National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

THE EFFECT OF FEDERAL, STATE AND LOCAL TAX RATES CAPITAL GAINS: NEW YORK STATE'S EXPERIENCE**

ON

FRANS SEASTRAND* Introduction

tax rates on capital gains. The assumption under federal tax reform was that the increase in tax rates on capital gains would raise additional revenue predominantly from high-income taxpayers to offset some of the benefits they would receive from lowering the maximum tax rate. The controversy stems from the discretionary nature of the tax on capital gains. Taxpayers may hold capital assets and defer the tax on any gains until the gains are realized through the sale of assets. Changes in tax rates are likely to affect the frequency or timing and amount of capital gains realizations. A growing number of studies have demonstrated that higher tax rates will encourage taxpayers to defer the realization of capital gains. The effect of higher tax rates on capital gains will reduce the after-tax rate of return on realized gains. This creates an inducement to defer the realization of capital gains and postpone the payment of an additional tax by locking in unrealized gains. The degree of taxpayer reaction to changes in capital gains tax rates has become the focal point of the controversy. If the behavioral effect is great enough, raising tax rates could actually lower revenue. On the other hand, if taxpayer responsiveness is weak, raising the tax rate could increase revenue. More recent studies have been preoccupied with estimating the tax rate on capital gains that will produce maximum revenue, including works by Lindsey (1986) and (1987) and CBO (1988). This issue has become prominent among federal policy analysts. The capital gains behavioral issue at the state level follows from federal/state tax linkages and conformity of many states to federal tax laws. For example, when states were struggling to respond to the federal tax reform changes, they had to try to estimate the size of the so-called revenue "windfall" they perceived they would receive because of conformity with federal

NE of the most controversial provi0 sions in the Tax Reform Act of 1986 was the elimination of the preferential treatment of long-term capital gains, leading to the greatest capital gains tax rate increase since the inception of the Internal Revenue Code of 1954. The end of the tax preference for capital gains in 1988 raised the weighted average marginal tax rate by 51 percent according to analysis related to a recent study by the Congressional Budge Office (CBO, 1988). As a result of this change, the taxation of capital gains is now being treated equally with ordinary income for the first time since 1921.1 The purpose of increasing the tax rate on capital gains was to raise revenue to finance the reduction in marginal tax rates on ordinary income, maintain equity and distributional neutrality and increase the simplicity of the tax system. Much of the concern about reform of the taxation of capital gains is over the impact of such a large rate increase on taxpayer behavior. The development of tax reform rested on a set of behavioral assumptions about how taxpayers would react to changes in individual provisions of the tax law. The behavioral assumptions surrounding capital gains tax reform were founded on past studies of taxpayer behavior. Subsequent to the enactment of the Tax Reform Act of 1986, considerable attention has been given.to the study of taxpayer reaction to an increase in capital gains tax rates and its impact on revenue. Following the enactment of federal tax reform, a controversy developed and intensified around the uncertainty of collecting additional revenue by increasing *New York State Department of Taxation and Finance, Albany, NY 12227 **The opinions expressed n this paper are those of the author and do not necessiarily represent the views of the New York State Department of Taxation and Finance. 415

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

416

NATIONAL TAX JOURNAL

income tax provisions. A major question for the states, as it was for the federal government, was how would taxpayers react to the federal repeal of the capital gains exclusion? The question had to be answered in a situation where the empirical work ignored state taxes on capital gains. This paper investigates whether taxpayers respond to changes in state tax rates as well as federal tax rates when realizing capital gains. Omitting a tax-rate effect on capital gains at any level of govemment may lead to an inaccurate and biased measure of the taxpayer behavioral response and how it affects the level of capital gains realizations and revenue. Misjudging the effect of taxpayer behavior could create inequities in tax policy when crafting federal and state tax reforms. If states overestimated the sensitivity of taxpayer behavior to the federal tax rate increase, they would fail to give back all the revenue windfall that was intended to be returned as their policy goal. An underestimate of the reaction of taxpayers would produce a greater-than-intended tax reduction and possibly lead to fiscal difficulties for some states. The taxpayer response to capital gains tax rate changes was probably the most critical assumption many states had to face in reforming their personal income taxes to maintain conformity with federal tax laws. A summary review of the literature that appears to be the most consistent with the experience of taxpayers' reaction to changes in capital gains tax rates since the enactment of the federal Tax Reform Act of 1986 is presented in the next section. It contains a discussion of the different ways that taxpayers can respond to changes in capital gains tax rates. Aside from tax rate effects, there are a number of economic factors influencing capital gains behavior. These factors are outlined along with sources of data limiting their measurement. The combina tion of tax-rate effects and economic factors are used to estimate capital gains realizations. Alternative specifications are presented for estimating the various components of taxpayer capital gains behavior followed by a summary of statistical

[Vol. XLI

results of the effects of federal tax rates on U.S. capital gains realizations. The analytical framework to estimate the effects of federal tax rates on capital gains realizations of U.S. taxpayers is "stepped down" to analyze the impact of changes in federal and state tax rates on capital gains realizations of taxpayers in a particular state. New York State's experience of changes in capital gains realizations from the federal Tax Reduction Act of 1986 and New York State's Tax Rate and Reduction Act of 1987 is described and documented in some detail. It will be demonstrated that state tax rates, like federal tax rates, influence taxpayer behavior in realizing capital gains. The failure to consider the behavioral effects of state tax systems could lead to overestimates of revenue and unintended tax cuts by states and the federal government when reforming their tax laws. Review of Literature A growing number of studies have demonstrated statistically that raising capital gains tax rates will lower the realizations of capital gains. The difficulty is that there is no general agreement among these studies concerning the degree of taxpayer response to capital gains tax rate changes. The question is whether capital gains realizations will decline by a greater or smaller percentage than the increase in the average tax rate on capital gains. Recently this disagreement has been raised in the context of determining the federal revenue-maximizing tax rate on capital gains. Studies have "deterniined" that this rate lies between a range from far higher to far lower than the average marginal tax rate existing under current law. Earlier studies can be categorized into two major approaches: cross-section and time-series studies. Cross-section studies measure the differences in capital gains behavior across taxpayers or groups of taxpayers for one or more years after accounting for the influences from other tax return characteristics of the taxpayer such as total income, age, dividends and number of dependents. Cross-section studies

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS

SEASTRAND

suffer from a number of methodological shortcomings. One difficulty is that the analysis usually covers only one tax law and one year of data. A second problem is that transitory and permanent responses to changes in tax rates cannot be identified separately without extending the study to include longitudinal or timeseries analysis, The transitory effect is the initial response of taxpayers to a change in the tax rate or response to a temporary change in tax rates. The long-term reaction to a tax rate change is considered to be a permanent effect. A third concern is the restriction of cross-section studies to the use of tax return information. Economic data that is not on the tax return is difficult to merge statistically with taxpayer information. These shortcomings have contributed to widely different conclusions among crosssection studies. The conclusions of crosssection studies have ranged from taxpayers being highly responsive to changes in capital gains tax rates, as in Feldstein, Slemrod and Yitzhaki (1980), to taxpayers having a low response in Minarik (1981). The shortcomings of cross-section studies are too restrictive for analyzing the impact of fundamental tax reform on taxpayer capital gains behavior and revenue. A summary of cross-section studies are reviewed elsewhere in CBO (1988) and in Cook and O'Hare (1987) and will not be considered here any further. Results from time-series studies have a greater central tendency than cross-section studies partly because time-series studies generally use similar data over the same time period. These studies observe how changes in (weighted average or maximum) marginal tax rates affect capital gains realizations after accounting for factors that are independent of tax return information and taxpayer behavior including income, wealth and price effects. Time-series studies include the effects of varying tax laws and can, at least theoretically, separate estimates of transitory from permanent taxpayer responses to tax rate changes. This study attempts to build upon the most salient features of prior time-series studies to develop a more robust model

