Regulating Capital Flows to Emerging Markets: An Externality View Anton Korinek∗ University of Maryland September 19, 2008 Abstract This paper analyzes the external financing decisions of emerging market economies that are prone to collateral-dependent financing constraints. We show that most forms of capital flows into such economies impose a macroeconomic externality that leads decentralized agents to take on too much systemic risk and makes the recipient country more vulnerable to financial instability and crises. Every capital inflow entails future outflows in the form of repayments, dividends, or profit distributions. In states of the world when financing constraints in an economy become binding, capital outflows necessitate an increase in the current account and a reduction in aggregate demand. This puts pressure on the exchange rate and triggers a financial accelerator mechanism, i.e. a mutual feedback cycle of depreciating exchange rates, deteriorating balance sheets, tightening financing constraints, and declining aggregate demand. Decentralized agents take prices as given and do not internalize that the capital outflows associated with their repayments contribute to the selling pressure on the country’s exchange rate, and therefore to the financial accelerator mechanism that is triggered in crisis states. As a result, they do not internalize the full social cost of capital inflows, they take on too much systemic risk, and they impose externalities on the rest of the economy. We illustrate how these externalities can be quantified for different categories of capital flows using historical data from Indonesia and we discuss policy measures that can restore social efficiency.

JEL Codes: Keywords:

F41, E44, D62, H23 capital market liberalization, international capital flows, externalities, systemic risk, financial crises

∗

The author would like to thank Viral Acharya, Alessandra Bonfiglioli, Phil Brock, Fernando Broner, Tiago Cavalcanti, Eric Fisher, Walt Fisher, Chris Gilbert, Olivier Jeanne, Laura Kodres, Enrique Mendoza, Carmen Reinhart, Joseph Stiglitz, and Carlos Vegh as well as conference participants at the CAF-FIC-SIFR Conference on Emerging Market Finance, the Cambridge Finance Conference on the IMF and Financial Crises, the CREI/Egon Sohmen Symposium, the FDIC/Cleveland Fed Conference on Financial Stability and seminar participants at the IIES Stockholm, the IMF and the University of Washington for helpful discussions and comments. Address for correspondence: 4118F Tydings Hall, University of Maryland, College Park, MD 20742, USA. Telephone number: +1 (917) 543-5237. Email contact: http://www.korinek.com/

1

1

Introduction

The emerging market crises that the world witnessed over the past quarter century have led researchers to re-evaluate the benefits and risks of capital market liberalization in developing countries. On the one hand, standard neoclassical models (see e.g. Obstfeld and Rogoff, 1995) suggest that free international capital flows increase the efficiency of the world allocation of capital. In particular, they should allow poor countries to increase their capital stock and thereby raise output and welfare (see Henry, 2007, for an excellent survey). During the 1990s, this view was strongly advocated e.g. by a number of researchers in the IMF (see Fischer, 1998) and led dozens of developing country governments to liberalize their capital account. On the other hand, a number of academics (see e.g. Rodrik, 1998; Stiglitz, 2002) have argued that capital market liberalization strongly increased the risk that an emerging market economy suffers a financial crisis, while the benefits it offered were questionable. Proponents of this view pointed out that the fundamental theorems of welfare economics that lay behind the view that capital market liberalization raised welfare hold only in economies that suffer from no other distortions. The typical emerging market economy is rife of market imperfections; hence restrictions on capital accounts can be an optimal policy in a second-best sense. However, this literature did not provide a detailed economic mechanism that would explain why the decentralized equilibrium in such an economy would be inefficient, and what exact forms of regulations would be warranted. This paper sets out to provide a theoretical foundation to this question. We show that decentralized agents do not internalize that their financing decisions give rise to financial accelerator effects, which play a key role in emerging market crises. This creates a macroeconomic externality that induces them (i) to undervalue the systemic risks posed by various forms of capital flows and (ii) to contract an excessive level of such flows. As a result, their economies are excessively vulnerable to financial instability and crises. We also show that well-targeted regulations can alleviate this distortion, induce decentralized agents to switch towards safer forms of finance, and offer emerging market economies the opportunity to enjoy the benefits of financial globalization without suffering the social costs imposed by frequent financial crises. The financial accelerator, and by implication the externality, arise from positive feedback effects between collateral-dependent financing constraints and depreciating exchange rates. Let us define situations in which an emerging market economy experiences an adverse shock that makes external financing constraints binding as financial crisis. In such states, repayments on financial obligations require that domestic agents cut back on consumption and investment, which reduces aggregate demand. Declin2

ing aggregate demand causes the exchange rate to depreciate,1 which constitutes a pecuniary externality: Atomistic agents take the exchange rate as given and do not internalize that it is affected by their financing decisions. However, since depreciations in the exchange rate deteriorate the balance sheet of other agents, the pecuniary externality has real effects in the form of tighter financing constraints for others in the economy. As a result, atomistic agents do not internalize the full social cost of liabilities that mandate repayments in constrained states of nature. An important condition for this externality to result in welfare losses is that the emerging market economy is in fact subject to aggregate risk. If international investors were risk-neutral and financial markets were complete, decentralized agents in the emerging economy would find it optimal to fully insure against aggregate shocks; financial crises would never occur, and the social optimum could be achieved.2 However, when capital markets are averse to some risk factors, atomistic agents in the emerging economy determine the optimal structure of liabilities by weighing off the private risk versus the required return on different forms of finance. Since they undervalue the social costs of payoffs in crisis states, they take on financial flows that entail too much systemic risk and impose an externality on the rest of the economy. When international capital markets are strongly risk averse to a particular state of the world, emerging market crises can arise from contagion, i.e. in the absence of any adverse domestic shock: if international investors receive high repayments in such states (for example, short-term debt confers the implicit option to not roll over the debt in the event of a global liquidity crisis), then the resulting ‘sudden stop’ in capital flows exerts pressure on the exchange rate and can trigger financial accelerator effects and a financial crisis. We construct a social pricing kernel that prices emerging market liabilities at their true social cost. (In analogy to traditional pricing kernels, which reflect how much private agents value payoffs across different states of the world, the social pricing kernel is a random variable that expresses how much a social planner values payoffs across different states of the world.) The difference between the private and social pricing kernels represents how much decentralized agents undervalue the social costs of statecontingent payoffs. We call this difference the externality kernel. In unconstrained states of the world, private and social pricing kernels coincide and the externality kernel is 1

In normal times, many emerging economies peg their exchange rates. However, as exemplified by Argentina in 2001/02, pegs typically cannot be maintained in case of large systemic shocks that lead to financial crises. 2 In fact, it can be argued that the existence of financial crises is proof that emerging markets do not have access to perfect and risk-neutral financial markets – otherwise they would be fully insured against all risk. See Korinek (2008a) for an elaboration of this point.

3

zero. In constrained states of the world, the social planner internalizes that payoffs are socially more costly than decentralized agents realize; the externality kernel is positive and grows larger the tighter financing constraints are. We show that the expected size of the externality imposed by a given liability can be calculated as the product of its stochastic vector of payoffs with the externality kernel. This can be used by policymakers to calculate the social costs imposed by capital flows of different forms, such as dollar debt, GDP-linked debt, local currency debt, portfolio investment, or foreign direct investment. For example, foreign currency-denominated debt, which mandates high payoffs in crisis states, is associated with large externalities; by contrast, foreign direct investment, which typically yields no profits during crises, is free of externalities. Our theoretical results are also consistent with empirical findings regarding the effect of different forms of capital flows on macroeconomic volatility and on the incidence of financial crises in emerging markets. For example, Calvo et al. (2004) and Levy Yeyati (2006) show that flows of foreign currency-denominated debt to emerging markets raise the risk of financial crisis and magnify macroeconomic volatility. Kose et al. (2007) find more generally that “portfolio debt [...] is not conducive to risk sharing.” On the other hand, Mauro et al. (2007) show “... that foreign direct investment and other non-debt creating flows are positively associated with long-run growth.” We can therefore provide useful guidance to policymakers on (i) whether measures against a particular form of finance are warranted and (ii) of what magnitude policy measures should be. Selective regulations, for example in the form of taxes or reserve requirements on risky forms of international capital flows, should make it possible for emerging market economies to enjoy the benefits of global financial integration while avoiding the costs imposed by recurrent financial crises.3 We illustrate how the discussed externalities can be quantified for different forms of capital flows using historical data from Indonesia and find that the resulting externalities (and optimal taxes) associated with dollar debt, local currency debt and equity portfolio inflows are 1.54%, 0.44% and 0.31% respectively of the value of the inflow. While the externality that we analyze stems not from the inflows of foreign capital, but from the effects of outflows when financial crises arise, we advocate that policy measures are imposed on inflows rather than outflows. In a rational expectations framework, both measures are equivalent. However, in practice regulations on inflows create a more predictable policy environment and avoid problems of time inconsistency. There 3

In contrast to e.g. Tobin (1978) the policy measures that we propose would apply only to risky forms of finance. In addition, they are motivated from a well-specified externality rather than a general concern about the volatility of international capital flows.

