.9 21.3 19.3 16.8 17.2 15.2 9.0 8.9 8.6 7.3 6.4 5.2

(%)

2013 54.4 48.7 36.3 23.6 21.6 20.0 17.6 16.8 14.9 10.3 9.0 8.0 7.5 6.2 5.9

High

Low

(%) Goods Producer goods Non-durable consumer goods Industrial production (ove rall) Durable consumer goods Capital goods Construction goods

2007 26.7 20.8 19.7 9.3 10.2 8.0

2008 27.6 20.3 20.1 9.2 10.1 7.7

2009 28.2 20.6 21.0 11.4 11.1 7.5

2010 27.4 21.6 20.9 11.5 11.4 8.3

2011 29.0 23.3 22.7 14.9 12.5 9.5

2012 29.2 24.1 22.9 14.4 13.1 9.3

2013 29.5 24.7 23.6 15.7 15.1 9.5

High

Low

(Note) 1. The lists are arranged in descending order of the import penetration rate in 2013. 2. Gradation color shows the degree of the import penetration rate for each industry sector and goods, from the highest to the lowest. 3. The 2007 figures are the estimated values. 6 Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

Trends of the import penetration rate by industry sector and goods (2) Changes in the Import Penetration Rate by Industry Sector (%) 60

Textiles Information and communication electronics equipment Non-ferrous metals

50

Mining and manufacturing (overall) Chemicals 40

Electronic parts and devices Electrical machinery Petroleum and coal products

30

General-purpose, production and business oriented machinery Ceramics, stone and clay products

20

Fabricated metals Pulp, paper and paper products 10

Plastic products Iron and steel Transport equipment

0 2007

2008

2009

2010

2011

2012

2013 (Year)

(Note) The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

7

Trends of the import penetration rate by industry sector and goods (3) •

•

When comparing two points of time, 2007 with 2013, the largest increase in the import penetration rate was observed in Information and communication electronics equipment industry in the category of industry sector and Durable consumer goods in the category of goods. Electronic parts and devices industry alone experienced a decrease in the import penetration rate. Variation Width of the Import Penetration Rate in 2007 → 2013 (% points) Industry Information and communication electronics equipment

Texitles Non-ferrous metals Mining and manufacturing (overall) General-purpose and business oriented machinery

Petroleum and coal products Chemicals Plastic products Pulp, paper and paper products Ceramics, stone and clay products Fabricated metals Transport equipment Electrical machinery Iron and steel Electronic parts and devices

2007→2013 (Difference in points)

Goods 27.6 7.8 7.1 3.9 3.4 2.4 2.3 2.2 1.9 1.8 1.5 0.8 0.7 0.7 -3.8

2007→2013 (Difference in points)

Durable consumer goods Capital goods Industrial production (overall)

Non-durable consumer goods

Producer goods Construction goods

6.4 4.9 3.9 3.9 2.8 1.5

(Note) 1. The lists are arranged in descending order of difference in points. 2. The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports” 8

Trends of production by industry sector and goods (1) •

When looking at the trends of production by industry sector and goods based on 2007 = 100, many industry sectors and types of goods including Mining and manufacturing (overall) experienced a significant decrease in 2009 after the Lehman crisis, and turned positive in 2010, while production has been stagnated since 2011. Changes in Production by Industry Sector and Goods (2007=100) Industry Chemicals Electrical machinery Petroleum and coal products Pulp, paper and paper products Plastic products Ceramics, stone and clay products Transport equipment Iron and steel Fabricated metals Mining and manufacturing (overall)

Electronic parts and devices Non-ferrous metals General-purpose, production and business oriented m achinery

Textiles Information and communication electronics equipment

2007 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

2008 96.8 97.1 98.1 98.8 96.3 93.7 98.5 96.5 99.3 96.6 94.3 94.4 91.0 90.5 93.6

2009 91.2 75.4 92.4 86.3 81.3 72.9 69.5 66.8 84.4 75.5 73.1 73.3 55.3 71.0 74.3

2010 96.9 88.9 92.7 90.1 89.1 86.4 85.5 87.0 85.9 87.3 94.5 85.3 72.7 75.6 82.4

2011 95.5 88.8 87.5 88.1 86.6 83.6 78.0 84.7 84.5 84.8 85.7 82.0 81.8 77.8 67.4

2012 93.4 87.3 87.2 86.7 87.6 84.1 87.1 84.9 85.7 85.3 82.4 83.8 77.4 75.9 63.6

2013 94.4 90.0 87.9 87.7 87.5 86.2 85.4 85.2 85.0 84.6 83.6 82.2 75.0 74.4 56.5

High

Low

(2007=100) Goods Non-durable consumer goods Producer goods Construction goods Industrial production (ove rall) Capital goods Durable consumer goods