417

explaining national capital gains behavior. The model is brought down to the state level to determine what role a state tax system can play in influencing capital gains behavior. Until this time, the study of the influence of state capital gains tax rates on capital gains behavior has been very limited. 2 Effect of Marginal Gains Realizations

Tax Rates

on Capital

The change in tax rates on capital gains will affect the realization of capital gains in several distinct ways. These behavioral responses are differentiated by the timing of the response with respect to the tax law change. One of the major efforts of previous studies has been on separating the measurement of the initial or transitory taxpayer behavioral response from the permanent response beginning with the effective date of the tax law change. The difficulty of statistically isolating a permanent response from a transitory response was noted in CBO (1988). Its attempt to measure the permanent effect based on behavior beginning with the second taxable year after a change in tax rates proved to be inconclusive and statistically insignificant. Other studies have tried to differentiate the response between the short-term or transitory reaction to temporary rate changes, say, in the first year of a new tax law from the long-term or permanent effect once the rate changes have been in effect for a year (including analysis conducted by the U.S. Department of the Treasury (1985), CBO (1986), and Auten and Clotfelter (1982)). Studies that have reported statistical differences between transitory and permanent effects have found the transitory behavioral effect to be greater than the permanent effect. Permanent Effect-One way taxpayers respond to higher marginal tax rates is by deferring the realization of capital gains and increasing the average period of time an asset is held before it is sold. By increasing the asset holding period, investors raise the after-tax rate of return and defer the tax increase. This will be exacerbated because the tax law continues to

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

418

NATIONAL TAX JOURNAL

allow capital gains to escape taxation entirely when appreciated assets are transferred to taxpayers' heirs at death. The deferral of capital gains realizations can have a considerable immediate effect on the proportion of accrued gains realized. In an expanding economy, the lengthening of the capital asset holding period will lower the percentage of unrealized gains that are realized, but it should only be lowered by a moderate amount according to Bailey (1969). In the long run, the increase in capital gains realizations from holding an asset longer can more than offset the reduction in realizations from initially deferring the realization of the gain. Thus, the revenue effect from the initial deferral of capital gains realiza tions will diminish over time and eventually vanish for accrued gains unlocked before death. The portion of the effect after the first year is considered to be permanent in the time-series analysis. The other permanent effect from raising the capital gains tax rate is an increase in the deferral of capital gains realizations until death. Unrealized gains at death permanently escape from taxation of capital gains because the cost basis is stepped up to market value. This effect has a permanent impact on revenue. Studies in the literature have used the prior year's (or average of two prior years) tax rate(s) along with the current year's tax rate as a proxy for determining the permanent effect. This may have some relevancy in cross-section/time-series studies where individual taxpayers (under a constant tax law) may face a long-term permanent rate and a transitory rate for a brief period of time. In time-series studies involving tax law changes, there is no apparent reason for taxpayers to defer capital gains by responding to tax rates in effect in prior years. The deferral of capital gains realizations is based on taxpayers'response to current and future tax rate changes, which may have little bearing on past tax rates. Measuring the permanent effect is more complex than what has been specified in the literature to date. Spin-Up Effect-There is one major taxpayer behavioral effect which has not been given much attention in the litera-

[Vol. XLI

ture until a recent study by CBO (1988). When there is time between enactment of a new tax law and its effective date, taxpayers have an opportunity to alter tax strategies before the new tax law takes effect. In other instances taxpayers may anticipate the enactment of pending legislation and even react before certain provisions are enacted and made effective retroactively into law. In the past, tax law changes gave taxpayers an incentive to smooth out their distribution of capital gains realizations by accelerating or postponing the realization of capital gains so that they would not be pushed into higher tax brackets. CBO statistically tested the effects of tax law changes on taxpayer behavior in which taxpayers had time to respond before enacted legislation went into effect, CBO made adjustments to exclude tax rate changes that taxpayers could not respond to in advance of their effective date and found the taxpayer response to be statistically insignificant. The CBO analysis was made from 1954 through 1985 and did not include the impact of the Tax Reform Act of 1986 because the amount of 1986 capital gains realizations was not available. As we now know, there was an enormous behavioral response following the enactment of the Tax Reform Act of 1986. Increasing the 1987 capital gains tax rate in the Tax Reform Act of 1986 created a substantial incentive for taxpayers to accelerate or "spin-up" the realizations of capital gains into 1986 to '%eat" the tax rate increase. Taxpayers were advised to realize capital gains before the end of 1986 if they planned to sell capital assets by the end of 1987. The marketing effort and financial advice of accountants, financial planners and brokers around the nation apparently encouraged investors to spin up a large amount of capital gains realizations in 1986. The spin-up of capital gains from 1987 (and possibly from years later) to 1986 appears to be responsible for the tremendous, unanticipated run-up in capital gains revenue collected in 1987 by the federal government and many states. These states and the federal government discovered an

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS SEASTRAND

unexpected surge in revenue in 1987 from estimated and final payments and extensions for the 1986 tax liability year. New York State's experience was that the spinup effect had a profound impact on 1986 tax revenue. Incorporating 1986 data into the analysis (as demonstrated in the New York State experience) showed that the spin-up effect is a statistically significant taxpayer behavior. The spin-up of capital gains realizations into 1986 has ramifications for future years. It can cause a reduction of capital gains realizations in 1987 and years beyond. In effect, the spin-up of capital gains realizations may have borrowed from the stock of unrealized gains that would have been realized in later years in the absence of the tax rate changes. The spin-up is estimated by the effect of marginal tax rates in the subsequent year on capital gains that are realized in the current year. Transitory Effect-This taxpayer re sponse occurs during the first full year of the tax law change. A tax rate increase, as in the Tax Reform Act of 1986, produces a decline in capital gains realizations. The decline is from the acceleration of some realized gains into the prior year to avoid a current tax increase and a deferral of realized gains into the out years to postpone a future increase in tax liability. The transitory effect is specified as the difference between the marginal tax rate and the spin-up effect. The Elimination of the Preferential Treatment of Long-term Capital GainsThis enabled the federal government to remove the distinction between long- and short-term gains and tax all realized gains equally. There is no longer a minimum holding period to qualify for capital gains tax preferences beginning this year (1988). It is believed that a decrease in the holding period can be expected to increase longterm gains, Kaplan (1981), and CBO (1988). More short-term gains will become long-term with a shorter minimum holding period. This is because assets held for nearly the minimum holding period tend to be held a while longer for longterm gains. A shorter holding period should decrease the amount of short-term

419

gains and increase the volume of trading and frequency of realizing long-term gains. Transactions costs will likely increase with the greater frequency of trading and can offset some of the increase in long-term capital gains realizations. It is generally believed that eliminating the holding period will have a negligible impact on total (short-term plus long-term) capital gains realizations. The uncertainty is whether the increase in frequency of asset sales will generate additional transactions costs that will reduce total capital gains realizations. CBO (1988) found that reducing the holding period to qualify for long-term gains will increase the amount of what would have been defined as long-term gains, although the increase is not statistically significant. When the impact on positive (long-term and short-term) capital gains is taken into account this study found that eliminating the holding period will reduce total capital gains realizations. The increase in what would have been long-term gains is achieved at the cost of a decrease in short-term gains. Again, the impact is statistically insignificant. Data Limitations

on Capital Gains

The estimation of capital gains realizations behavior is restricted by certain data limitations. One data limitation is the unavailability of data on the source of capital gains realizations -the stock of accrued, unrealized capital gains. No published data exists on what investors paid to purchase assets (the cost basis) and on the amount of unrealized gains unlocked and untaxed at death. The market values of certain types of assets are used as proxies for unrealized gains even though the ratio of accrued gains to wealth can change when gains are realized or when depreciation for tax purposes exceeds economic depreciation. The realization of capital gains is derived from the stock of accrued, unrealized gains. In the estimation of capital gains behavior there are two approaches to the measurement of the stock of accrued, unrealized gains. One source of the