4

is also a role for policy to actively encourage capital inflows in the midst of a financial crisis: decentralized agents will generally undervalue the social benefits of capital inflows in mitigating crises and alleviating economy-wide financing constraints. Policy measures against the discussed externality are only effective if they affect the price of risky assets. We show that if private agents expect contingent transfer payments in crisis states (e.g. from the emerging market government or, indirectly, from international bodies), they will take on more risk to undo the effect, since the decentralized equilibrium with excessive risk taking constitutes their private optimum.4 While the model in our paper is set in a rational expectations framework, it is often argued that real-world market participants did not fully expect the severe movements of macroeconomic variables that occurred during financial crises. We can illustrate that errors in expectations regarding the severity of a financial crises entail large social costs, since the financial accelerator magnifies the effects of agents’ misallocations on consumption. By contrast, errors in expectations in normal times impose only small welfare costs, since the effects of misallocations on consumption can be smoothed over time when borrowing constraints are loose. In methodology, our work contributes to the literature on the financial accelerator, which has often been invoked as an important mechanism to describe financial crises (see e.g. Fisher, 1933; Kiyotaki and Moore, 1997; Bernanke et al., 1999; Krugman, 1999; Mendoza, 2006). So far little attention has been paid to the constrained welfare implications of such accelerator effects, in particular to the ex ante social efficiency of financing decisions. We show that if international capital markets are risk-averse, the financial accelerator creates an externality that induces individual firms to take on excessive risk.5 Our work is also related to the literature on excessive risk-taking in emerging markets. Many authors argue that firms take on excessive risk due to moral hazard, i.e. in order to take advantage of bail-out guarantees (see e.g. Krugman, 1998; Schneider and Tornell, 2004). However, as argued by Eichengreen and Hausmann (1999), risky forms of finance are pervasive even among firms that are unlikely to be bailed out, and in most financial crises government bailouts are not sufficient to cover most of the firms 4

While this can give rise to behavior that is observationally similar to moral hazard, there is no asymmetric information involved in the optimization problem of decentralized agents. 5 In earlier research (Korinek, 2008b), we have analyzed the relative desirability of local currency versus dollar debt in a framework with a similar distortion and discussed how to design an unremunerated reserve requirement on dollar debt to restore efficiency. The current paper, by contrast, analyzes the social efficiency of any form of capital inflows in a more general Arrow-Debreu framework with complete asset markets. We show that any debt flow, even if denominated in local currency debt, imposes a negative externality on the recipient country.

5

that went bankrupt. Eichengreen and Hausmann (1999) propose instead that emerging market economies simply do not have access to contingent forms of finance, which they term ‘original sin.’ However, as shown in Reinhart and Rogoff (2008), episodes of ‘original sin’ are typically temporary in the aftermath of a country experiencing financial distress. Another explanation by Caballero and Krishnamurthy (2003) argues that the interaction between frictions in international and in domestic financial markets induces agents in emerging markets to take on too much dollar debt. Our paper presents an alternative and complementary view, which differs along the following four dimensions: First, our result relies on a single market friction – collateraldependent borrowing constraints that limit access to international financial markets. The resulting fluctuations in the availability of external finance from international investors has been viewed as a key factor of financial instability in emerging markets by the literature on third generation crises (see e.g. Krugman, 1999; Chang and Velasco, 2001). We can therefore provide a unified theory of the mechanism of financial crises and the reasons for socially excessive exposure to crisis risk. Second, our analysis examines the efficiency of a multitude of different financial liabilities – not only dollar debt. Third, Mendoza (2006) has demonstrated that the financial accelerator effects that generate our externality result can quantitatively account for the evolution of macroeconomic variables in emerging market financial crises. This makes our findings more applicable for quantitative policy analysis. Fourth, note that in Caballero and Krishnamurthy (2003), a Pareto improvement can be enacted only by an all-powerful social planner who can engage in transfers from domestic borrowers to domestic lenders.6 In our paper, by contrast, a Pareto improvement can be attained by a constrained social planner by limiting excessive risk-taking. The remainder of the paper is structured as follows. Section 2 introduces a stylized two-period model of a small open emerging market economy in which a financial accelerator mechanism is triggered in low output states. We demonstrate that decentralized agents value liquidity in such crisis states less than a social planner would. In section 3 we add one time period before the crisis potentially occurs and analyze the ex-ante financing decisions of decentralized agents and the social planner. We show that decentralized agents generally contract a socially excessive level of repayments in crisis states since they do not internalize that repayments in such states contribute to the selling pressure on the exchange rate. Section 4 analyzes first- and second-best policy measures to correct the distortion. Section 5 concludes. 6

They address this issue by assuming that each agent has a one-half probability of being borrower or lender ex ante; in expectation a limit to dollar borrowing therefore makes all agents better off.

6

2

Benchmark Model of Financial Accelerator

This section analyzes a stylized two-period model of a small open emerging market economy that is subject to collateral-dependent financing constraints in the style of e.g. Mendoza (2006). We show that when financing constraints bind, a financial accelerator mechanism is triggered: lower borrowing capacity forces agents to increase repayments, cut back on spending and reduce aggregate demand, which depreciates the country’s exchange rate. The decline in the exchange rate in turn lowers the value of domestic collateral, reducing the agent’s borrowing capacity even further and leading to a downward spiral of depreciating exchange rates, falling collateral values, tightening financing constraints and contracting demand. While the equilibrium allocations of decentralized agents and the social planner coincide in this simplified model, we can show that decentralized agents value liquidity in crisis states when the financial accelerator is triggered less than a social planner.

2.1

Analytical Environment

We analyze a small open economy that consists of a continuum of mass 1 of identical representative agents. There are two goods in the economy, a tradable good T which can be traded with large international investors and which is the numeraire good, and a non-tradable good N with a relative price pN , which is also a measure of the real exchange rate.7 The economy spans over two time periods indexed t = 1 and 2. At the beginning of time the economy’s aggregate state of productivity ω ∈ Ω is realized.

2.2

Domestic Agents

Domestic agents derive utility from the consumption of tradable CT and non-tradable goods CN in periods 1 and 2 according to the utility function 1

σ

1+σ 1+σ CN,t U = u(C1 ) + βu(C2 ) where Ct = CT,t

(1)

where u is a standard neoclassical utility function, β is the agent’s discount factor, and 1 σ and 1+σ are the shares of tradable and non-tradable goods in the consumption 1+σ 7

We chose to model the economy’s exchange rate as a real exchange rate for analytical simplicty. More generally, any model in which the exchange rate depreciates in crises, i.e. in response to strong negative shocks to aggregate demand, will yield our externality result. Note that this property is generally the case in emerging markets, even under pegged exchange rate regimes, which typically collapse in response to strongly negative shocks, as illustrated e.g. by the Argentine crisis in 2001/02.

