Applied Geography 22 (2002) 235–251 www.elsevier.com/locate/apgeog

European environmental taxes and charges: economic theory and policy practice Ian Bailey ∗ Department of Geographical Sciences, University of Plymouth, Drake Circus, Plymouth PL4 8AA, UK Received 29 June 2001; received in revised form 29 April 2002; accepted 27 May 2002

Abstract The environmental and economic benefits of environmental taxes and other market-based mechanisms over standards-based legislation have been strongly articulated in the economics literature. This paper examines these claims based on studies of the European Union Packaging Waste Directive. Evidence from the investigation indicates that the pollution-reducing effect of environmental taxation is severely constrained for price-inelastic commodities but that revenue hypothecation for defensive expenditures provides genuine possibilities for promoting environmental improvements whilst retaining the economic benefits of market-based regulation. The importance of empirical spatial analysis for theoretical and practical advancement is stressed and future research directions are suggested. 2002 Elsevier Science Ltd. All rights reserved. Keywords: Environmental policy; Environmental taxation; Green taxation; European legislation; Marketbased mechanisms

Environmental economists have long argued that environmental policy should be based more firmly on the use of market-based mechanisms, such as environmental taxes and tradable permits, which integrate the environmental costs of pollution clearly into the economy (Pearce, Markyanda, & Barbier, 1989; Pearce & Barbier, 2000). Their central argument is that ‘traditional’, standards-based ‘command-andcontrol’ environmental regulation is economically inefficient because it imposes uniform obligations on polluters, regardless of their ability to control environmentally damaging practices. This can appreciably increase compliance costs and industry ∗

Tel.: +44-1752-233087; fax: +44-1752-233054. E-mail address:

[email protected] (I. Bailey).

0143-6228/02/$ - see front matter 2002 Elsevier Science Ltd. All rights reserved. PII: S 0 1 4 3 - 6 2 2 8 ( 0 2 ) 0 0 0 1 1 - 5

236

I. Bailey / Applied Geography 22 (2002) 235–251

resistance to future environmental regulation of any description. Economists also consider command-and-control to be environmentally inefficient, as polluters have few incentives to reduce pollution beyond standards set by government, whereas market-based mechanisms create a constant price pressure for improvement (Pearce & Barbier, 2000). Despite the importance of environmental issues for national and international policy, geographical input into such debates has, in the main, been marginal. This is surprising, considering the extent of the economic geography research agenda and the discipline’s enduring empirical tradition, which suggests immense potential for examining the spatial, economic and environmental implications of policies seeking to promote sustainable development (Gibbs, 1996). This paper argues that greater empirical scrutiny of economic theory is vital if the innovative capacity of marketbased mechanisms is to be fully realized. It examines one policy where economic instruments have been extensively employed, the European Union (EU) Packaging Waste Directive. It assesses the practical merits of market-based mechanisms in the implementation of the Directive and, thereby, demonstrates the value of comparative analyses in furthering debates on the economic approach to environmental policy. After outlining contemporary debates on the merits of market-based mechanisms and the political background of the Directive, the use of economic instruments in Britain and Germany is examined. The strengths and weaknesses of these market-based mechanisms are then discussed and recommendations made for increasing their environmental efficiency whilst retaining the economic benefits of price-based environmental policy.

Theoretical background Although command-and-control and market-based environmental policies both create financial incentives to reduce pollution (either through the cost of complying with environmental standards or the tax itself), market-based mechanisms provide polluters with greater choice of whether to continue polluting and pay increased costs, or reduce environmentally damaging activities.1 Economic theory states that firms will choose the latter option if abatement costs are less than the price charged by the market-based mechanism (Pearce & Barbier, 2000). Either way, by allowing flexibility of response, market-based mechanisms generally promote cost-effective environmental protection. Market-based mechanisms can also be iterated more easily than command-and-control instruments to alter the relative appeal of continued pollution or abatement until socially and ecologically ‘optimum’ pollution levels are attained. By contrast, command-and-control standards – either prohibitions or requirements to use particular technologies – imposed by governments that do not 1 Market-based mechanisms in their truest sense stipulate neither environmental standards nor methods of implementation. Economic instruments may also be deployed in a ‘mixed’ system, however, whereby command-and-control mechanisms are used to specify environmental targets and economic instruments are introduced to promote implementation flexibility (Pearce & Barbier, 2000).