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

420

NATIONAL TAX JOURNAL

stock of unrealized gains is the Federal Reserve Board data on the revaluation of assets for corporate equities and noncorporate businesses. The revaluation of assets is equal to the change in unrealized capital gains (change in asset market value less net purchases) including unrealized gains unlocked at death.' By including the unrealized gains unlocked at death, the cumulative sum of revaluation of assets overstates the total stock of unrealized gains. A second approach has been to construct estimates of the stock of unrealized gains as in Auten (1983). Unrealized gains also can be constructed by summing the realizations of capital gains for an assumed average asset holding period. A third measure of unrealized gains is a proxy value from the year-end market value of assets by asset type as reported by the Federal Reserve System.' The principal asset types held by households are: corporate equities, bonds, land, owner-occupied housing and equity in noncorporate business. The most likely sources of capital gains subject to tax are corporate equities, bonds, equity in noncorporate business and land. The capital gains on owner-occupied housing largely escape taxation.5 The most important source of capital gains is from corporate stock. Corporate stock accounted for 24.7 percent of net capital gains in 1981. The percent of capital gains attributable to corporate stock transactions is understated because some of the major asset categories include realized gains from the ownership of corporate stock. These asset categories includ capital gains distributions, prior year installment sales proceeds, share of capital gain or loss from partnerships and fiduciaries and unclassified transactions. Excluding these four asset categories would leave corporate stock accounting for nearly 40 percent of net capital gains (IRS, 1985-86). Economic Factors Affecting Capital Gains Realizations Behavior Capital gains are eventually realized or otherwise unlocked from the stock of accrued, unrealized gains. The forces motivating the realization of gains are nu-

[Vol. XLI

merous. They include the sale of assets to finance the purchase of consumer durables or human capital investments, the restructuring of investment portfolios in reaction to changing opportunities or risks in financial markets, increased demand for assets by other investors and death. Although the taxation of capital gains is avoided by death, the assets may be liable for estate tax. Capital gains realizations behavior can be explained by a number of measures of economic activity that influence investors to purchase capital assets. These measures vary from such broad-based measures as GNP, to the market value of assets, dividends paid out and the constructed stock of unrealized capital gains. This study tried to build upon the earlier work of others by analyzing how individual classes of assets contribute to capital gains realizations. Until now, earlier studies measured the effect of the market value of corporate equities of households and other tradeable (and nontradeable) wealth on the realization of capital gains. The market value of assets of households was separated into several classes: (1) corporate equity, (2) equity in noncorporate businesses, (3) owner-occupied housing, (4) land and (5) bonds. With the exception of corporate equity, the market values of these assets were highly correlated with one another. As a result, the highly correlated assets had to be used in some linear combination. As in most other studies, corporate equity offered the best explanation of capital gains realizations followed by the linear combination of all other assets. The constructed value of unrealized capital gains was found to be an alternative explanatory variable to the market value of assets in determining capital gains realizations. Financial factors affecting market risk were significant contributors to the timing of the realization of capital gains. Income produced by assets (corporate profits), cost of money (short-term interest rates) and liquidity of the financial system (money supply) are important determinants of when capital gains are real ized. Investors are likely to realize greater gains *hen market risks are the highest, i.e., when corporate profits are high,

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS SEASTRAND

money supply is plentiful and cost of money is low. The proportion of unrealized gains that are realized increases with the market risk, the rise in the rate of return of other competing investment opportunities, the increase in personal and business savings available to purchase assets, the flow of money capital around the world affecting asset appreciation and the general rise in the expected fortunes of financial markets. Five types of equations explaining capital gains realizations were developed. These equations are labeled by one variable that distinguishes each equation from the others rather than by the variable that best explains taxpayer behavior. These equations are characterized by: (1) the general level of economic activity (GNP), (2) asset wealth as a proxy for the measure of unrealized capital gains, (3) dividend income, (4) money supply, and 5) the revaluation of assets as an estimate of unrealized capital gains. These five variables are highly correlated with each other and they cannot be used together to estimate realized capital gains without biasing the coefficients because of multicollinearity. MFhen these variables are individually combined with other factors explaining capital gains behavior, five different types of models obtain. 1. The Level of Economic Activity (GNP) Equation GNP is the broadest indicator of economic activity measuring income from capital (assets) and labor and the value of national product or output. In the context of the National Income Accounts: income from assets determines the capitalized value of assets; dividends are the part of income that are paid to investors as a return on investment; labor income provides demand for assets; and output reflects consumer durables that are purchased by capital gains realizations. The timing of capital gains realizations varies directly with the level of GNP. II. Asset (Wealth) Equation The market value of assets is a good measure of the stock of unrealized

421

gains that is available to be realized. This study disaggregates the effects of the various types of financial assets where possible. The market value of specific types of assets besides corporate equities were found to be important in determining capital gains realizations. The linear combination of equity in noncorporate businesses, bonds, owner-occupied housing and land influenced the realization of capital gains. The major statistical difficulty is that the market value of bonds, owner-occupied housing, land and equity in noncorporate businesses are highly correlated with each other. The solution was to combine these assets as a single factor in explaining capital gains realizations. 111. Dividend Income Equation Dividend income is an important measure from which to capitalize the present value of a future income stream received by investors. The dividend yield also can be compared to market rates of interest to price assets based on the difference between asset yield, interest rates on fixed income investments and alternative forms of savings, and the cost of money for purchasing assets. IV. Money Supply Equation The amount of liquidity is a primary driving force underlying the value of assets and the realization of capital gains in the money supply model. Financial markets feed on liquidity. The rise in liquidity tends to lead the increase in asset values. A downturn in liquidity signals increased market risk, creating incentives for investors to realize gains before asset values erode further and returns on investment decline. V. Revaluation of Market Assets Equation The revaluation of market assets is a constructed proxy for the value of the stock of unrealized capital

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

422

NATIONAL TAX JOURNAL gains. The revaluation sum overstates the stock of unrealized gains by the amount of gains unlocked at death. Revaluation of corporate equities and equity in noncorporate businesses were both tested for their statistical significance in estimating the amount of capital gains realizations.

The Effect of Federal Tax Rates on Capital Gains Behavior in the U.S. There are many possible specifications for explaining the response of capital gains realizations to tax policy changes. It was found that the alternative equations for explaining capital gains realizations were sensitive to how the equations were speeified, but the more statistically robust alternatives are presented as they have greater precision, accuracy and consistency in their results. The family or group of specified equations described above offers both theoretical and empirical explanations of capital gains realizations and generally display statistical results that agree with those obtained by CBO (1988). The explanatory power of the equations, the standard error of the estimates, and the precision of the tax rate effects appear to be at least on par with the CBO (1988) statistical results. Statistics from the CBO on long-term capital gains realizations and weighted average marginal tax rates for long-term capital gains were used as a starting point for specifying equations to explain capital gains realizations. The CBO marginal tax rates were calculated from predicted (instead of actual) weights of capital gains realizations using dividends and adjusted gross income less gains as explanatory vari ables. The calculated average marginal tax rates are used because they are independent of the response of capital gains realizations to tax changes. This improves their explanatory power in the behavioral equations. Estimates of taxpayer capital gains behavior are obtained from the family of behavioral equations explaining long-term capital gains from 1954 through 1985. The explanatory variables are expressed in

[Vol. XLI

nominal terms. The equations have been formulated in semilogarithmic and logarithmic forms to estimate the exponential growth in capital gains realizations and to conveniently estimate the revenuemaximizing tax rate and the tax-rate elasticity of capital gains realizations. Other functional forms were not evalu. ated to determine if they would be better in explaining taxpayer behavior. The statistical results in Table 1 are the five equations that explain the realizations of capital gains throughout the nation. Other variables that explain capital gains realizations that are included in these models are: the market value of corporate equities of households, income of assets (corporate profits before taxes), the cost of money (three-month Treasury bill rates), money supply and the change in money supply. Each one percentage point increase in average marginal tax rates on capital gains reduces capital gains realizations by about three percent. It should be noted that the spin-up effect is not statistically significant. The analysis excluded the effects of tax reform in 1986 (because U.S. capital gains realizations data was unavailable). Based on New York State's experience with the Tax Reform Act of 1986, the spin-up effect should prove to be statistically significant throughout the nation once an estimate for 1986 U.S. capital gains realizations becomes available. Federal Revenue-Maximizing Tax Rate on Capital Gains and Tax-Rate Elasticity Estimates of the federal revenue-maximizing tax rate on capital gains and taxrate elasticity are obtained from the semilogarithmic and logarithmic forms of the capital gains equations. Revenues are maximized for a single-rate (flat) tax when a one percentage point increase in the tax rate generates an equal percent decline in the tax base (i.e., capital gains realizations). The revenue-maximizing tax rate is conveniently expressed in a semilogarithmic functional form as 1/B, where B is the regression coefficient for the marginal tax rate. 6