7

index Ct . This implies that σ is the ratio of the value of non-tradable consumption to tradable consumption, which is constant given the Cobb-Douglas aggregator. We assume that agents are born with a an initial amount of wealth W1 (which can be negative because of debts taken on in earlier periods). They need to invest I¯ units of ω ¯ tradable goods in period 1. As a result, they receive an endowment of (YT,t , YN ) in both ω periods 1 and 2, where YT,1 depends positively on the aggregate state of productivity ω, and for simplicity YT,2 = Y¯T and Y¯N = 1 are assumed fixed.8 Agents can borrow by selling an amount B1 of bonds to international investors, in period 1 in exchange for a repayment of $1 in period who buy each unit at price $1 R 2. We assume without loss of generality that domestic agents’ discount factor and international lenders’ interest rate are such that βR = 1. Domestic agents can sell bonds up to a borrowing limit K ω , which depends on the value of their collateral. We follow Mendoza (2006) in assuming that the maximum borrowing capacity K ω is a fraction κ of the agent’s income in period 1:9 ω B1ω ≤ K ω = κ YT,1 + pωN,1 Y¯N

�

(2)

This constraint reflects that lower income and net worth reduce the stake that an agent has in his project and therefore amplify the principal agent problems that arise in lending relationships (see e.g. Stiglitz and Weiss, 1981). As a result, lenders reduce the amount of funds they supply to borrowers whose income and net worth decline.10 We identify periods when the financing constraint on the representative domestic agent is binding as financial crises. In the following subsections it will become clear that this is a good characterization of crises. 8

This assumption reflects that production factors cannot be re-allocated between the two sectors of the economy in the short run. Our insights would be unaffected if we endogenized investment and introduced a lag between investment and production. 9 To ensure that the borrowing constraint is relevant, we make the assumption κσ < 1. This guarantees that the appreciation of the exchange rate that results from a one dollar capital inflow raises the borrowing capacity of the country by less than one dollar. Otherwise the borrowing constraint would never be binding. 10 While this constraint is not derived from an optimal contract setting here, we would like to point out that our results hold in any framework where an agent’s borrowing capacity increases in his net worth, as is typical in the literature on financing constraints. We can show, for example, that our externality result continues to hold in the presence of financing constraints that arise from imperfect pledgeability as in Holmstr¨ om and Tirole (1998).

8

The domestic agent’s optimization problem can then be denoted as max

2 X

ω ,C ω {CT,t N,t ,B1 }

t

�

1 1+σ

σ 1+σ

�

β u CT,t CN,t

(3)

t=1

ω ω ω s.t. I¯ + CT,1 + pωN,1 CN,1 = YT,1 + pωN,1 Y¯N + W1 + B1ω ω ω CT,2 + pωN,2 CN,2 = Y¯T + pωN,2 Y¯N − B1ω R � ω + pωN,1 Y¯N B1ω ≤ κ YT,1

2.3

Definition of Equilibrium

We can characterize the decentralized equilibrium in the described emerging market economy for a given ω as ω ω • an allocation (CT,t , CN,t , B1ω ) and

• a price pωN,t for t = 1, 2 • which maximize agents’ optimization problem (3) • which clear markets for both time periods: ω = Y¯N = 1 – for non-tradable goods: CN,t ω ω + B1ω + I¯ = YT,1 – for tradable goods: CT,1 ω = Y¯T − B1ω R CT,2

2.4

Equilibrium in the Non-tradable Sector

The first-order conditions of the agent’s maximization problem with respect to nontradable consumption in periods 1 and 2 pin down the relative price of non-tradables, i.e. the real exchange rate in the described economy. pωN,t = M RS = σ ·

ω CT,t ω = σCT,t ω CN,t

(4)

ω where we used the market-clearing condition for non-tradable goods CN,t = Y¯N = 1 in the last step. For simplicity, the endowment and the consumption of non-tradable goods are always fixed in this economy. As a result, fluctuations in aggregate demand take the form of fluctuations in tradable consumption and entail corresponding movements in the relative price of non-tradables. In particular, a decline in aggregate demand, e.g. ω a fall in the endowment of tradable goods YT,1 or a decline in borrowing B1 depreciates the exchange rate.

9

Note that this is a standard pecuniary externality, i.e. the mechanism by which the market reaches equilibrium, and typically has no welfare implications. However, in the described economy the valuation of agents’ collateral depends on the level of the exchange rate. When financing constraints are binding, a depreciation in the exchange rate reduces the value of collateral, which reduces agents’ borrowing capacity K and forces them to cut back on borrowing. In other words, when financing constraints are binding, the pecuniary externality can become a real externality.

2.5

Equilibrium in the Tradable Sector

Having solved for equilibrium in the non-tradable goods sector, we can simplify our notation of the agent’s optimization problem by expressing the utility function purely σ 1 in terms of tradable goods uT (CT ) = u(C 1+σ Y¯ 1+σ ). This results in the following LaT

N

grangian: � ω � DE ω ω ω L = uT (CT,1 ) + βuT (YT,2 − B1ω R) − µω CT,1 + I¯ − YT,1 − W1 − B1ω R − ω ω

CT,1 ,B1

� �� ω − λω B1ω − κ YT,1 + pωN,1 Y¯N

(5)

where µω is the shadow value of liquidity (or wealth) in period 1, and λω is the shadow value of relaxing the financing constraint. We can denote the first-order conditions of this problem as follows: ω ω FOC(CT,1 ) : µω = u0T (CT,1 ) ω FOC(B1ω ) : µω = βRu0T (CT,2 ) + λω

(6) (7)

Loose Financing Constraints When the agent’s collateral is sufficient so that financing constraints are loose, λω = 0 ω and the two first-order conditions reduce to the standard Euler equation u0T (CT,1 )= 0 ω βRuT (CT,2 ). Agents choose their borrowing such as to perfectly smooth consumption across both time periods. This is depicted graphically in figure 1. To the right of the threshold ω ˆ , financing constraints are loose and agents can smooth perfectly. Consumption in both periods ω 1 and 2 is the average of the levels of output YT,1 and Y¯T,2 in periods 1 and 2 (left panel). As a result, desired borrowing B1ω is a declining function of the state of productivity ω. On the other hand, the maximum amount that an agent can borrow K ω rises in the state of productivity (right panel). This is because higher tradable income and consumption appreciate the exchange rate, which increases the value of the do-

10

ω YT,1 ω CT,1

Kω

YT,2

B1ω

ω^

ω

ω^

ω

Figure 1: Output and consumption (left panel), and desired borrowing and financing constraint (right panel) as a function of the state of productivity ω

mestic agent’s collateral. The threshold ω ˆ is defined as the value of ω where financing constraints are just marginally binding. Binding Financing Constraints and Financial Accelerator Effect On the other hand, when financing constraints in the economy are binding, the shadow value on the constraint is positive, λω > 0, and agents cannot smooth their income ω ω across time, i.e. u0T (CT,1 ) > βRu0T (CT,2 ). In the described economy, agents borrow the ω ω maximum amount possible B1 = κ(YT,1 + pωN,1 Y¯N ), and this pins down their consumpω ω tion allocations CT,1 and CT,2 . The resulting shadow price on the borrowing constraint ω 0 ω 0 ω is λ = uT (CT,1 ) − βRuT (CT,2 ), which is the wedge in the agent’s Euler equation. Note that any aggregate shock is now amplified by the financial accelerator mechanism. Assume e.g. that we start in an equilibrium with binding financing constraints and analyze the effects of a small reduction in wealth W1ω . The first effect is that, for a given borrowing capacity K ω , the decentralized agent has to contract his spending ω on consumption CT,1 by an equivalent amount. However, this depreciates the exchange rate (4), and the depreciation in turn reduces the value of the non-tradable collateral of all agents and tightens the financing constraint (2). A tightening in the financing constraint forces the agent to cut back further on his consumption, and the result is a feedback cycle of falling exchange rates, tightening financing constraints, and decline in consumption. Note that all these phenomena, including the rise in the current account that mirrors the decline in borrowing, are typical features of financial crises (Calvo et al., 2004). In figure 1 aggregate states where financing constraints bind are depicted to the left of the threshold ω ˆ . The left panel shows that consumption reacts much more 11

strongly to marginal changes in productivity than in unconstrained states, reflecting the amplification effects of the financial accelerator mechanism. The right panel depicts the threshold where financing constraints become binding as the level of productivity where desired borrowing B1ω and the constraint K ω coincide. The maximum amount of borrowing K ω declines more sharply when financing constraints bind because the financial accelerator strongly depreciates the exchange rate in such states.