I. Bailey / Applied Geography 22 (2002) 235–251

237

possess intimate knowledge of each industry sector are more likely to limit options available to industry and, thereby, increase compliance costs. Whilst market-based mechanisms can be classified in numerous ways according to function or point of levy, Ekins (1999) highlights three objectives economic instruments may be designed to achieve: 앫 Incentive taxes: taxes levied purely with the intention of changing environmentally damaging behaviour by increasing the marginal cost of polluting. 앫 Cost-covering charges: where parties using particular environmental resources contribute to the cost of monitoring or mitigation. This is normally achieved by earmarking, or hypothecating, revenues for expenditures that improve the management of environmental damage caused by these activities, and 앫 Revenue-raising taxes: all environmental taxes yield revenue, which may contribute towards overall public finances or reductions in employment or product taxes. It is important to recognize that these tax objectives are not mutually exclusive, however, as cost-covering or revenue-raising charges may also produce incentive effects and vice versa. However, Ekins (1999) stresses the importance of understanding the main purpose of each environmental tax, as charges that finance environmental management projects adequately are only likely to correspond with those needed to provoke pollution deterrents by coincidence. Similarly, if an environmental tax is successful in changing behaviour, it may raise substantially less revenue than anticipated (Barde, 1997). There has been extensive discussion of market-based mechanisms in the economic literature, with Baranzini, Goldemberg and Speck (2000) and Ekins and Speck (2000) highlighting two particular concerns that have surfaced in OECD countries. The first is the potential inflationary impact of environmental taxes, which may hamper economic performance and competitiveness, particularly in sectors that rely heavily on processes or products targeted by environmental taxes. However, both theoretical and empirical studies suggest that market-based mechanisms remain the most efficient method for pursuing many environmental goals, so that countries pursuing such strategies generally perform better economically than those that rely on legislative standards (Ekins & Speck, 2000). It is nonetheless imperative that vulnerable sectors are given special consideration to avoid competitive effects, by providing selective rebates that compensate for economic impacts without diluting the incentive patterns intended by the tax. The second issue concerns the distributional impact of environmental taxes that impinge disproportionately on poorer sectors of society (Baranzini et al., 2000). Whilst requiring consideration on a case-by-case basis, regressive distributional effects can be mitigated through tax-free thresholds for essential uses, lower-income households and smaller businesses. The environmental efficacy of market-based mechanisms is also keenly contested in the literature. Beder (1996) argues that whereas legislation compels polluters to observe defined standards, financial incentives merely encourage changes in behaviour. If individuals choose to continue polluting for non-economic reasons or because conflicting incentives exist, incentive taxes may fail to fulfil their primary objective.