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

FRANS

No. 31

SEASTRAND Table

423

1

Explanation of Capital Gains Realizations in the United States From 1954-1985 GNPEquation 1 ln(RCGUS) - -4.953+ 0 318 ln(GNP) + 0.696ln(CRPEQ)+ 0 386ln(ZB)- 0 185ln(TREASST)- 029MTRUS + 0.185la(RCGUSG) (7.62)

(-7 50) (l.T7) R'

0 992 S.E E - 0 085 D W.

(2,51)

(-2.87)

(-3.28)

(1.84)

1.73

Asset (Wealth) Equation 2. ln(RCGUS) R'

3.103 + 0.172 ln(ASSETS) (-4.84) (1.59)

0.993 S E E.

0078 D W

+ 0 516 ln(CRPEQ) (5.46)

+ 0.349ln(ZB) (2.61)

+ 4.978 dia(MS1) (372)

- 0.032 MTRUS (3.63)

+ 0.167 ln(RCGUSG) (201)

1.53

Dividend Income Equation 3 ln(RCGUS) R2

2.963 + 0.343 la(DIVUS) + 0,571 ln(CRPEQ) + 0.408 tn(ZB) + 4 452 dLn(MS1) 0.032 MTRUS (-2.82) (-445) (165) (5.22) (227) (3.n

0991 S.E.E.

0.097 D.W.

1.15

MoneySupply Equation 4. LN(RCGUS) 3.53 + 0 294 ln(MS1) + 0.527 ln(CRPEQ) + 4.323 dln(MSI + 0389 tn(ZB) 0 033 MTRUS + 0.138 ln(RCGUSG) (4.79) (1.84) (5.68) (3-37) (363) (-3.90) (138) R'

0.993 S F E.

0 077 D.W.

1.51

Constructed Stock of UnrealizedGains Equation 5 [n(RCGUS) - -4.711 + O-W ln(SREVCEO) + 0 192ln(ASSET'S))+ 0.299ln(ZB) + 5 363din(MSI) 0.034 (MTRUS) + 0.178tn(RCGUSG (3.76) (2.07) (-495) (5 13) (1.73) (219) (396) R'

0.992 S.E.E. - 0 081 D.W.

1.48

Note: t - Statistics are in parenthesis Variable Definitions: RCGUS:

Realized net long-term capital gains, in excess of net short-term

losses in U.S.

GNP: Gross National Product CRPEQ:

Corporate

ZB: Corporate

equity of households

TREASST.- Short-term MTRUS: RCGUSG:

in U.S.

profits before taxes treasury bill rate (3 months) lagged one year

Weighted average marginal tax rate on U.S. capital gains Realized

net long term capital gains, in excess of net short-term

losses in U S lagged one year

ASSETS: End-of-year market value of the sum of household equity in noncorporate land and bonds ofU.S. households

business, bonds, owner-occupied

housing

MS1: Money supply (Ml) DIVUS: U.S. dividend income SREVCEQ:

Sum of revaluation

Of Corporate equity of U.S. households

The impact of the Tax Reform Act of 1986 on U.S. capital gains realizations is presented in Table 2. Capital gains realizations are expected to decline by 30 percent in 1987 from the increase in federal tax rates on capital gains. Revenue from capital gains should continue to expand

since 1947

as the percent increase in tax rates exceeds the percent decline in capital gains realizations (tax-rate elasticity is about -0.60). The estimates of the federal revenue-maximizing tax rate indicate that marginal tax rates can be increased by more than 10 percent above current levels

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

424

NATIONAL

TAX JOURNAL

[Vol. XLI

Tcible 2 Federal Revenue-Maximizing Rate and the Impact of the Tax Reform Act of 1986 on U.S. Capital Gains Realizations

Federal Revenue-

Equation

Percent

Maximizing Tax Rate

Tax-Rate Elasticity

Change

1 (GNP)

34.5

Transitory Effect -0.53

2 (ASSET)

31.3

-0.58

-30

3 (DIV)

31.3

-0.59

-30

4 (MS1)

30.3

-0.59

-30

5 (REV)

29.4

-0.62

-32

Spin-tJp

in

Capital Gains Realizations in 1987 1986 Transitory Spin-Up Effect -27

*Statistically insi M*ficant (an estimate of capital gains realizations for 1986 is not available a f before maximum revenue is collected from capital gains. Effects of Federal, State and Local Tax Rates on Taxpayer Capital Gains Behavior in New York State New York State's tax law conforms partially to the Internal Revenue Code. With the passage of the Tax Reform Act of 1986, New York State was one of a number of states that had to assess the revenue implications of the flow through of basebroadening provisions of capital gains income on its personal income tax. These base-broadening provisions, federal conformity and federal/state tax linkages

have changed federal, state and local tax rates on capital gains .7 The effects of federal, state and local taxes on capital gains were analyzed to obtain an understanding of how taxpayers respond to capital gains tax rates in New York State. Methodology The study of New York State capital gains realizations follows from the national time-series analysis. The methodology incorporates statistical features of the equations that estimated national capital gains realizations and relates the behavioral response of taxpayers to New

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS SEASTRAND

York State and New York City tax rates on capital gains. It should be noted that, in doing the New York State analysis, the definition of capital gains realizations was extended to include short-term gains. Realized capital gains of New York State taxpayers are defined as positive (long-term and shortterm) capital gains of taxable returns. Net losses are omitted. The realization of capital gains is believed to respond to state and national economic activity, the market value of corporate equities, equity in noncorporate business and other assets held by New York State households, and the stock of unrealized capital gains. Gross state product (if reliable data were available) could be used as a broad-based measure of capital gains realizations of state taxpayers, but GNP is believed to offer a better measure of the timing of capital gains realizations in national financial markets. Dividends were evaluated as a component of income that would affect the appreciation of assets. Likewise, U.S. dividend income is better suited than state dividend income as a measure of capital gains realizations of state residents because timing is conditional upon the health of corporations and national financial markets. Estimates of New York State capital gains realizations were developed from the annual study of a representative sample of New York State income tax returns. Data from these annual studies has been gathered from 1964 through 1985. A preliminary estimate of capital gains realizations for 1986 was made from a special study of 18,000 tax returns analyzing the spin-up effect. The final estimate of capital gains realizations for 1986 from the annual personal income tax study should be available soon. By including 1986 data, the spin-up effect under the Tax Reform Act of 1986 was captured in the analysis. In the methodology, the variation of capital gains was related separately to weighted average marginal tax rates for the U.S., New York State and New York City. The tax rates used in the equations are the weighted average marginal tax rates for each year. The federal marginal

425

tax rates of U.S. taxpayers were.used as proxies for New York State taxpayers. The New York State tax rate variable accounted for the historical effects of the State minimum tax and the federal offset. The New York City tax rate includes the effects of the State and federal offset and the historical effects of the City minimum tax. It was prorated to reflect the New York city share of New York State capital gains realizations. The estimates of the market value of New York State assets were made by attributing a proportion of the value of U.S. assets to New York State according to New York State's share of sources of personal income derived from those assets. The estimates of the market value of New York assets were imputed from the following sources of income. Assets Source of Income Corporate equity Dividend income Equity in noneorporate businesses Dividend income Owner-occupied housing Rental income Land Rental income Bonds Interest income The prorated market value of New York State assets is not as accurate a measure of asset value as the national data and is likely to be a source of error when estimating the behavior of New York State capital gains realizations. This is one reason why the standard error of the statistical analysis of taxpayer behavior of capital gains for New York State is twice as large as that obtained for the n-ational analysis. Statistical