2007 100.0 100.0 100.0 100.0 100.0 100.0

2008 101.1 95.9 96.3 96.6 93.4 96.8

2009 99.7 74.8 82.9 75.5 62.8 70.3

2010 100.3 89.5 81.4 87.3 76.3 83.8

2011 99.2 85.6 81.1 84.8 80.3 74.0

2012 99.9 85.9 83.1 85.3 78.5 78.4

2013 99.5 86.0 85.0 84.6 76.7 74.9

High

Low

(Note) 1. The lists are arranged in descending order of the indices of production in 2013. 2. Gradation color shows the degree of production of each industry sector and goods, from the highest to the lowest. 3. The figures of general-purpose, production and business oriented machinery industry in 2007 is the estimated values. Source: Created based on “METI: Indices of Industrial Production”

9

Trends of production by industry sector and goods (2) •

When comparing two points of time, 2007 with 2013, production of all industry sectors and types of goods decreased. Especially the largest decrease was observed in Information and communication electronics equipment industry in the category of industry sector, and Durable consumer goods and capital goods in the category of goods. Variation Width of Production in 2007 → 2013 (Points) Industry Chemicals Electrical machinery Petroleum and coal products Pulp, paper and paper products Plastic products Ceramics, stone and clay products Transport equipment Iron and steel Fabricated metals Mining and manufacturing (overall)

Electronic parts and devices Non-ferrous metals General-purpose, production and business oriented m achinery

Textiles Information and communication electronics equipment

2007→2013 (Difference in points) -5.6 -10.0 -12.1 -12.3 -12.5 -13.8 -14.6 -14.8 -15.0 -15.4 -16.4 -17.8 -25.0 -25.6 -43.5

Goods Non-durable consumer goods Producer goods Construction goods Industrial production (overall)

Capital goods Durable consumer goods

2007→2013 (Difference in points) -0.5 -14.0 -15.0 -15.4 -23.3 -25.1

(Note) 1. The lists are arranged in descending order of difference in points. 2. The figure of general-purpose, production and business oriented machinery industry in 2007 is the estimated values. Source: Created based on “METI: Indices of Industrial Production”

10

Trends of production capacity by industry sector (1) •

Looking at the trends of production capacity by industry sector based on 2007 = 100, many industry sectors including Manufacturing (overall) industry trended downward after peaking in 2007 or 2008. Changes in Production Capacity by Industry Sector (2007=100) Industry Electronic parts and devices Iron and steel Transport equipment Non-ferrous metals Chemicals Manufacturing (overall) General-purpose, production and business oriented machinery

Pulp, paper and paper products Electrical machinery Fabricated metals Petroleum and coal products Ceramics, stone and clay products Information and communication electronics equipment

Textiles

2007 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

2008 108.9 100.4 101.0 100.2 99.9 100.5 99.9 99.6 95.2 99.7 100.1 97.4 101.0 97.0

2009 112.5 101.6 99.7 99.5 99.1 98.9 93.7 97.1 93.7 98.2 99.6 96.5 98.7 90.2

2010 118.3 101.8 99.4 98.6 99.8 98.5 94.0 95.1 93.0 95.6 92.3 93.3 99.2 84.2

2011 120.7 101.9 99.5 98.6 98.6 98.4 96.3 94.5 91.7 93.2 91.9 92.3 97.4 81.8

2012 119.1 101.5 99.7 99.2 97.8 96.8 96.2 91.5 90.3 91.7 91.6 90.9 82.7 80.8

2013 119.7 101.5 99.1 98.3 98.0 95.8 92.7 91.4 90.8 90.6 88.8 88.8 78.4 77.9

(Note) 1. The list is arranged in descending order of production capacity in 2013. 2. The figures of general-purpose, production and business oriented machinery industry in 2007 is the estimated values. 3. Gradation color shows the degree of production capacity of each industry sector, from the highest to the lowest. Source: Created based on “METI: Indices of Industrial Production”

High

Low

11

Trends of production capacity by industry sector (2) •

•

When comparing two points of time, 2007 with 2013, the production capacity of many industry sectors decreased. Among them, the largest decrease was observed in Textiles industry and Information and communication electronics equipment industry. Meanwhile, the production capacity of Electronic parts and devices industry and Iron and steel industry increased. Variation Width of Production Capacity in 2007 → 2013 (Points) Industry Electronic parts and devices Iron and steel Transport equipment Non-ferrous metals Chemicals Manufacturing (overall) General-purpose, production and business oriented machinery