2.6

Social Planner’s Equilibrium

The social planner internalizes the effects of her intertemporal consumption allocations on exchange rates. She realizes that higher tradable consumption in period 1 appreciates the exchange rate, which in turn loosens the financing constraint K ω . Analytically, we can express this by substituting the equilibrium condition for the exchange rate (4) into the decentralized agent’s maximization problem (5) to obtain � ω � SP ω ω ω L = uT (CT,1 ) + βuT (YT,2 − B1ω R) − µω CT,1 + I¯ − YT,1 − W1 − B1ω − ω ω CT,1 ,B1

� �� ω ω − λω B1ω − κ YT,1 + σCT,1 This results in the following first-order conditions for the social planner, where we index the shadow prices by ‘SP’ to distinguish them from the values prevailing in the decentralized equilibrium, indexed by ‘DE’: ω ω FOC(CT,1 ) : µωSP = u0T (CT,1 ) + κσλωSP ω FOC(B1ω ) : µωSP = βRu0T (CT,2 ) + λωSP

Let us compare these two conditions with the decentralized agent’s first order conditions (6) and (7). When financing constraints are loose and λωSP = 0, it is easy to see that both equilibria lead to identical allocations that involve perfect consumption smoothing. When financing constraints are binding, both the social planner and decentralized ω agents choose to borrow the maximum amount possible B1ω = K ω = κ(YT,1 + pωN,1 Y¯N )., and the resulting wedge in the Euler equation is identical in both equilibria. However, ω as the first-order condition on CT,1 illustrates, the social planner’s valuation µωSP of liquidity in period 1 is higher than that of the decentralized agent in (6). This is because she realizes that increasing period 1 wealth would not only raise consumption, but would also appreciate the exchange rate, increase the value of domestic collateral and relax the financing constraint, thereby leading to a superior intertemporal allocation of consumption. By the same token, the social planner perceives binding borrowing constraints to be more costly, as captured by her shadow price on the constraint λωSP . Combining the 12

Valuation of payoffs Social valuation Private valuation

ex ity al rn te

Output shock Yω

binding borrowing constraints

two first-order conditions above yields that λωSP

ω ω ) ) − βRu0T (CT,2 u0T (CT,1 λω = DE = 1 − κσ 1 − κσ

(8)

1 >1 The social planner’s valuation of relaxing collateral constraints is by a factor 1−κσ higher than that of decentralized agents. This is because a one unit exogenous relaxation of the constraints has amplification effects of κσ in round two, which in turn yield an amplification of (κσ)2 in the next round and so on, and summing up these terms gives 1 1 + κσ + (κσ)2 + · · · = 1−κσ .

Proposition 1 (Undervaluation of Liquidity in Crises) In crisis states (when financing constraints are binding), the social planner values liquidity more highly than decentralized agents µωSP > µωDE , since she internalizes the financial accelerator effects arising from the constraints.

3

Optimal Financing Decisions

In the simple model that we have analyzed so far, the private and social valuations of liquidity differed, yet this did not introduce any inefficiency into the real allocation of resources. The reason was that when financing constraints were binding, decentralized agents simply borrowed the maximum amount they could and did not effectively have any optimization problem to solve. This section analyzes the implications of the mis-valuation of liquidity for the ex ante financing decisions of decentralized agents. For this purpose, we add to the problem 13

of the previous section another time period t = 0, in which decentralized agents need ω to invest I¯ while facing uncertainty about what aggregate state of productivity YT,1 will be realized in the next period. Agents can finance themselves in period 0 using a complete set of Arrow-Debreu securities. We show that in general, their under-valuation of liquidity leads agents to insure insufficiently against crisis states in which financing constraints are binding. In other words, they take on too many dangerous forms of finance and expose their economy to excessive risk from a social point of view. Analytically, this section assumes that domestic agents are born in period 0 with wealth W0 . They need to raise I¯ units of tradable goods for investment so as to produce output in period 1. They can finance this by using their initial wealth and by selling the amounts B0ω of Arrow-Debreu securities that each pay off one unit in state ω of period 1. International investors buy these securities at a price of M0ω each in period 0. In other words, their period 0 value of a one unit payoff in state ω of period 1 is M0ω . By implication the random variable M0ω represents the pricing kernel of international investors. The total amount of finance that domestic agents raise by selling a statecontingent bundle B0ω of Arrow-Debreu assets is E[B0ω M0ω ]. For example, if domestic agents promised a non-contingent payoff of one unit, we would set B0ω ≡ 1 and find that the risk-free interest rate satisfies RE[M0ω ] = 1. More generally, the budget constraints for periods 0 and 1 are I¯ = E[B0ω M0ω ] + W0 ω ω CT,1 + B0ω + I¯ = YT,1 + B1ω

3.1

(9) (10)

Decentralized Period 0 Financing Problem

We can then extend the formulation (5) of the optimization problem of decentralized agents with the terms describing the problem of period 0 financing as � � � DE ω ω ω ¯ − W0 − M ω B ω L = E u (C ) + βu (Y − B R) − ν I T T T,1 T,2 1 0 0 ω ω ω B0 ,CT,1 ,B1

�� � ω � � ω ω − µω CT,1 + B0ω + I¯ − YT,1 − B1ω − λω B1ω − κ YT,1 + pωN,1 Y¯N where ν is the shadow price of period 0 liquidity. While the first-order conditions on ω CT,1 and B1ω remain unchanged from (6) and (7) in the previous section, the additional first-order condition on B0ω is FOC(B0ω ) : µωDE = M0ω · νDE = M0ω · RE[µωDE ]

(11)

In the second step we used the expression νDE = RE[µωDE ], which follows from the same first-order condition by taking expectations. It states that the shadow price of period 14

0 liquidity is simply the discounted expected shadow price of liquidity in period 1. Let us define the pricing kernel of domestic agents as D0ω =

ω βu0 (CT,1 ) βµωDE = ω ω 0 E[µDE ] E[u (CT,1 )]

(12)

where the subscript DE emphasizes that the shadow prices µωDE in the expression are evaluated in the decentralized equilibrium. The first-order condition (11) entails that decentralized agents issue Arrow-Debreu securities up to the point where their relative marginal valuation of liquidity in period 1 coincides with the relative marginal valuation of payoffs of international investors, or where the pricing kernels of domestic agents and international investors coincide: M0ω µωDE = E[µωDE ] E[M0ω ]

3.2

or

D0ω = M0ω

(13)

Social Planner’s Period 0 Financing Problem

By the same token, we can express the social planner’s optimization problem using the following Lagrangian: � � � SP ω ω ω ¯ − W0 − M ω B ω L = E u (C ) + βu (Y − B R) − ν I T T T,1 T,2 1 0 0 ω ω ω B0 ,CT,1 ,B1

� ω � � �� ω ω ω − µω CT,1 + B0ω + I¯ − YT,1 − B1ω − λω B1ω − κ YT,1 + σ · CT,1 As in the previous section, the only difference between the two problems is that the social planner recognizes that the exchange rate is endogenous, i.e. that pωN,1 Y¯N = 1−σ ω · CT,1 in his formulation of the borrowing constraint. Hence he internalizes feedback σ effects from aggregate consumption to the exchange rate and the valuation of collateral. ω The first order conditions to this problem on CT,1 and B1ω are unchanged from the ones in section 2.6, and the one on B0ω is identical to decentralized agents’ first order condition in (11). In analogy to the pricing kernel of decentralized agents above, we denote the social planner’s shadow prices by the subscript SP and we define the social pricing kernel S0ω as � 0 � ω ω ω β u (C ) + λ βµ T T,1 SP SP S0ω = = (14) ω E[µωSP ] E[u0T (CT,1 ) + λωSP ] The social pricing kernel therefore represents the period 0 social cost of a repayment of one unit of tradable goods to foreign investors at time 1 in state ω.