238

I. Bailey / Applied Geography 22 (2002) 235–251

The incentive potential of market-based mechanisms also depends on the demand price elasticity for targeted activities; consequently, several charge iterations may be necessary to secure desired abatement levels. Jones (1999) adds that because businesses, the sector most frequently targeted by environmental taxes, typically base major investment decisions on total factor costs rather than individual market-based mechanisms, the effect of incentive taxes on behaviour should not be over-stylized. As Jacobs (1991: 152) concedes, the normative economic models on which marketbased mechanisms are based often ‘fail to represent the complexities of the real world, in which “institutional” factors crucially affect corporate and consumer decision-making’. Finally, where market-based mechanisms are grafted inappropriately into ‘mixed’ systems where legislation plays a dominant role, their performance may be distorted by the wider regulatory regime (Goddard, 1995). The cost-covering functions of environmental taxes are also not universally welcomed, as excessive hypothecation may introduce rigidities into government expenditure that are unjustified in terms of public or environmental need. Conversely, hypothecation can assist public understanding of the reasons for new taxes and, where earmarking systems are separated from mainstream taxation and expenditure to ameliorate specific problems, ‘closed loops’ of environmental charges and expenditure can be created (Spackman, 1997). Excessive focus on hypothecation may also prevent environmental taxes from achieving their main objective of changing polluter behaviour, whilst, as noted earlier, reductions in pollution may induce over-capacity in pollution-control facilities and, hence, economic inefficiencies (Barde, 1997). Given these controversies, it is unsurprising that many European policy-makers were initially reluctant to experiment with policy instruments that devolved many responsibilities for environmental management from government to the market. However, their popularity has increased markedly in recent years, as it has become apparent that command-and-control standards have failed to resolve many environmental problems. The Dobris Assessment of environmental quality in Europe in 1992 graphically illustrated the extent of this failure and, in response, the European Commission sought new instruments to promote the sustainability ambitions of the Fifth EU Environmental Action Programme (1993–2000): In order to create market based incentives for environmentally friendly economic behaviour the use of economic and fiscal instruments would have to constitute an increasingly important part of the overall approach. (Commission of the European Communities, 1992) Environmental taxes and other market-based mechanisms have subsequently become integral to environmental policy in many member states, tackling such diverse problems as waste management, climate change, fuel technology and water pollution (European Environment Agency, 2000). Several states have also established far-reaching ecological tax reform commissions to promote an overall shift of taxation from economic ‘goods’, such as employment, towards environmental degradation. However, rather than relying entirely on the pollution-reducing potential of market-based mechanisms, most governments have opted for mixed systems of legis-

I. Bailey / Applied Geography 22 (2002) 235–251

239

lation and economic instruments that stipulate clear environmental standards whilst still promoting cost-effective implementation through market-based mechanisms. In summary, although the economic theory of market-based mechanisms has been robustly defended, many issues still require further investigation to improve practical understanding of factors influencing their environmental and economic effectiveness. This is particularly true since many market-based mechanisms have only been deployed relatively recently and, therefore, their practical implications are only beginning to become apparent. This paper focuses primarily on the environmental benefits of economic instruments but also briefly considers economic impacts. It is also restricted to incentive taxes and cost-covering charges, as revenue-raising taxes are not central to the main focus on the environmental performance of marketbased mechanisms. Linking into current political and theoretical debates, therefore, the paper addresses the following issues. First, it assesses the circumstances under which market-based mechanisms are capable of curbing demand for environmentally damaging activities. Second, it examines conditions determining where market-based mechanisms yield more cost-effective results than standards-based command-and-control techniques and how competitive and distributional effects can be mitigated. Third, it reviews the potential applications of hypothecation to improve environmental protection in situations where incentives prove difficult or costly to generate. It does this with reference to one specific policy instrument – the EU Packaging Waste Directive. The discussion thus proceeds by outlining the regulatory context of the Directive and its implementation in selected member states, and then examines the reaction of businesses to economic instruments and the role of hypothecation.

Policy context: the Packaging Waste Directive The EU formally adopted the Packaging Directive in December 1994 with the aim of approximating member-state laws governing the management of packaging waste. Following the introduction of the German Verpackungsverordnung (Packaging Ordinance) in 1991, the European Commission feared that disparate national packaging laws would create technical obstacles to EU trade and sought harmonizing legislation aimed … as a first priority, at preventing the production of packaging waste and, as additional fundamental principles, at reusing packaging, at recycling and other forms of recovering packaging waste and, hence, at reducing the final disposal of such waste. (Article 1) (Official Journal of the European Communities, 1994: 12)2 Following protracted and acrimonious negotiations, only two targets were actually

2 Recovery denotes the recouping of value from packaging waste, including composting, combustion with energy recovery, and recycling.