Pulp, paper and paper products Electrical machinery Fabricated metals Petroleum and coal products Ceramics, stone and clay products Information and communication electronics equipment

Textiles

2007→2013 (Difference in points) 19.7 1.5 -0.9 -1.7 -2.0 -4.2 -7.3 -8.6 -9.2 -9.4 -11.2 -11.2 -21.6 -22.1

(Note) 1. The list is arranged in descending order of difference in points. 2. The figure of general-purpose, production and business oriented machinery industry in 2007 is the estimated value. Source: Created based on “METI: Indices of Industrial Production”

12

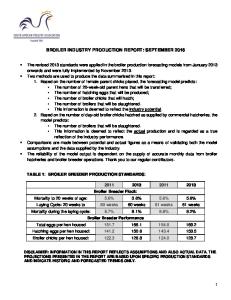

Trends of the import penetration rate, production, and production capacity by industry sector and goods (1) Changes in Import Penetration Rate, Production, Production Capacity by Industry Sector and Goods (2007 = 100) Mining and manufacturing

150 140 130 120 110 100 90 80 70 60 50

150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

General-purpose, production and business oriented machinery

Iron and Steel 150 140 130 120 110 100 90 80 70 60 50

Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity

150 140 130 120 110 100 90 80 70 60 50

2007 2008 2009 2010 2011 2012 2013 (Year)

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013

(Year)

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

Ceramics, stone and clay products

Import penetration rate Production Production capacity

150 140 130 120 110 100 90 80 70 60 50

2007 2008 2009 2010 2011 2012 2013 (Year)

2007 2008 2009 2010 2011 2012 2013 (Year)

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

Chemicals 150 140 130 120 110 100 90 80 70 60 50

2007 2008 2009 2010 2011 2012 2013 (Year)

Import penetration rate Production

Import penetration rate Production Production capacity

Fabricated metals 150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

Electric machinery 150 140 130 120 110 100 90 80 70 60 50

Plastic products

Petroleum and coal products 150 140 130 120 110 100 90 80 70 60 50

2007 2008 2009 2010 2011 2012 2013 (Year)

Electronic parts and devices

Import penetration rate

Transport equipment 150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity

Non-ferrous metals 150 140 130 120 110 100 90 80 70 60 50

150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

Pulp, paper and paper products

Import penetration rate Production Production capacity 2007 2008 2009 2010 2011 2012 2013 (Year)

240 230 220 210 200 190 180 170 160 150 140 130 120 110 100 90 80 70 60 50

Information and communication electronics equipment Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

Textiles 150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production Production capacity

2007 2008 2009 2010 2011 2012 2013 (Year)

13

Trends of the import penetration rate, production, and production capacity by industry sector and goods (2) Changes in Import Penetration Rate, Production, Production Capacity by Industry Sector and Goods (2007 = 100, continued from the previous slide) Capital goods 150 140 130 120 110 100 90 80 70 60 50

150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production 2007 2008 2009 2010 2011 2012 2013 (Year)

Non-durable consumer goods

Import penetration rate Production 2007 2008 2009 2010 2011 2012 2013 (Year)

Construction goods 150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production

Producer goods 150 140 130 120 110 100 90 80 70 60 50

Durable consumer goods

2007 2008 2009 2010 2011 2012 2013 (Year)

Import penetration rate Production 2007 2008 2009 2010 2011 2012 2013 (Year)

170 160 150 140 130 120 110 100 90 80 70 60 50

Import penetration rate Production 2007 2008 2009 2010 2011 2012 2013 (Year)

(Note)

1. The graphs for plastic products industry and each goods only show the import penetration rate and production because no figures are available on production capacity. 2. The figures of production and production capacity of general-purpose, production and business oriented machinery industry in 2007 are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports” and “Indices of Industrial Production”

• • • •

While production capacity of many industry sectors including the overall mining and manufacturing has been shifting downward, production has remained stagnant, and the import penetration rate has been slowly but steadily increasing. For Information and communication electronics equipment industry, the production and production capacity has significantly decreased, while the import penetration rate has greatly increased. For Electronic parts and device industry, the production has been stagnating, while the production capacity has increased and the import penetration rate has been decreased. The production of Durable consumer goods and Capital goods remains stagnant, while the import penetration rate has been substantially increased. 14

Trends of Information and communication electronics equipment industry (1) • •

•

The import penetration rate for Information and communication electronics equipment industry continued increasing from 2007 to 2013. Domestic production and the overall supply decreased in 2008 and 2009 after the Lehman crisis occurred, but they increased in 2010 due to the policy effect of the eco-point system for home appliances and lastminute demand in accordance with the transition to digital terrestrial transmission and other factors. Both of them decreased from 2011. Imports continued stagnant from 2007 to 2009, but increased from 2010.