Results

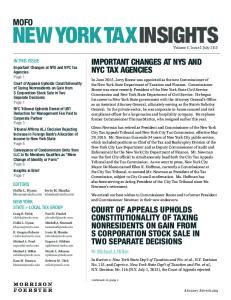

of Tax Rate Effects

Figure 1 shows the time trend of federal and New York State weighted average marginal tax rates on capital gains realizations and New York State capital gains realizations since 1954. Between the middle of the 1950s and 1968, federal and New York State tax rates were fairly stable (see Appendix). New York State's top tax rate on capital gains increased from 3.5 percent (on $9,000 taxable income) to 5.0 percent (on $15,000 taxable income) in 1959. The federal tax rate was effectively capped by the alternative mini-

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

Comparison with

0

Figure 1. Positive Capital & NYS Marginal 1954 1987

of NYS Federal

Ga T

Estimate

as--

Marginal Combixi.ed (Right

Tax Federal

ReLtes, & state

Scale.

Rates)

zo--

io--

Federal

Marginal

(Right

Scale.

Tax

Rates

Rates) Positive

CaLpital (Left

Scale,

Gains

Realiz

$Billions)

01954

1958

1962

1966

1970 Year

1974

19

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS SEASTRAND

mum tax at 25 percent. Capital gains realizations trended upward during that 14 year period, paralleling the long-term bull market in corporate equities. During the next decade, federal and New York State tax rates rose and capital gains realizations declined. In 1968, federal and New York State tax rates on capital gains marked a ten-year period of substantial increases. The federal increases were featured by tax surcharges (1968-1970), a new add-on minimum tax on tax preference items and reductions in maximum tax rate benefits from tax preference items ("maximum tax poisoning"). New York State tax rates rose from a series of increases in top rates, tax surcharges, the introduction of a minimum tax on tax preference items and a reduction in the capital gain exclusion from 50 percent to 40 percent. During this time frame, financial markets went through two severe downturns (1968-1970) and (1973-1975), the latter in which many households throughout the nation liquidated financial assets. By 1977, long-term capital gains realizations in New York State were one-half the peak level set a decade earlier. Since the latter part of the 1970s, federal and New York State tax rates were reduced, while capital gains realizations increased dramatically. In 1978, federal and New York State tax rates on capital gains began an eight-year decline. The federal capital gains exclusion was increased to 60 percent, the top tax rate on income was reduced to 50 percent and the alternative minimum tax on tax preference items was cut. In addition, the minimum holding period to qualify for longterm gains was reduced from one year to six months. New York State embarked on a long-term tax-reduction program including a general decline in the top tax rate and an increase in the capital gains exclusion from 40 percent to 60 percent. Between 1975 and 1987, financial markets experienced tremendous increases in the market value of assets and trading volume. As a result of this asset appreciation and trading activity, positive capital gains realizations in New York State

427

increased by nearly 14 fold between 1977 and 1986. In 1987, tax rates on capital gains realizations increased by more than 50 percent and capital gains realizations are estimated to have fallen by 38 percent. This historical review portrays a negative correlation between capital gains realizations and federal and New York State weighted average marginal tax rates on capital gains. Effects of State Tax Rates-Estimates of the statistical response of capital gains realizations to changes in tax rates in New York State are shown in Table 3. The statistical analysis reveals that changes in state as well as federal tax rates have had a significant role in motivating taxpayers to realize capital gains. It is interesting to note that the behavioral effect of federal tax rates in the equations for New York State is similar to the behavioral effect of federal tax rates in the national results. Although federal tax rates are the more dominant force in affecting capital gains, New York tax rates demonstrate a meaningful effect on taxpayer behavior. Effects of Local Tax Rates-The effect of New York City's marginal tax rates on taxpayer capital gains behavior is statistically insignificant. The New York City tax on capital gains as a percent of total capital gains tax liability is small. Changes in New York City capital gains tax rates at historical levels apparently are not a primary concern to taxpayers who decide to realize capital gains. Analysis of the Spin-up The spin-up effect is when additional capital gains are realized to avoid increases or anticipated increases in tax rates in the following year. The spin-up is a euphemism for tax rate increases in the Tax Reform Act of 1986. A tax rate decrease would have led to a decline in capital gains realizations to catch the benefit of lower ftiture tax rates. The spinup effect stems from two contributing sources: (1) anticipated New York State tax rate changes and (2) anticipated or actual federal tax rate changes.

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

NATIONAL

428

TAX JOURNAL

[Vol. XLI

Table 3 Effect of Federal,

State and Local Tax Rates on Capital

Realizations

Gains

in New York State From 1954-1986

GNP Equation 1 ln(RCGNY)

= 8.OM

+ 0.418

in(GNP)

(-8.10) (1.61)

+ 1317

ln(CRPEONY)

(10.44)

+ 0.361 1.(ZB)

(1.38)

0 145 ln(TREASST)-

(137)

0.061

(-2.29)

MTRUS

+ 0.027 MTRD

(196)

0.143 MTRUY

(3.28)

R' - 0.975 S.E E. - 0.149 D.W. - 195 Asset (Wealth) Equation 2.ln(RCGNY)

-6.662+0.2701n(ASSETNY)+1.244in(CRPEQNY)+03771n(ZB)+3.2DOdin(MS1) (.6.10)

R'

(1.57)

(8.97)

(1.89)

0.06OMTRUS+0022MTPD-0134MTRMY (2.26) (1.97)

(1,26)

(3.17)

- 0 976 S.E E. - 0.146 D.W. - 2.04

DividendIncome Equation 3. ln(RCGNY)

R2

0.9n

- 4.71 + 0.591 ln(DIVUS) (-5.49) (4.39)

+ 1042 tn(CRPEQNY) (7-52)

+ 4.47 din(MS1) 0.057 NffRUS (1.83) (220)

+ 0 023 MTRD (196)

- 0.120 WRRNY (2.86.)

S.E.E. - 0.151 D.W. - 1.79

MoneySupplyEquation 4. ln(RCGNY)

lk2

- -7.996 + 0.382 ln(MSI) + 1.311 ln(CRPEONY) (-8.14) (1.58) (11.38)

0 9-74 S.E E.

0.148 D.W

+ 0.466 ln(ZB). 0 055 MTRUS (141) (1.98)

+ 0.218 MTRD (186)

O.M MTRNY (-3.65)

1.96

Constructed Stock of Unrealized Gains Equation 5 ln(RCGNY) R2

-

0.974 S.E.E.

1094 + 0,9301n(SRCEQNY) (-7.13) (874) o.149 r).w.

+ 0470in(ASSETNY) (4.05)

+ 4.800dln(MSI) (206)

0.058MTRUS (224)

+ 0023MTPD (204)

0.135MTRMY (3.41)

= 1.79

Note: t - statistics are in parenthesis Variable Definitions: RCGNY: New York State realized positive capital gains (long term and short term). Returns with net losses are excluded GNP: Gross National Product CRPEQNY: Corporate equity of New York State households ZB: Corporate Profits before taxes T'REASST: Short-term treasury bill rate (3 month%) lagged one year MTRUS: Weighted average marginal tax rate on U S capital gains. MTRD: Weighted average marginal tax rates On U.S. and New York State capital gains realizations in the subsequent year MTRNY: Weighted average marginal tax rates on New York State capital gains realizations ASSMY: End-of-year market value of sum of equity in noncorpOTate businesses, owner-occupied housing, land and bonds of New York State households MSI: Money supply M-1 DIVUS: U.S. Dividend income SRCEQNY: Sum of revaluation of Corporate equity of New York State households since 1947

New York State tax reform was not enacted until after the end of the 1986 tax year. Taxpayers had to anticipate the level of the 1987 State tax rates in deciding whether to realize gains in 1986. What was anticipated by investors is highly uncertain. If the law was not changed, taxpayers would have been subjected to a large tax increase. However, elected government officials began to announce before the end of the 1986 tax year the intent to

return the entire windfall to taxpayers. Many changes in New York State's personal income tax law since 1954 were made effective retroactive to the first of the tax year in which the changes were enacted (see Appendix). This made estimating the spin-up difficult for New York State. It was assumed that taxpayers would have made decisions to realize capital gains in response to actual changes in the tax law. It is estimated that about 90

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS

SEASTRAND

429

Table 4 The Impact of Federal and State Tax Rates on Capital Gains Realizations in NewYork State

PercentChange Change nCapital GainsRealzatons 1987 Transitory Effect

Tax-Rate Elastcity Transitory Effect

SpinUp Equation

1986 SpinUp

U.S.