15

3.3

Equilibrium Period 0 Financing Decisions

Risk-Neutral International Capital Markets If international capital markets are risk-neutral, their pricing kernel is a constant, i.e. M0ω = 1/R ∀ω. Given that risk markets are complete, international investors would ω then provide insurance against the domestic productivity shock YT,1 at zero cost. Since the utility function of domestic agents is concave, both decentralized agents and the social planner would take advantage of this opportunity by fully insuring against the ω shock YT,1 . Proposition 2 (Full Insurance) If international capital markets are risk-neutral, the ex ante financing decision of decentralized agents in economies that are prone to financial crises entail full insurance against aggregate shocks, and they are socially efficient. Even though decentralized agents and the social planner put a different value on liquidity in period 1 when financing constraints are binding, they both agree that the optimum entails full insurance. Their equilibrium allocations are therefore identical. In fact, when all shocks are insured away, it is likely that financing constraints will be loose in all states of nature, implying that the decentralized and the social valuation of liquidity coincide. Risk-Averse International Capital Markets On the other hand, if international capital markets are risk-averse so that M0ω is a non-degenerate random variable, then the choice of B0ω for the different states of the nature ω involves a risk-return trade-off. While our analytical results hold for any general specification of M0ω , we will focus on the case that international capital markets are on average averse to emerging market ω risk. In that case, M0ω and YT,1 are negatively correlated, i.e. capital markets value payω ω offs relatively highly (M0 high) when the productivity shock YT,1 is low and vice versa. While we assumed that the economy we examine is small compared to international capital markets, we believe it is reasonable to characterize international investors as risk averse towards the emerging market economy: First, many of the shocks to the tradable sector in emerging market economies are correlated with global factors. One example are fluctuations in commodity prices, which are driven by the global business cycle. Another example are exchange rate depreciations in competing emerging markets, which often play a role in the propagation of financial crises (‘contagion’) across countries. Secondly, as we observed above, if international capital markets were neutral

16

towards emerging market risk, then decentralized agents could insure their economies costlessly against all aggregate shocks. This is clearly counter-factual.11 Let us compare the insurance decision B0ω for state ω of a decentralized agent (subscript DE) and of the social planner (subscript SP ). If risk aversion among international investors is sufficiently small that decentralized agents decide to insure to the point that they will never face binding financing constraints, or if financing constraints are sufficiently loose that they never bind in the decentralized equilibrium, then λω = 0 ∀ω. As a result, the decentralized equilibrium is socially efficient and coincides with the social planner’s optimum. Proposition 3 (Loose Financing Constraints) If financing constraints in the decentralized equilibrium are always loose, then the decentralized equilibrium is socially efficient. Analytically, we can see that µωDE = µωSP for all ω since λω = 0. Since financing constraints are always loose, there are no financial accelerator effects in such an economy, and no externalities arise. On the other hand, in an emerging economy where insurance is too expensive to avert binding financing constraints in some states of the world, this result no longer holds. It is easy to see that E[µωDE ] < E[µωSP ] as long as there are some states of the world in which financial crises occur, since the social planner accounts for the role of higher period 1 consumption in alleviating financing constraints in her valuation of period 1 liquidity µωSP in constrained states ω. ω ω In unconstrained states, µωDE = u0T (CT,1 ) and µωSP = u0T (CT,1 ), but the denominator on the left-hand side of (13) is higher for the social planner. For condition (13) to hold, the social planner has to contract higher repayments in state ω than the decentralized ω agent, implying a higher marginal product of consumption u0T (CT,1 ). This captures that the social planner repays more in unconstrained states of nature so as to save liquidity for crisis states. On the other hand, in crisis states when financing constraints are binding, µωSP = ω u0T (CT,1 )+λω κσ. For condition (13) to hold, the social planner has to contract fewer reω payments in such constrained states12 , which raises consumption CT,1 , thereby lowering 0 ω both the marginal product uT (CT,1 ) and the tightness of financing constraints λω . Proposition 4 (Binding Financing Constraints) If domestic agents do not fully insure against binding financing constraints, their ex ante financing decisions involve 11

For a more extensive discussion of this observation see Korinek (2008a). More precisely, because of the change in the denominator on the left-hand side of condition (13), the social planner would also increase his repayments when λω is positive but very close to zero, so as to save funds for other states of nature where financing constraints are more costly. 12

17

too little insurance against financial crises. This makes crisis in the economy more severe and increases macroeconomic volatility. As this result illustrates, financial crises in our framework do not originate exclusively from domestic shocks. Instead the degree of risk aversion in international markets plays a crucial role in triggering binding constraints in an emerging market economy. In fact, we can show that financial crises can arise in the absence of any domestic shocks, i.e. purely as a result of international risk aversion. This can be interpreted as contagion. Assume that output in an emerging market economy is always constant, but that there is a state of nature ω to which international lenders are strongly averse, i.e. M0ω is extremely high in that state. Following equilibrium condition (13), decentralized agents in the emerging market economy will sell a large amount of bonds contingent on that state, entailing a large payment to international investors and little wealth left for ω domestic consumption, i.e. a high u0T (CT,1 ). For a sufficient degree of international risk aversion, domestic agents will commit to repayments that make the financing constraint on the emerging market economy binding, triggering a financial accelerator effect and creating an externality. While we have not explicitly modeled the maturity structure of an emerging economy’s external debts, a typical example of capital flows that are contingent on such states is short-term debt. If international capital markets experience a crisis and require liquidity (high M0ω ), they will not roll over short term debts to emerging markets. The resulting capital outflows exert pressure on the exchange rate and deteriorate the balance sheets of borrowers, and if these effects are strong enough the financial accelerator can be triggered. This can lead to a financial crisis in the affected emerging market economy, even though it did not experience any domestic shock. Proposition 5 (Contagion) Assume there are states of nature in which international lenders withdraw finance from the emerging market economy and cause financing constraints to bind. Decentralized agents will under-insure against such states and will experience socially excessive volatility.

3.4

Importance of Rational Expectations

While the model presented in this paper is set in a rational expectations framework, it is often argued that in the real world, market participants are surprised by “unexpectedly” large movements in exchange rates and real variables during financial crises, i.e. that they did not have rational expectations. Our model allows us to shed some light on 18

why a failure of rational expectations is particularly costly in the context of financial crises. Assume as a starting point that the economy is in period 0 of the decentralized equilibrium, and that agents have rational expectations regarding all prices and quantities. Suppose there is a constrained state ω in which individuals’ expectations of the real exchange rate is suddenly perturbed by a noise dp, i.e. they are over-optimistic and predict the exchange rate to be pˆωN,1 = pωN,1 + dp in that state. They believe that this relaxes the borrowing constraint in state ω by dK ω = dp·κY¯N . Since the constraint was binding before the perturbation, they could now increase consumption by an identical amount. However, this would not be optimal: before the perturbation, decentralized agents had chosen to take on the risk of facing binding constraints in state ω, given the cost of insurance. The same considerations would make them undo the expected extra income from the perturbation, and they would issue an additional amount dB0ω = dK ω of Arrow-Debreu bonds in period 0 so as to restore the initial equilibrium. (Note that this additional bond issuance would not have a discernable effect on period 0 wealth, since we assumed the probability for each state to be infinitesimal.) When the crisis state ω ˆ is realized and agents realize the error in their expectations, consumption not only falls by the amount dB0ω , which would constitute the repayment on the new bond issues that were designed to undo the perturbation. Instead, the higher repayments are amplified by the financial accelerator effect, i.e. they lead to a decline in the exchange rate below the earlier equilibrium level pωN,1 , which depreciates borrowers’ collateral further, forces them to cut back even more on consumption and so forth. To find the total effect we substitute the borrowing constraint (2) and the equilibrium exchange rate (4) into the agent’s budget constraint (10) and obtain ω ω ω CT,1 = YT,1 − I¯ − B0ω + κσCT,1 and

