Issue 3 Volume 15 October 2014

by PLASTICS INSTITUTE OF THAILAND

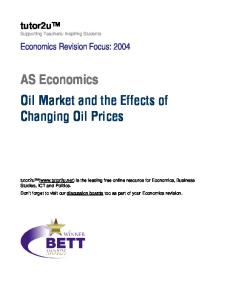

Oil and Plastic Resin Prices The average crude oil price in September 2014 was at 96.99 USD/barrel, down from the previous month 4.86 USD/barrel or down 4.77 percent. The crude oil prices started the downward trend since entering the third quarter. The ongoing factors pulling the crude oil prices down included the increased production level and export of crude oil of exporting countries such as Libya, resulting in increased supply or even the US dollar with its highest appreciation in four years.

However, the crude oil prices are expected to remain stable or slightly increase with the fourth quarter. The cold season in many areas will increase demand in the market. This is one factor that can balance the falling crude oil prices in the world market. The average prices of LDPE/LLDPE HDPE PP PET HIPS ABS as per October 2014 were 57.25, 56, 57.25, 44.5, 62, and 71 respectively. They generally changed according to the changes of oil prices. However, the plastic resin prices in the fourth quarter are expected to remain stable, similarly to the situation up till now until the end of the year.

Plastic Resin Prices compared to Crude Oil Prices

Resin (Baht/Kg)

Crude Oil Dubai (USD/Barrel)

120

140

100

120 100

80

80

60

60

40

40

LDPE/LLDPE

HDPE

PVC

PP

PET

HIPS

ABS

Sep-14

Crude Oil Dubai

Source: World Bank / Plastic Intelligence Unit, October 2014

-1-

Aug-14

Jul-14

Jun-14

May-14

Apr-14

Mar-14

Feb-14

Jan-14

Dec-13

Nov-13

Oct-13

Aug-13

Sep-13

Jul-13

Jun-13

May-13

Apr-13

Mar-13

Feb-13

Jan-13

Dec-12

Oct-12

Nov-12

Sep-12

Aug-12

Jul-12

Jun-12

May-12

Apr-12

0 Mar-12

0 Feb-12

20 Jan-12

20

ISSUE 3 VOLUME 15 October 2014

Import – Export of Plastic Resin Import September 2014

Export September 2014

As per September 2014, the import value of Thailand’s PE, PP, PVC, PS/EPS, ABS/SAN and PET amounted to 4,980 million baht, up from the previous month 7.1 percent. The import volume of 83,841 tons was up from the previous month. LDPE (H.S.390110) contributed to the highest import value of 981 million baht or 19.7 percent of the total import value of plastic resin. The import volume of 17,004 tons contributed to 20.3 percent of the total import volume of plastic resin.

As per September 2014, the export value of Thailand’s PE, PP, PVC, PS/EPS, ABS/SAN and PET amounted to 17,896 million baht, up from the previous month 7.4 percent. The export volume of 350,181 tons was up 8.3 percent from the previous month. HDPE (H.S.390120) contributed to the highest export value of 5,069 million baht or 28.3 percent of the total export value of plastic resin. The export volume of 97,797 tons contributed to 27.9 percent of the total export volume of plastic resin.

Source: Customs Department, October 2014

-2-

ISSUE 3 VOLUME 15 October 2014

Total: 41,619 Million Baht

Total: 162,741 Million Baht

Total: 121,625 Million Baht

Total: 41,030 Million Baht

Source: Customs Department, October 2014

-3-

ISSUE 3 VOLUME 15 October 2014

Production of Plastic Products In October 2014 or the first month of the fourth quarter, the production of plastic products remained similar to the production level in the third quarter with the Manufacturing Production Index of the plastic products at 166.24 points. The Capacity Utilization Rate in October 2014 still varied according to the direction of the Manufacturing Production Index. From the middle of the second quarter until the beginning of the fourth quarter, the Capacity Utilization Rate was at the average of approximately 60 percent. Overall, in 2014, the Capacity Utilization Rate of the plastic product industry decreased when compared to the previous year. The plausible explanation of the situation was the goods remaining in stock as producers slowed down their production and accelerated the release of the goods remaining in stock into the market, as well as the possible capacity expansion of producers, resulting in the high level of the overall production, whereas the capacity utilization remained stable or slightly decreased. However, it is estimated that the production level will decrease in the future, due to the seasonal production in the fourth quarter until the end of the year which is the relaxed period of the production of plastic products. The festivities including the year-end long holiday remain the additional factor that results in the decreased production level as well. Manufacturing Production Index and Capacity Utilization Rate of Plastic Products Index

Capacity Utilization

Manufacturing Production Index

Capacity Utilization

Source: Industrial Economics Information Center, Office of Industrial Economics, October 2014

-4-

ISSUE 3 VOLUME 15 October 2014

Import – Export of Plastic Products Import September 2014

Export September 2014

As per September 2014, Thailand’s import value of plastic products amounted to 12,102 million baht, up from the previous month 22 percent. Other articles of plastics (H.S.3926) had the import value of 4,998 million baht or 41.2 percent of the total import value of plastic products, followed by articles for packing of plastics (H.S.3923) with the import value of 1,633 million baht or 13.5 percent of the total import value of plastic products.

As per September 2014, Thailand’s export value of plastic products amounted to 10,759 million baht, up from the previous month 6.9 percent. The articles for packing of plastics (H.S.3923) had the export value of 3,175 million baht or 29.5 percent of the total export value of plastic products, followed by other films of plastics (H.S.3920) with the export value of 2,645 million baht or 24.5 percent of the total export value of plastic products.