NYS

U.S.

ws

U.S.

NYS

Total

U.S.

NYS

Total

1 (GNP)

.44

.13

-.58

.68

28

4

32

-28

-14

-42

2 (ASSETNY)

.42

.17

-.61

-.63

28

3

31

28

-13

-41

3 (DIVUS)

.46

.15

-.44

-.61

30

3

33

-25

12

-37

4 (MS1)

42

.17

-.54

-.70

27

4

31

-24

-15

-39

5 (REVNY)

.49

.13

.43

-.69

33

1

34

-25

-13

-38

Table

5

The Impact of Federal and State Tax Rates on Capital Gains Revenue in New York State

Change in Capital Gains Realizations (in $ billions) 1986 Spin-Up Equation

Changein Capital Gains Revenue (in $ billions) 1986 1987 Transitory Spin-Up

1987 Transitory

1 (GNP)

6.2

1.0

7.2

-9.0

-4.7 -13.7

.55

.09

.64

-.79

.41

2 (ASSEINY)

6.3

0.6

6.9

-8.5

-4.2 -12.7

.55

.06

.61

-.75

-.36 -1.11

3 (DIVUS)

6.4

0.7

7.1

-6.6

-3.2

9.8

.56

.06

.62

-.58

-.28 -0.86

4 (MSI)

6.1

0.9

7.0

7.7

-4.8 -12.5

.54

.08

.62

-.67

.42

-1.10

5 (REVNY)

7.1

0.3

7.4

6.8

3.6

.62

.03

.65

.59

.32

0.91

percent of the spin-up of capital gains realizations was attributable to increases in federal tax rates and the remaining 10 percent was caused by a decrease in the federal offset to New York State rates (see Table 4). New York State's positive capital gains realizations increased from $14.35 billion in 1985 to $29.9 billion in 1986-an increase of 108 percent. About one-half of the increase in capital gains is estimated to be caused by the spin-up

NYS Total

NYS Total

U.S. NYS Total

10.4

U.S.

U.S.

U.S. NYS Total

1.20

of effect. The spin-up is an acceleration capital gains realizations from future years. It is likely that a large portion of the revenue spin-up in 1986 came from capital gains that would have been realized in 1987, but the amount is unknown. The total spin-up estimate from the statistical analysis corresponds well with the actual experience in New York State for 1986.8 The spin-up estimates in Table 5 compare favorably with the $646 mil-

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

NATIONAL

430

TAX JOURNAL

lion of unexpected revenue that New York collected from final payments and extensions. This revenue is not only nonrecurring, but it is borrowed from the future revenue stream. The revenue was placed in an Infrastructure Trust Fund for capital improvement expenditures on roads, bridges and low-income housing. There was an additional amount of unanticipated revenue that was collected with estimated payments from 1986 tax returns. Based on the spin-up estimates, it is likely that some of the unexpected surge in revenue may have occurred because of faster appreciation of assets, greater risks in financial markets and the higher volume of asset sales in 1986 rather than because of the spin-up effect. In other words, revenue collections may have been stronger than anticipated in 1986 even in the absence of tax reform. Estimating 1987

the Transitory

Effect for

New York State Department of Taxation and Finance's initial assumption for estimating capital gains revenue in 1987 was a 25 percent decline in capital gains realizations from $29.9 billion in 1986 to $22.6 billion. This translated into a $650 million decline in tax revenue. The assumed decline in capital gains realizations came from the loss of the one-time spin-up of capital gains and a transitory effect. This was offset to some extent by the appreciation of assets. This assumption was made on account of the strength in estimated payments in 1987 and the continued growth of financial markets through the middle of 1987. The transitory effect is estimated from the behavorial impact of the tax rate, excluding the spin-up effect. The transitory effects from changes in federal and New York State tax rates are statistically significant. According to the behavioral equations, New York State capital gains realizations can be expected to decline by 41 percent in 1987 solely from increases in federal and state tax rates. Following the enactment of New York State's Tax Reform and Reduction Act of 1987, State

[Vol. XLI

tax rates on capital gains (after the fed@ eral offset) influenced taxpayers to reduce capital gains realizations by 12-14 percent of what they would have taken without federal tax reform. About twothirds of the transitory effect is explained by federal marginal tax rates and one-third is attributed to New York State marginal tax rates. Capital gains realizations are expected to decline by about 38 percent in 1987 from $29.9 billion to $18.6 billion when the combined effects of increases in the market value of financial assets and federal and state tax rates are considered. The estimates of the transitory effect from the behavioral equations are consistent with current revenue collection trends. The difference between the initial assumption of $22.6 billion in capital gains realizations and the most recent estimate of $18.6 billion is $4.0 billion in capital gains realizations or $350 million shortfall of revenue attributable to understating capital gains behavior from the 1987 tax liability year. impact

of Stock Market

Collapse

of 1987

The stock market collapse of 1987 has been identified as one of the reasons for underestimating taxpayer capital gains behavior. The unexpected stock market panic has had a greater impact on capital gains realizations than previously thought. Initially, anticipated net capital losses were raised by $400 million, following the crash, reducing forecasted revenue by $35 million. It was argued by some analysts that the record-trading volume accompanying the collapse brought about an increase in capital gains realizations from taxpayers with large, accrued gains. An analysis of trading volume and capital gains realizations confirms that the record-trading volume triggered an increase in capital gains realizations during the stock market crash. The record-breaking volume during the last half of October and November raised the annual volume by nearly 6 percent. Given the volume elasticity (0.33), capital gains realizations increased by 2 percent or $400 million from the higher trading volume, raising $35

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS

SEASTRAND

million in revenue. However, capital gains realizations are about three times as responsive to the market value of assets (elasticity of 1.1) as trading volume. The effect of the free fall in market prices of equities that characterized the market crash swamped the effect of the recordtrading volume on capital gains realizations. The loss in market value reduced the annual market index about 9 percent. The market-price effect produced a loss of capital gains realizations of $1.750 billion or $153 million in revenue. The net revenue impact of the stock market crash of 1987 on capital gains revenue from the combination of the record-volume effect and the market-price effect was a loss of more than $115 million, more than three times the earlier estimate. The additional revenue loss beyond the initial forecast is equivalent to more than 20 percent of the estimated shortfall in revenue from underestimating capital gains behavior.