ω dCT,1 1 = >1 ω dB0 1 − κσ

The total effect of the bond sale dB0ω is multiplied by this factor. In short, when borrowing constraints are binding, any small misallocation that arises from erroneous expectations or other biases is strongly amplified and has large welfare and efficiency effects. By contrast, when borrowing constraints are loose, then unexpected income dC ω 1 = 1+β � 1 and reducing the shocks can be smoothed over time, implying that dBT,1 ω 0 impact of biases in expectations on welfare. Proposition 6 (Welfare Costs of Expectational Errors) In constrained states, financial accelerator effects magnify the impact of misallocations resulting from expectational errors on consumption. As a result, the welfare costs of such errors are by an order of magnitude larger than in unconstrained states, when shocks to consumption can be smoothed over time. 19

4

Policy Implications

In the previous section, we analyzed the social efficiency of decentralized borrowing decisions. When the decentralized equilibrium is characterized by binding financing constraints, we found that private agents borrow too much in Arrow-Debreu securities contingent on crisis states, i.e. they under-insure against the binding constraints. In this section we relate this finding to capital flows in the real world. Every asset in the real world can be thought of as a bundle of Arrow-Debreu assets with appropriate weights. We can captures this in the following definition. Definition 1 A security X is a contract that obliges the issuer to make a state-contingent payment X ω to the buyer. Naturally, the greater the payoffs of a given security in crisis states, the larger the externality that the security imposes on the economy. For example, foreign currency denominated debts mandate a fixed payoff in terms of tradable goods across all states of nature, including those states in which financing constraints are binding. This implies a relatively large weight on states in which private agents undervalue the social costs of repayments. By implication foreign currency denominated debts create large externalities. By contrast, flows that take the form of foreign direct investment are unlikely to reap profits in low output states and are therefore unlikely to entail repatriations of profits, i.e. capital outflows, in crisis states. This implies that they create no or only very small externalities. In the remainder of this section, we first discuss first-best policy measures on how the externality that we identified can be corrected. Then we lay out what second-best policy measures are warranted if first-best measures cannot be satisfactorily implemented.

4.1

First-best Policy Measures

The externality in this paper arises as a result of a financial accelerator, i.e. because of the positive feedback effects in low states of the nature between capital outflows, falling exchange rates, and tightening financing constraints. Hence first-best policy measures would attempt to break this feedback mechanism. One way of doing so would be to correct the capital market imperfections that underlie the financing constraints. While welfare will unambiguously improve if borrowing constraints are completely abolished, it is difficult to predict a priori how a mere relaxation of the constraint as captured by an increase in κ would affect welfare, since the relationship between the tightness of constraints and welfare can be non-monotonic (Matsuyama, 2008). A policy measure that has consistently led to a reduction in the 20

volatility of international capital flows is improvements in the quality of domestic financial institutions (IMF, 2007). Another measure that can break the accelerator mechanism that unfolds during financial crisis would be to peg the country’s exchange rate. In the given model setup, one way of doing so would be to maintain a buffer of foreign reserves that is used to stabilize the domestic consumption of tradable goods. While emerging market economies have long engaged in the practice of pegging exchange rates (Calvo and Reinhart, 2002), their ability to maintain pegs in response to strong adverse shocks has traditionally been limited. Defending a peg during economically challenging times often requires a large amount of foreign reserves. In fact, many observers, e.g. Aizenman and Marion (2003); Durdu et al. (2007), argue that an important factor behind the unprecedented accumulation of foreign reserves in Asia in recent years is the attempt to insure against future financial crises and the associated exchange rate depreciations. Encouraging Capital Inflows There is a role for policy to actively encourage capital inflows during financial crises, i.e. when financing constraints are binding: decentralized agents will generally undervalue the social benefits of capital inflows in mitigating crises and alleviating economy-wide financing constraints. For example, individuals might be reluctant to sell equity at fire-sale prices, even though it would be optimal from a social point of view, since the associated capital inflow would support the exchange rate and mitigate the financial accelerator. In such a situation, government incentives to attract foreign capital would be socially beneficial.13 Government Transfers On the other hand, we can show that anticipated transfer payments to the private sector in constrained states of nature will be ineffective. Assume that the government commits to paying a state-contingent transfer T ω to decentralized agents. In constrained states, we assume that the transfer T ω > 0; furthermore the government imposes lump-sum taxes, i.e. a negative T ω < 0, in some high states of nature where constraints are loose so as to make the policy in expectation revenue-neutral with E[M0ω T ω ] = 0. We can then show the following result: Proposition 7 (Ineffectiveness of Anticipated Government Transfers) An anticipated state-contingent government transfer T ω with E[M0ω T ω ] = 0 will be undone by 13

However, if foreign owners are less efficient at managing domestic companies than domestic owners, fire-sales to foreigners can introduce inefficiencies of a different nature (see Acharya et al., 2008).

21

decentralized agents. The solution to the decentralized agent’s problem (5) is an optimal risk-return tradeoff. If the government provides an anticipated transfer T ω in state ω, the agent will sell a state-contingent bond in the same amount to undo the effects of the transfer, since the decentralized equilibrium with excessive risk-taking constitutes his private optimum. By our assumption E[M0ω T ω ] = 0, the government transfer will not affect the agent’s wealth. Therefore his equilibrium consumption allocations are identical to the allocations that we derived for the decentralized equilibrium above. Naturally, this result depends on the assumption that those agents who receive transfers have access to a complete set of Arrow-Debreu markets in order to undo the transfers. If there are some agents in the economy who do not have access to such markets (e.g. financially-constrained workers), then a government transfer to this group does have real effects and can mitigate the financial accelerator that is triggered during crises by expanding aggregate demand and mitigating the fall in the exchange rate. This has imporant implications for the design of fiscal stimuli that are effective against crises. When decentralized agents undo the effects of anticipated government transfers, the outcome is observationally similar to moral hazard. However, in the given problem there is no asymmetric information and hence no hidden action by domestic agents. Risk-taking in the emerging market economy is simply the optimal response to the risk aversion of international investors. Naturally, proposition 7 applies only to anticipated transfers. If a government transfer was unanticipated, it would have the desired positive effects. By the same token, if a transfer has been anticipated in the event of a crisis, then an unexpected decision to withholds the transfer can be extremely costly: in anticipation of the transfer private agents have taken on additional risk, making the crisis more severe.

4.2

Second-best Ex-ante Policy Measures

In the short to medium run, it is difficult for emerging market economies to reform in a way to alleviate all market imperfections and implement the first-best equilibrium. As a result second-best policy measures might be desirable. While the externality that is the subject of this paper arises not from the inflows of foreign capital, but from the effects of outflows during financial crises, it is advisable that policy measures are imposed ex ante on inflows rather than ex post on outflows. In a rational expectations framework, both measures would be equivalent. However, in practice, regulations on inflows create a more predictable policy environment and can avoid potential problems 22

of time inconsistency. In period 0, international investors supply finance to domestic agents at a price determined by their pricing kernel M0ω . In the unregulated decentralized equilibrium, doβu0 (C ω ) mestic agents adjust their portfolio so that their private pricing kernel D0ω = E[uT0 (CT,1 ω T T,1 )] ω equals the exogenous pricing kernel M0 of investors. In the given complete markets framework, the period 0 valuation PX of any asset X with payoffs X ω in period 1 is therefore identical for decentralized domestic agents and international lenders; we denote this price as PX : E[M0ω X ω ] = PX = E[D0ω X ω ] However, this condition does not account for the social costs that repayments in constrained states and the resulting exchange rate depreciations impose on the owners of domestic collateral. The social valuation PX∗ of a liability X with payoffs X ω is instead PX∗ = E[S0ω X ω ]