(%) 50 45 40

Changes in the Import Penetration Rate, and the Overall Supply, Domestic Production, and Imports of “Information and Communication Electronics Equipment Industry” (2010=100) 160 Overall supply 140 Domestic production Import penetration rate Imports 120

35

100

30

80

25

60

20

40 2007

2008

2009

2010

2011

2012

2013 (Year)

2007

2008

2009

2010

2011

2012

2013 (Year)

(Note) 1. Of the weighting of 560.67 for the overall supply from information and communication electronics equipment industry, domestic production comprises 402.26 and imports comprises 158.41. 2. The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

15

Trends of Information and communication electronics equipment industry (2) •

When analyzing factors of changes in the import penetration rate for Information and communication electronics equipment industry from the previous year, the “factor of decrease in domestic production” exceeded the “factor of increase in imports” and contributed to the increase in the import penetration rate in all years except in 2010. Factorial Analysis of the Import Penetration Rate (Compared to the previous year) for “Information and Communication Electronics Equipment Industry” (Compared to the previous year, %, % points)

Imports: Increase Domestic production: Decrease

0.4

Factor of decrease in domestic production

0.3

Factor of increase in imports

0.2

Import penetration rate

0.1 0.0 -0.1 -0.2 Imports: Decrease Domestic production: Increase

2008

2009

2010

2011

2012

2013 (Year)

(Note) The 2008 figures, changes from the previous year, are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports” 16

Trends of Information and communication electronics equipment industry (3) •

•

When comparing two points of time, 2007 with 2013, the domestic production of Information and communication electronics equipment industry decreased by 45.3%. Items such as Cellular telephone, Flat panel television and Video camera contributed to the decrease in domestic production. Imports of Information and communication electronics equipment industry increased by 95.1%. Items such as Notebook computers, Cellular telephone and Desktop computers contributed to the increase in imports. “Information and Communication Electronics Equipment Industry” Contribution Ratio to Growth Rate by Item Domestically Produced or Imported (2007→ 2013) (1) Domestic production

(%, % points)

(%, % points) 0

-10

100 Cellular telephone

-20 -30 -40 -50

(2) Imports

Flat panel television Video camera Others Total of Information and communication elecctorinics equipment

Total of Information and communication electronics equipment industry

90

Others

80

Desktop computers

70 60

Cellular telephone

50 40 30 20

Notebook computers

10 0

(Note) 1. “Others” includes remaining 18 items after excluding top 3 items which contributed to the growth in domestic production and imports of Information and communication electronics equipment industry (2007→2013). 2. The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

17

Trends of Information and communication electronics equipment industry (4) •

When checking the trends of the domestic production of main items which contributed to the decrease in domestic production and the increase in imports based on 2007=100, in 2013, Desktop computers increased to 102.9, but decreases were observed in items such as Notebook computers (decreased to 77.0), Cellular telephone (decreased to 18.9), Flat panel television (decreased to 6.1), and Video cameras (decreased to 4.6). “Information and Communication Electronics Equipment Industry” Changes in Production Index by Item (2007 → 2013) (2007 = 100) 160 140

Flat panel televisions

120

Desktop computers 102.9

100

Notebook computers 77.0

80 60 40 20 0

Video camera

Cellular telephone 18.9 6.1 4.6

2007 2008 2009 2010 2011 2012 2013

(Year)

(Note) The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Production”

18

Trends of Electronic parts and devices industry (1) • •

The import penetration rate for Electronic parts and devices industry shifted downward from 2007 to 2012, while it increased in 2013. It was not necessarily that the domestic production had continued increasing, and the imports had kept decreasing. Changes in the Import Penetration Rate and the Overall Supply, Domestic Production, and Imports of “Electronic Parts and Devices Industry” (2007 = 100) 120

(%) 24

Overall supply Domestic production Imports

Import penetration rate

23

110

22

100

21 90

20

80

19

70

18 2007

2008

2009

2010

2011

2012

2013 (Year)

2007

2008

2009

2010

2011

2012

2013 (Year)

(Note) 1. Of weighting of 589.11 for the overall supply from electronic parts and devices industry, domestic production comprises 457.59 and imports comprises 132.52. 2. The 2007 figures are the estimated values. 19 Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