431

Analysis of Taxpayer Assumptions

Behavioral

The New York State Department of Taxation and Finance estimated revenue from capital gains realizations predicated on certain assumptions about taxpayer behavior. Evidence from early collections data on final payments and extensions from 1987 personal income tax returns indicate that prior assumptions about taxpayer behavior appear to have overstated revenue estimates. An analysis of these assumptions was made by simulating revenue using the five taxpayer behavioral equations and comparing the simulations to the prior revenue estimates. The final outcome of taxpayer behavior on capital gains realizations for 1987 will not be known until the 1987 personal income tax returns are completely analyzed. The equations described in this paper

Table 6 Revenue

Impact

of Estimating

Taxpayer

Capital

Statein (in millions

Gains

Behavior

in New York

1987 of dollars)

Estimated

Original

Capital

Capital

Gains Realizations

Capital Gains

Gains

Assumption in Revenue Forecast

Realizations Shortfall

Revenue Impact

Equation

Realizations

1 (GNP)

19,200

$22,600

$3,400

$(300)

2 (ASSETNY)

18,400

22,600

4,200

(370)

3 (DIVUS)

16,800

22,600

5,800

(500)

4 (MSI)

19,800

22,600

2,800

(245)

5 (REVNY)

16,600

22,600

6,000

(525)

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

432

NATIONAL

TAX JOURNAL

[Vol. XLI

Table 7 Revenue-Maximizing

Tax Rates on Capital Gains Realizations

Equation 1.(GNP) 2. (ASSETNY) 3. (DIVUS) 4. (MSl) 5. (REVNY)

NYS*

U.S. 33.1 31.6 37.9 39.0 37.4

7.0 7.5 8.4 6.7 7.5

*Includes the federal offset to the New York State tax rate. In 1988, the New York State weighted average marginal tax rate on capital gains after the federal offset is 6.2 percent. have been used to simulate capital gains realizations from changes in federal and state tax rates and economic growth. The simulations are compared to the capital gains realizations used for the baseline revenue forecasts. The simulations in Table 6 illustrate that capital gains realizations could decline by nearly four billion dollars more than assumed in the baseline revenue forecast. This is another means of illustrating a revenue shortfall of approximately $350 million in fiscal year 1988 89 from underestimating taxpayer behavior on capital gains. New York State's Revenue-Maximizing Tax Rate on Capital Gains Much attention has been given to estimating the federal revenue-maximizing tax rate on capital gains. There is an analogous tax rate for New York State. New York State's revenue-maximizing tax rate on capital gains was estimated to be in the neighborhood of 7 to 8 percent (including the federal offset) as shown in Table 7. Under current law, New York State's weighted average marginal tax rate is 6.2 percent in 1988 when including the federal offset. This indicates that New York

State, like the nation, has a tax rate on capital gains that may be below the revenue-maxirnizing rate. Omitting the effects of state tax rates on taxpayer behavior, when they are signficant policy variables, will introduce an upward bias to the estimate of taxpayer behavior from federal tax rates. This will result in a downward bias in estimates of the federal revenue-maximizing tax rate. Indeed the estimates of the federal revenue maximizing tax rate tend to be lower in the national analysis (as exhibited in Table 2) than the estimates in the New York State analysis in Table 7. However, the national estimates also are biased by statistical problems associated with autocorrelation. Nevertheless, national studies that ignore the effects of statistically significant state tax rates on capital gains behavior may understate the estimates of the federal revenue-maximizing tax rate. Conclusion The base-broadening provisions enacted in the federal Tax Reform Act of 1986 will limit or eliminate many item ized deductions, restrict tax shelters and

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

FRANS

No. 3]

SEASTRAND

eliminate the preferential treatment of capital gains. Since New York State generally conforms to the federal definitions of income and deductions, federal tax reform would have produced a revenue 11winffall" to the State in 1987 in the absence of any changes to the State tax laws. New York State amended its tax laws in order to prevent a tax increase and give back the windfall to taxpayers. This paper has documented and analyzed how changes in federal and New York State tax rates under tax reform have affected taxpayer behavior in realizing capital gains. Virtually all prior studies measuring the effects of tax rate changes on the realization of capital gains suggest that taxpayers will react to an increase in tax rates by decreasing their "realized" capital gains in 1987. One shortcoming of these studlies is that the findings are based strictly on federal tax rates. The effects of changes in state and local tax rates have been ignored. Provisions in the federal Tax Reform Act of 1986 increase the tax on capital gains at the federal and state levels. This study is an extension of earlier studies of the effects of federal tax rates on capital gains realizations to include the effects of state tax

rates

for New

York

State.

It was

em-

pirically verified that the combined effect of federal and state rate changes should result in a substantial reduction in the realization of capital gains in New York State in 1987. Simulations of taxpayer behavior indicate that revenue from capital gains realizations will be less than originally forecast for 1987, Besides the tax-rate effects, another reason for underestimating taxpayer behavior on capital gains appears to be from understating the effect of the stock market collapse of 1987. These behavioral estimates have important consequences on the State's fiscal plan, estimates of the amount of windfall and reshaping the State's tax code since capital gains is a large percentage of the total revenue windfall and a growing share of total tax collections. Understanding and estimating the behavior of taxpayers an their response to tax change is an impor-

433

tant element in enacting tax reform and forecasting tax revenues. This study demonstrates that state tax systems influence federal as well as state revenue. The federal government has essentially ignored the effects of state conformity to the federal tax code and federal/state tax linkages and how they affect the federal fisc. The effects of state tax rates as well as federal tax rates on capital gains realizations are important to recognize in estimating federal and state budgets and reshaping federal and state tax codes, whether it be for fundamental tax reform, incremental tax changes or return of the revenue windfall to taxpayers. NOTES 'The Tax Reform Act of 1986 only moved toward the equal treatment of taxing capital gains and orginary income by eliminating the capital gains exclu. ,ion There are other preferential treatments of capital gains that have not been eliminated: (1) tax deferral of accrued but unrealized gains, and (2) the escape from taxation of capital gains at death through the step up in the cost basis to market value. 2 For example, Aten (1987) found that capital gains realizations per capita were significantly higher in states (as a group) without taxation of capital gains than in states with taxation of capital gains in 1981. [There was no significant difference in 1980.1 The Economic Recovery Act of 1981 reduced federal marginal tax rates on capital gains. This increased the state share of the total tax on capital gains and en couraged taxpayers to realize more gains in states that did not tax capital gains than in states that did tax ca ital gains. pA) Assett Assett I URCG + Net Investment URCG + (Purchases URCG + (Purchases B) Revaluation, Assett 1

Sales) Cost Basis + RCG)

Asset, (Purchases

Sales)

By Substitution, Revaluation, Where;

= URCG

URCG is unrealized capital gains RCG is realized capital gains

'Board of Governors of the Federal Reserve Sys"Balance Sheets for the U.S. Economy" (1987). 'Most of the capital gains are: (1) rolled over in the

tem,

purchase one-time

of more expensive housing (2) allowed capital gains exclusion of $125,000 since

from

sale

the

of homes

by

and (3) stepped up in their , t death 'The semilogarithmic condition

is:

taxpayers cost

aged basis

55

and

to market

revenue-maximizing

the 1978 over, value rate

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

NATIONAL TAX JOURNAL

434

d[ln(RCGUS)l - -d(MTRUS)/MTRUS or dfln(RCGUS)I/d(MTRUS)/MTRUS In the semilogarithmic d[ln(RCGUS)I/d(MTRUS) By substitution tion, MTRUS(B)

I

equation, B

with the revenue-maxirnizing

condi-

I

or MTRUS - 1/B 'The federal/state tax linkages include itemized deductions of state and local (capital gains) income taxes from federal adjusted gross income. This offset to federal income taxes, in effect, reduces the effective state and local tax rates. This is known as the federal offset. 'The New York State spin up was estimated as the difference between the spin-up from the sum of federal and state tax rate increases and the spin-up from the federal tax rate increase. REFERENCES Aten, Robert H. 1987, "Capital Gains and the Personal Income Elasticity of State Income Taxes," Washington, unpublished paper. Auten, Gerald E. and Charles Clotfelter, 1982, "Permanent Versus Transitory Tax Effects and the Realization of Capital Gains," The Quarterly Journal of Economics, (November).