(15)

Accounting for the fact that capital outflows create negative externalities in constrained states, this social valuation is higher than the decentralized price PX demanded by international investors. Externality Kernel Let us assume the economy is in the social planner’s equilibrium and denote the difference between the social and the private valuation of liquidity in period 1 of that equilibrium, normalized by the expected private valuation, as the externality kernel τ ω : ω ω ) ) − βRu0T (CT,2 u0T (CT,1 µωSP − µωDE λωSP κσ τ = = κσ · · E[µωDE ] = 1 − κσ E[µωDE ] ω

(16)

where we employed equation (8) in the last step. The intuition of this expression is straightforward: the uninternalized social benefit of a one unit payoff in state ω is a relaxation of the borrowing constraint by κσ, which yields an increase in utility of � 0 � 1 ω ω by the financial uT (CT,1 ) − βRu0T (CT,2 ) that is in turn magnified by the factor 1−κσ accelerator. A social planner could make agents internalize the externality associated with capital inflows by imposing a tax that raises the cost of capital on each asset to its socially efficient level. The optimal tax on a unit payoff in state ω equals the externality kernel τ ω created by that payoff. By implication, the optimal tax t∗X on a given security X with contingent payoffs X ω is the expected product of the externality kernel with the vector of payoffs: t∗X = E [τ ω X ω ] 23

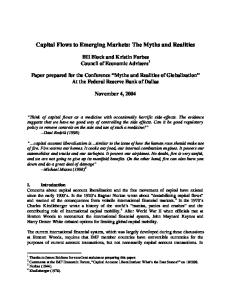

Valuation of payoffs Social valuation Private valuation

Payoff of assets

Dollar debt GDP-linked debt Local currency debt Portfolio investment FDI

Output shock Yω

Figure 2: Different forms of financing entail different repayments in different states of the world. Repayments in constrained states create an externality. The optimal tax on any particular flow can be calculated as the expected product of a given asset’s payoff vector with the externality kernel.

Figure 2 schematically shows both the private and social valuation of payoffs as a function of the state of the economy ω. Repayments in states when financing constraints are binding entail an externality of size τ ω , which is represented as the wedge between private and social valuation in the figure. In the lower panel we have schematically depicted the repayments on various forms of capital flows as a function of the state of the economy, from uncontingent dollar debt to foreign direct investment.

4.3

A Sample Calibration to the Case of Indonesia

Let us now perform a simple exemplary calibration of the externality kernel in Indonesia and derive the optimal tax on a number of different forms of capital flows to the country. We base our calibration on yearly historical data from the past two decades (i.e. 1988 – 2007).14 While we obtained our analytical results in a simple three period model, our calibration method uses only few structural assumptions and is therefore robust to a large number of different specifications of the financial accelerator mechanism that drives variations in external borrowing capacity (see e.g. Krugman, 1999; Schneider and Tornell, 2004; Mendoza, 2005; Mendoza and Smith, 2006). 14

Data from International Financial Statistics, IMF, 2008.

24

Before we proceed let us note three caveats. Firstly, since our calibration is based on historical data, it does not account for permanent changes in the structure of the economy. Second, if the vulnerability of an economy to financial crisis fluctuates over time, the externality kernel itself should be regarded as a time-varying random variable. We do not account for this an describe instead a permanent externality kernel.15 Third, we implicitly assume a yearly maturity for the assets we investigate. Debt flows that are of shorter (longer) maturity than one year would naturally impose larger (smaller) externalities. While these three concerns are certainly important for the practical implementation of capital flow regulations, it should be clear that the framework that we outline below can easily be adjusted to take these factors into account. Our main goal in this section is to conceptually illustrate how existing data can be used to quantify the externality kernel that we described. Our proposed calibration method proceeds in five steps: Step 1: Describe the set Ω of potential outcomes and identify constrained states: In our simple example, we define Ω = {1988, . . . , 2007} as the state space, which we assume representative for the Indonesian economy, i.e. we assign to each of these states a probability πω = 5%. During the described time span, the Asian financial crises of 1997/98 is the only incident in which a currency crises as defined by Frankel and Rose (1996) and a sudden stop as defined by Calvo (1998) took place. The crisis hit Indonesia in the second half of 1997, culminated in 1998 and a modest recovery started before the end of that year (Radelet and Sachs, 1998). For simplicity, we attribute the entire crisis to the calendar year of 1998. λω

Step 2: Quantify the tightness E[µDE ω ] of constraints: As described above, the tightness DE of constraints (as perceived by decentralized agents) is given by the wedge in the agent’s Euler equation, which we normalize by the decentralized agent’s expected marginal utility. Since real consumption data during the crisis episode is rather unreliable, we approximate the wedge by using the economy’s percentage decline in real GDP ∆y 1998 = 13.1% as a rough guide for the decline in consumption and the difference in relative marginal utilities that was experienced. Assuming agents have a CRRA utility function with a coefficient of relative risk aversion γ = 2 we can use a Taylor-approximation to calculate this wedge as λ1998 DE ≈ γ · ∆y 1998 = 26.2% ω E[µDE ] 15

This would be desirable for example as guidance for policymakers who want to impose constant tax rates on international capital inflows.

25

We assumed that no financial accelerator effects were at work in other years, i.e. λωDE = 0 for all other states of the world ω 6= 1998. Step 3: Estimate the strength of accelerator effects in constrained states: The factor κσ in equation (16) captures how strongly a given change in aggregate demand 1−κσ affects the tightness of borrowing constraints in our model at the margin, i.e. ω κσ = dK . For data availability reasons, we approximate this marginal effect 1−κσ dY ω using the average change in borrowing capacity as captured by the magnitude of the observed current account reversal (expressed as the change in the ratio of the current account to GDP CA/Y ) resulting from a change in aggregate demand by the economy’s growth rate ∆y in constrained states. This implies that ∆(CA/Y )1998 −7.1% dK 1998 ≈ = = .54 dY 1998 ∆y 1998 −13.1% κσ In our analytical model, the factor 1−κσ was constant across all states with financial accelerator effects, and in the given example, the state ω = 1998 is the only one in which binding constraints occurred. More generally, exchange rates can be non-linear functions of aggregate demand and constraints can be non-linear in κσ ω exchange rates. This can be captured by calibrating the magnitude of ( 1−κσ ) separately for each state ω based on the observed accelerator effects.

We can then express the externality kernel τ 1998 =

dK 1998 1998 ·λ = .54 · 26.2% = 14.1% dY 1998 DE

In other words, we estimate the externalities (i.e. uninternalized welfare costs) caused by any capital outflow from Indonesia in 1998 to be equivalent to 14.1% of the amount of the outflow. Step 4: Describe the payoff structure X ω of different assets in constrained states: In order to obtain the externalities caused by different forms of capital flows, we need to characterize the state-contingent payoffs of different asset classes in constrained states, i.e. in 1998 in our simple example. We have compiled a list of the realized gross returns of different asset categories measured in real domestic consumption units (i.e. local currency units deflated by consumer prices) in the first column of table 1. Step 5: Calculate the expected magnitude of the externality as E[τ ω X ω ]: The externality created by each payoff in a given state ω can simply be obtained as the realized real gross return X ω multiplied by the externality kernel τ ω . We have calculated this for Indonesia in 1998 in the second column of table 1. 26

Asset class Dollar debt GDP-indexed dollar debt CPI-indexed rupiah debt Rupiah debt Stock market index

Real gross return Externality in 1998 Optimal tax 218% 30.7% 1.54% 190% 26.8% 1.34% 100% 14.1% 0.71% 63% 8.9% 0.44% 44% 6.2% 0.31%

Table 1: Realized real gross return and externality of different asset categories in Indonesia, 1998.