Trends of Electronic parts and devices industry (2) Factorial Analysis of the Import Penetration Rate (Compared to the previous year) for “Electronic Parts and Devices Industry” (Compared to the previous year, %, % points) Imports: Increase Domestic production: Decrease

0.2

Factor of decrease in domestic production Factor of increase in imports

0.1

Import penetration rate

0.3

0.0 -0.1 Imports: Decrease Domestic production: Increase

-0.2 -0.3 2008

2009

2010

2011

2012

2013 (Year)

(Note) The 2008 figures, changes from the previous year, are the estimated values. Source: Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

20

Trends of Electronic parts and devices industry (3) •

•

When comparing two points of time, 2007 with 2013, the domestic production of Electronic parts and devices industry increased by 0.3%. Items such as Metal oxide semiconductor ICs (Memory), Active matrix LCDs (middle and small) and Metal oxide semiconductor ICs (CCD) contributed to the increase in domestic production. Imports of Electronic parts and devices decreased by 19.8%. Items such as Magnetic tapes, Switching power supply units and Metal oxide semiconductor ICs (Memory) contributed to the decrease in imports. “Electronic Parts and Devices Industry” Contribution ratio to Growth Rate by Item Domestically Produced or Imported (2007 → 2013) (1) Domestic production (%, % points) 0

(%, % points) 20 15 10 5 0

(2) Imports

MOS ICs (CCD) Active matrix LCDs (Middle and small)

Magnetic tapes -5 Switching power supply units

MOS ICs (Memory) Total of electronic parts and devices industry

-10

-5 -10 -15 -20

Others

-15

-20

MOS ICs (Memory) Others

Total of electronic parts and devices industry

(Note) 1. “Others” includes remaining 21 items after excluding top 3 items which contributed to the growth in domestic production and imports of electric parts and devices industry. 2. The 2007 figures are the estimated values. Source:Created based on “METI: Indices of Industrial Domestic Shipments and Imports”

21

Trends in Electronic parts and devices industry (4) •

When checking the trends of the domestic production of main items which contributed to the increase in domestic production and the decrease in imports based on 2007=100, in 2013, significant increases were observed in items such as Metal oxide semiconductor ICs (Memory) (increased to 230.0), Active matrix LCDs (Middle and small) (increased to 167.6) and Metal oxide semiconductor ICs (CCD) (increased to 116.5). Meanwhile, Switching power supply units decreased to 79.9, and Magnetic tapes also decreased to 65.6. “Electronic Parts and Devices Industry” Changes in Production Index by Item (2007 → 2013) (2007=100) 240 220

Metal oxide semiconductor ICs (Memory)

230.0

200 180 160

Active matrix LCDs (Middle and small)

167.6

140 120 100 80 60

Metal oxide semiconductor ICs 116.5 (CCD) Switching power supply units

79.9 65.6

Magnetic tapes

2007 2008 2009 2010 2011 2012 2013 (Year) (Note) The 2007 figures are the estimated values. Source: Created based on “METI: Indices of Industrial Production”

22

• From 2007 to 2013, production capacity of many industry sectors including Mining and manufacturing (overall) has shifted downward, while production has remained stagnate and the import penetration rate has slowly but steadily increased. • In Information and communication electronics equipment industry, the production and production capacity substantially decreased, while the import penetration rate largely increased. The “factor of decrease in domestic production” exceeded the “factor of increase in imports” and contributed to the increase in the import penetration rate in all years except in 2010. • The coexistence of “significant contraction of production base” and “rapid expansion of dependence on import”, which occurred in Information and communication electronics equipment industry during 2007 to 2013, is considered a main reason that the import penetration rate has not turned over in spite of continued weak yen. 23

• Electronic parts and devices industry is the only industry which experienced reduction in the import penetration rate from 2007 to 2013. However, it was not necessarily that domestic production had continued increasing, and imports had kept deceasing during the period. • When comparing two points of time, 2007 with 2013, the production in Electronic parts and devices industry (overall) decreased by 16.4 points, while the production of smartphonerelated parts, such as Metal oxide semiconductor ICs (Memory), Active matrix LCDs (middle and small) and Metal oxide semiconductor ICs (CCD), greatly increased. The production capacity also increased. 24

• Japan’s import penetration rate shifted upward from 2007 to 2013. When analyzing factors of changes in the import penetration rate from previous year, the “factor of increase in imports” contributed in a positive way from 2010. The “factor of decrease in domestic production” reversed its direction of contribution, but the degree of contribution reduced. • Japan’s import penetration rate of the nearest third quarter of 2014 was 24.0%, further increased from 23.6% in 2013. We need to focus on the future trends of the import penetration rate.

25