[Vol. XLI

Auten, Gerald E., 1983, "Capital Gains: An Evalua tion of the 1978 and 1981 Tax Cuts," in Charls E. Walker and Mark A. Bloomfield, eds., New Directions in Federal Tax Policies for the 1980's, Cambridge, MA: Ballinger Publishing Company. Bailey, Martin J., 1969, "Capital Gains and Income Taxation," in Arnold C. Harberger and M. J. Bailey, eds., The Taxation of Income from Capital, Washington, D.C.: Brookings Institution. Congressional Budget Office, 1986. 'Effects of the 1981 Tax Act on the Distribution of Income and Taxes Paid," Staff Working Paper, Washington. Congressional Budget Office, 1988, "How Capital Gains Tax Rates Affect Revenues: The Historical Evidence," Washington. Cook Eric W. and John F. O'Hare, 1987, "Issues Relating to the Taxation of Capital Gains," National Tax Journal, Volume 40, (September). Feldstein, Martin and Shlomo Yitzhaki, 1978, "The Effects of the Capital Gains Tax on the Selling and Switching of Common Stock," Journal of Public Econonies, Volume 9. Feldstein, Martin, Joel Slemrod and Shlomo Yitzhaki, 1980, "The Effects of Taxation on the Selling of Corporate Stock and the Realization of Capital Gains," Quarterly Journal of Economics, (June). Internal Revenue Service, 1985-86 Statistics of Income Bulletin, Washington. Kaplan, S., 1981, "The Holding Period Distinction of the Capital Gains Tax," NBER Working Paper No. 762. Lindsey, Lawrence, 1986, "Capital Gains: Rates, Realizations and Revenues," NBER Working Paper No. 1893. United States Department of the Treasury, 1985, "Report to Congress on the Capital Gains Tax Reductions of 1978," Office of Tax Analysis, Washington.

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS SEASTRAND

435

Appendix New York State and Federal Treatment of Long-Term Capital Gains From 1954 - 1987 Year 1954

New York State

Chapter 511 of the laws of 1938. 1954 Enacted 4/6/38; effective 10/31/37.

Imposed a separate tax on capital gains. Tax rates ranged from 1% on the first $1,000 of taxable income to 3.5 % on taxable income in excess of $9,000. 1959

Year

Chapter 60 of the Uws of 1959. Enacted 3/12/59; effective 1/l/59.

Federal Internal

Revenue

Code of 1954.

50% exclusion for any net long-term capital gains in excess of net short-term capital losses. 6 month holding period for long-term gains and losses. Maximum of $1,000 capital loss deduction allowed to offset ordinary income. Top tax rate on income is 91%.

Tax rates ranged from 1% on first $1,000 of taxable income to 5% on taxable income in excess of $15,000. Required estimated tax payments. 1960

Chapter 563 of the Laws of 1960. Enacted 4/18/60; effective 1/l/61.

Alternative tax of 25% imposed on long-term gains in excess of short-term losses. 1964 Revenue Act of 1964. Enacted 2/26/64; effective 1/l/64. Top tax rate on income reduced to 77% in 1964 and 70% in 1965.

Replaced Article 16 with Article 1968 Revenue and Expenditure Control 22 in NYS Tax Law. Act. Separate tax on capital gains Enacted 6/28/68; effective 4/l/68. repealed. Top tax rate on income Imposed a tax surcharge on is 10% with no distinction between earned and unearned income. individual income tax liability (4/l/68 - 6/30/70). 50% IRC long-term gains Tax surcharge imposed at annual exclusion adopted. rates of 7.5% beginning 4/l/68,5% in 1969 and 5% for 1970. Effective rate for 1970 is 2.5% (Jan. - June ).

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

436

Year

NATIONAL TAX JOURNAL

Now York State

1968 Chapter264 of the Laws of 1968. Enacted 5/14/68; effective 12/31/67.

Year

Tle first $50,000 of net capital gains eligible for alternative tax; the remainder is taxed at one-half the rate of ordinary income.

Chapter 1005 of the Laws of 1970. Enacted 5/20/70; effective I/l/70. State conformity to federal Tax Reform Act of 1969.

Add-on minimum tax imposed at 10% on total tax preference items including long-term gains less a $30,000 exclusion and less regular income tax liability.

Long-term gains exclusion treated as a tax preference item and subject to a 3% minimum tax. Deduction of $10,000 (single) and $20,000 (married) allowed in computing "minimum tax" liability. 1972 Chapter 1 of the Laws of 1972. Enacted 1/4/72; effective 1/l/72. 40% long-term capital gains exclusion. Add back 1/5th of federally excluded long-term gains. Not to exceed 10%. "Minimum ta)e'rate increased to 6%; deduction reduced to $2,500 (single) and $5,000 (married). Top tax rate on income increased from 14% to 15%. In addition, a tax surcharge imposed at a rate of 2.5 % in 1972, 1975 and 1976 increasing the effective tax rate from 15% to 15.375%. Chapter 70 of the Laws of 1978. Enacted 4/14/78; effective 1/l/78.

Federal

1969 Tax Reform Act of 1969. Enacted 12/30/69; effective 1/l/70.

Top tax rate on income increased from 10% to 14%. 1970

[Vol. XLI

Tax preferences in excess of $30,000 reduced the amount of earned income subject to maximum tax beginning 1/l/71. 1976

Tax Reform Act of 1976. Enacted 10/4/76; effective 1/l/77. Excluded portion of long-term gains subject to a 15% tax as a tax preference item under add-on tax, less the larger of a $10,000 exclusion or one-half of regular income tax liability. Tax preferences reduced the amount of earned income subject to maximum tax. Long-term gains holding period increased from 6 to 9 months for 1977 and from 9 to 12 months after 1977.

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

No. 31

FRANS

Year

SEASTRAND

New York State

Maximum capital loss deduction allowed to offset ordinary income increased to $2,000 in 1977 and to $3,000 in 1978. 1978

Chapter 1981. Enacted 1/l/81.

103 of the Laws of

Chapter Enacted

Chapter Enacted 1/l/87.

Act of 1978. 11/6/78; effective

Repealed alternative tax for tax year beginning 1/l/79. gains exclusion. Long-term gains increased to 60%.

29 of the Laws of 1985. 4/9/85; effective 1/l/86.

28 of the Laws of 1987. 4/20/87; effective

Top tax rate on capital gains imposed at the same rate as for earned income (8.75% in 1987 and 8.375% in 1988). State conformity to federal Reform Act of 1986. Repeals the long-term gains exclusion as a tax preference under the minimum tax.

Tax

exclusion

Add-on minimum tax for tax preferences (capital gains exclusion) repealed. Beginning 1/l/79, capital gains exclusion subject to a new alternative minimum tax if such tax exceeds regular tax liability. Alternative minimum tax imposed at graduated rates of 10, 20 and 25%.

Top tax rate on unearned income reduced from 14% to 13.5 % with an effective tax rate of 13.375% for 1985. 1987

Revenue Enacted 11/l/78.

5/15/81; effective

60% long-tern 1985

Federal

Year

Distinction made between earned and unearned income. Top tax rate on unearned income is 15% (1978) and 14% from 1979 through 1984 respectively. 1981

437

1981

Economic Recovery Act of 198 1. Enacted 8/13/8 1; effective 6/9/8 1. Top rate on unearned income is reduced to 50% beginning 1/l/82. Reduces minimum alterntive income in 10% rate $60,000 is

the top alternative tax rate to 20% on minimum taxable excess of $60,000. The between $20,000 and retained.

National Tax Journal, Vol. 41, no. 3, (September, 1988), pp. 415-38

438

Year

NATIONAL TAX JOURNAL

New York State

[Vol. XLI

Year

Federal

1982

Tax Equity and Fiscal Repsonsibility Act of 1982.

Enacted 10/19/82; effective 1/l/83. Alternative minimum tax is broadened to include more tax preference items and the exclusion allowed against the tax is increased to $40,000 (married joint) and $30,000 (single). Deficit Reduction Act of 1984. Enacted 7/18/84; effective 6/22/84. Reduced holding period on long-term gains from 1 year to 6 months. 1986

Federal Tax Reform Act of 1986. Enacted 10/22/86; effective 1/l/87. Repeals the long-term gains exclusion. Limits the top tax rate on long-term capital gains to 28%. However, taxpayers in the personal exemption and tax rate benefit phase-out ranges face a marginal tax rate of 33% in tax years after 1987. Removes the long-term gains exclusion as an item of tax preference under the minimum tax.