Source: Customs Department, October 2014

มศุลกากร, ตุลาคม 2557

-5-

ISSUE 3 VOLUME 15 October 2014

Total: 93,770 Million Baht

Total: 17,879 Million Baht

Total: 91,065 Million Baht

Total: 26,749 Million Baht

Source: Customs Department, October 2014

-6-

ISSUE 3 VOLUME 15 October 2014

Production and Trade of Downstream Industries Fiscal Policy Office (FPO) revised the forecast of Thailand’s GDP this year down to 1.4 % from the previous forecast of 1.5–2.0 % due to the slower recovery of export and tourism as previously estimated. It was partly the result of the slowdown of the economy of trading partners especially Europe, coupled with the low prices of exports especially those of agricultural goods. GDP is estimated to grow approximately 2.9% during the second half of the year and to 4.1% next year thanks to the clearer picture of the political situations. Moreover, the stimulus package at the end of the year also promotes consumption and expands investment in the last quarter. The government spending remains an important factor promoting the continuous growth of the Thai economy this year. The Ministry of Commerce reported the increased import in line with the government’s investment plans. Thailand’s export grew for the first time in four months. The export value grew especially in agricultural goods such as rice and electronic goods which recovered in line with the economy of the trading partners. However, other factors affecting Thailand’s export still remain such as the reduced automobile export, the continuously reduced export value of rubber, and the slowdown of the Chinese economy. All these factors may affect the Thai export to grow slightly.

-7-

ISSUE 3 VOLUME 15 October 2014

- Automotive Industry -

- Food Industry -

In 2014, Thailand’s automotive industry slowed down since the beginning of the year. The automobile production fell due to the sluggish domestic demand as the result of the end of the first- car buyer policy, coupled with the slowdown of the local economy. The decreased production for export was the result of the sluggish economy of the trading partners all around the world. The export of passenger cars to Indonesia also declined by 40 percent as Indonesia increased the production capacity of domestic cars, resulting in the decreased export of cars and components in September by 13.6 percent. However, in the fourth quarter, there are good signs from the economic factors in the world including Thailand with slightly better trend so the export of cars starts to recover. The total production in September recovered and grew 17 percent from the previous month. The export of car components and accessories grew 11.4 percent, as well as the implementation of the Eco Car Project Phase 2. All these factors are expected to have positive impact on the automotive industry to recover by the end of the year.

National Food Institute reported that Thailand’s accumulative export value of food for 8 months in 2014 grew 15.48 percent and the export volume grew 12.10 percent. It is estimated to meet the export target of 1 trillion baht this year. The positive factors include the private sector’s investment expansion in convenience stores and export of processed food to regional markets such as CLMV, the beginning of Thailand’s tourist season from October until the middle of next year, and the government’s tourism package which promotes more consumption and spending for the public and the tourists. Therefore, the food industry is set to experience continuous growth. However, the factors that need to monitor in the future include the prices of some agricultural goods and Europe’s cancellation of GSP to Thailand which will affect tariff privileges from export next year.

-8-

ISSUE 3 VOLUME 15 October 2014

- Construction Industry In the beginning of 2014, the real estate sector was sluggish due to the political situations such as the cancellation of 2 trillion baht basic infrastructure development plans. The period with no appointment of the new BOI board also reduced investors’ confidence. In the first half of the year, NESDB reported the shrinkage of the construction production by 7.5 percent and the real estate sector by 1.2 percent. Although during the second half of the year the sales volume and business profits started to recover from the relaxed political situations, the entrepreneur confidence index for the third quarter of 2014, from the Real Estate Information Center, was 54.5 point, slightly down from the second quarter, due to investment, employment, and production costs. Nevertheless, the real estate sector is set for

the residential sale season in the fourth quarter. Other positive factors include the clearer drive of the government’s investment policies and the private sector’s continuous construction plans, whether the budget for renovation of the government sector’s buildings or the project to build Thailand’s new tallest building. The integration of AEC will result in many big investment projects positively impacting the real estate market in 2015. The construction materials started to recover since the third quarter. In addition, the government’s short-term economic stimulus measures during the last three months of 2014 will, from now until the end of 2015, have impact on the high growth of construction materials. The interior decoration equipments, and furniture will also recover in line with the construction industry.

-9-

ISSUE 3 VOLUME 15 October 2014

Investment in the Plastics Industry According to the reports of the investment approvals of the Office of the Board of Investment between January – September 2014 in chemical, paper, and plastics industries, there were in total 104 investment approved projects, up 17 projects from August, with the total registered capital of 28.1 billion baht, up from the previous month by 7 billion baht. BOI approved Projects in Chemical, Paper, and Plastics Industries Jan. – Sep. 2014

Projects

2012 Jan. – Dec. 298

2013 Jan. – Dec. 242

2013 Jan.– Sep. 210

2014 Jan. – Sep. 104

Billion baht

128.6

80.4

66.6

28.1

Unit

Number Registered capital

Source: Office of the Board of Investment, October 2014 Disclaimer Plastics Institute of Thailand prepared the Monthly Analysis of the Situations of the Plastics Industry (PITH Analysis) with the objective of presenting information and situations in the plastics industry through the process of compiling and editing various data accompanying the analysis to facilitate the readers. Plastics Institute of Thailand is not involved or has any interest with the information sources. Therefore, it reserves the right not to be responsible for any loss or damage, whether directly or indirectly, associated with or as the result of applying the information obtained from this analysis to use.

Monthly Analysis of the Situations of the Plastics Industry

Prepared by

Plastics Institute of Thailand MIDI Building 86/6 Soi Treemit, Rama IV Road, Klongtoey Sub-district, Klongtoey District, Bangkok 10110 Tel. 02 391 5340-2 Fax 02 712 3341 www.thaiplastics.org

- 10 -

ISSUE 3 VOLUME 15 October 2014