Finally, since we assumed that the set Ω is representative of the long-run incidence of adverse shocks and binding constraints, we can express the expected magnitude of the externality by multiplying this number with the probability of the state π 1998 = 5%. The results are given in the final column of the table. Our results are the following: • Dollar debt is characterized by large repayments in constrained states of the world and is therefore one of the most dangerous forms of finance, imposing a large externality on the economy. Calibrated to the case of Indonesia, we found the size of this externality to be roughly 1.54% in the decentralized equilibrium. • GDP-linked debt is typically still denominated in foreign currency. Repayments are indexed to the state of the economy, which is supposed to mitigate fluctuations in aggregate demand. In our calibration we assumed the dollar interest rate on GDP-linked debt to equal the growth rate of the economy, i.e. -13%. While GDP-linked debt is a superior insurance instrument to uncontingent dollar debt, declines in exchange rates are typically much larger than declines in GDP during a financial crises, implying that local currency debt offers a far superior risk profile. • CPI-indexed local currency debt offers an acyclical repayment of 100% that is always constant in terms of domestic real consumption units. During emerging market crises exchange rates typically decline more strongly than inflation rises, implying that CPI-indexed debt protects borrowers from the pro-cyclicality of dollar denominated debts. • Local currency debt is inflated when a country’s price level rises, which is typically the case during emerging market crisis. This implies that the real value of local currency debts falls when the economy experiences a crisis – non-indexed local currency debt is an excellent insurance instrument. 27

• Portfolio investment in equity markets enhances risk-sharing opportunities significantly. When capital flows reverse, investors in emerging market equity markets see both the domestic currency value of their shares and the dollar value of the domestic currency drop sharply. This implies that portfolio investment entails only small repayments in constrained states and a very small negative externality. • Foreign direct investment (omitted in the table) is unlikely to entail profit repatriations in low states of nature, when profits are generally low or nonexistant. From this point of view, foreign direct investment is the one form of finance that does not create an externality. In fact, if a parent company injects additional liquidity into its emerging market subsidiary, then the resulting capital inflow entails a positive externality that would call for a subsidy, since capital inflows raise aggregate demand and mitigate the financial accelerator effect. Taxing risky assets makes decentralized agents internalize the externalities that their contracted repayments impose on the rest of the economy. Instead of direct taxes on capital inflows, equivalent policy measures such as unremunerated reserve requirements (URRs) or banking regulations can be employed in order to reduce the relative attractiveness of risky forms of finance and raise the relative demand for safer assets. As a result, the incidence and severity of borrowing constraints in the economy is reduced, macroeconomic volatility is lower, and social welfare is increased. The social planner’s interventions therefore constitute a Pareto improvement. In this context, it should be noted that most tax systems around the world enable entrepreneurs to deduct interest payments on debt from corporate (or individual) taxes. By contrast, dividend payments are subject to taxation. This introduces an important bias into the capital structure of firms that leads to excessive debt financing and therefore magnifies the externality that we discussed. The fact that agency problems are more severe for assets with highly state-contingent payoffs reinforces this problem. It is often argued (see e.g. Forbes, 2005) that capital account regulations are undesirable because they increase the cost of finance for private firms and they give rise to evasion. However, raising the private cost of capital inflows to the social cost is precisely the point of such regulations (just as environmental regulations raise the cost of pollution in order to discourage it). All regulation that imposes costly constraints gives rise to attempts to circumvent it (this includes e.g. banking regulation in developed countries). However, attempts to circumvent regulation are not a good reason to abolish it; rather it should encourage regulators to come up with better ways of enforecement.16 16

One proposal to enforce regulations on capital inflows is for example to make claims by foreign

28

4.4

Second-best Policy Measures During Crises

Capital Flight and Suspension of Convertibility In severe crises, when a country experiences strong capital outflows (i.e. states in which Bω B0ω > R1 ) and a financial accelerator is triggered and magnifies the resulting contraction, a policy measure of last resort might be to temporarily suspend international capital flows (see e.g. Krugman, 1999). Naturally, such a strong measure raises a number of difficult questions regarding adverse signaling and confidence effects. Ideally, the temporary suspension of capital account convertibility should take place in an international framework that (i) defines clearly under what circumstances the policy can be applied, i.e. in crises when strong financial accelerator mechanisms are at work, such as the East Asian crisis and that (ii) is supervised by an international organization. The goal of these conditions is to legitimize suspension of convertbility as a policy measure of last resort in extreme circumstances.17 However, our focus here is to discuss the merits of such a measure in alleviating the negative externality associated with capital outflows when financing constraints are binding and financial accelerator effects are at work. For this purpose, let us return to the model emerging market economy outlined in the previous section and assume that policymakers there have credibly committed to temporarily suspending capital account convertibility when a financial crisis beyond a defined magnitude occurs. The threshold for such action could be described e.g. as a quota on capital outflows. In a rational expectations framework international investors would anticipate this policy action when allocating their funds, i.e. they realize that any repayments from the emerging market economy can be subject to delay if they come due in the event of a financial crisis, and they adjust their required return accordingly. Since they are compensated for this risk, international investors would be indifferent to the policy measure. However, if no capital outflows from the economy are permitted in crisis times, no financial accelerator is triggered, and no externality arises. These benefits would have to be weighed carefully against the cost of completely preventing any risksharing between domestic agents and international lenders.18 creditors that have evaded capital controls unenforcable in court. 17 As described e.g. in Radelet and Sachs (1998), the downward spiral and the financial meltdown in the countries that experienced the East Asian crisis came to an end only when a temporary suspension of debt payments to international creditors was announced. In the case of Korea, this suspension and forced roll-over of debts was part of an agreement brokered by the US government. 18 Optimal risk-sharing entails that domestic agents also carry some risk, though less than what they would take on in the unregulated market equilibrium.

29

Quota on Capital Outflows One way of operationalizing such a policy measure would be a pre-defined quota on capital outflows. The externality kernel defined in (16) is linear in the shadow cost of borrowing constraints λω , which is approximately proportional to the outflow of capital from the economy, once the threshold where constraints become binding has been reached. This motivates a quota that allows capital to flow out of the country freely up to the point where borrowing constraints become binding, and that requires investors to either delay outflows or face a haircut once this threshold has been reached.

5

Conclusions

This paper showed that the financial accelerator effects that arise during emerging market financial crises create an externality that induces decentralized agents to take on excessively risky forms of finance and expose the economy to too much systemic risk. The resulting macroeconomic equilibrium exhibits socially excessive volatility, which takes the form of current account reversals coupled with sharp declines in consumption and the exchange rate when economy-wide financing constraints bind and accelerator effects are triggered. We described the basic building blocks of an optimal regulatory system for international capital flows in emerging market economies that makes decentralized agents internalize the systemic externalities they impose on the rest of the economy and that mitigates the risks of financial globalization. This should allow emerging market economies to enjoy the benefits of financial globalization while avoiding most of the associated downsides, thereby increasing social welfare. While this paper has analyzed the externality in one particular (and, admittedly, highly simplified) model, a similar mechanism arises more generally whenever an economy is subject to a financial accelerator mechanism whereby a decline in some macroeconomic price (such as the exchange rate, asset prices etc.) and a fall in output (e.g. because of balance sheet effects) mutually reinforce each other. The essential feature is that atomistic agents take macroeconomic prices as given, even if price declines have adverse macroeconomic effects. Aside from distorting financing decisions in an emerging market economy, the same externality also creates two distortions in their investment decisions: First, the undervaluation of liquidity in period 1 implies that agents do not internalize the full social cost of capital in period 0 when promising repayments in constrained states of period 1, for example whenever they issue debt. As a result, they generally invest too much. Secondly, when they evaluate the state-contingent payoffs of different investment projects, 30

they do not internalize the full social value of payoffs in constrained states of period 1. Therefore their investment will be biased towards excessively pro-cyclical projects. For example, an entrepreneur in a commodity-dependent economy who evaluates two investment projects, of which one is to invest more in the commodity-producing sector and the other to invest in a counter-cylical project, will not internalize the social benefits of risk diversification and might pick the pro-cyclical commodity project even if the social value of the other project is higher. These questions are the subject of our ongoing research.