240

I. Bailey / Applied Geography 22 (2002) 235–251

quantified, the recovery of 50–65% and recycling of 15–45% of packaging waste produced in each member state – both to be achieved by June 2001. The prevention and re-use objectives were instead downgraded to unquantified ‘Essential Requirements’ (Annex II), as it was felt that defined standards in these areas would excessively constrain European industrial competitiveness on international markets. Although the Directive only introduced legislative standards, the Council adopted economic instruments to promote its implementation (Article 15). It is therefore apparent that most member states anticipated implementing its requirements using some combination of command-and-control standards and economic instruments. The implementation case studies examined here – those of Germany and Britain – are particularly pertinent to the aims of this paper, in that the two governments have adopted contrasting approaches to the design of economic instruments. They therefore illustrate the extent to which such variations can alter both the economic and environmental outcomes achieved by price-based methods of environmental regulation. The British model According to the consultation paper circulated prior to the Producer Responsibility Obligations (Packaging Waste) Regulations 1997 (the Regulations), the British government was committed to implementing the Directive in the least burdensome manner to industry (Department of the Environment, 1996). Consequently, the targets set by the Regulations in 1997 were towards the minimum allowed by the Directive, 52% recovery and 16% recycling per material. Although the Department of the Environment, Transport and the Regions (1999) revised these to 56% and 18% in 1999, the government’s aim remained the achievement of the Directive’s minimum requirements. In order to reduce distributional and competitive impacts, responsibilities are shared amongst all sectors of the packaging chain according to their contribution to waste production and the economic impact of recycling and recovery (Table 1). The Regulations also exempt small businesses (those with an annual turnover below £2 million or handling less than 50 t of packaging) from direct recovery obligations. Finally, specialist compliance schemes were established to help businesses manage their recycling responsibilities, thereby further easing the implementation burden (for more detailed analysis, see Bailey, 1999). Whilst mandatory standards provide the mainstay of the Regulations, market-based mechanisms have become critical to policy implementation. To prove compliance with the Regulations, producers or schemes must submit evidence annually to the Environment Agency or its regional equivalents. The standard form of evidence is certificates, termed packaging recovery notes (PRNs), produced by accredited reprocessors as they recycle or incinerate waste collected from industrial or household sources. Under the scheme, reprocessors are entitled to charge producers for supplying PRNs, with prices determined by the weight of packaging reprocessed and prevailing conditions in each material market. The PRN scheme operates primarily as a cost-covering charge to generate funds for investment in new recycling infrastructure but, at the same time, producers can reduce their costs by consuming less, or

I. Bailey / Applied Geography 22 (2002) 235–251

241

Table 1 UK recycling targets, cost assessment and producer responsibilities Activity

Annual turnover Compliance Cost as % of (£millions) costs (£millions) turnover

Sector responsibilities (%)a

Raw materials Converter Packer-filler Retailer Total

8200 8500 112 800 123 500 253 000

6 9 37 48 100

33 77 244 278 632

0.4 0.9 0.2 0.2 0.3

Source: data supplied by the Packaging Federation. a Expressed as a percentage of packaging consumed by each sector, measured by weight. To meet its sector recovery target, a retailer, for example, must recover packaging waste according to the following algorithm: 56% recovery target × 48% sector obligation = 26.9% total packing consumption. Prior to 1999, converters attracted an 11% sector obligation, which increased the sector’s costs to 1.1% of turnover. This was renegotiated in 1999 to spread the economic burden more evenly, with 2% of the converter obligation being shared between packer-fillers and retailers.

re-using, packaging. In theory, therefore, PRNs also create financial incentives for reduced packaging-waste production. The economic efficiency of the PRN market is maintained, according to government thinking, by competition between reprocessors seeking to access PRN revenue, a precept adopted for many other market-based mechanisms (currently reprocessors 225 are licensed by the Environment Agency to participate in the scheme). The German model The Verpackungsverordnung of 1991 (amended in 1998) makes all manufacturers and distributors in Germany responsible for re-using and recycling their packaging waste outside the public waste disposal system, and requires retailers to set up instore facilities for collecting used packaging (Umweltsbundessamt, 1991). Unlike the British model, there are no detailed provisions for reducing distributional and competitive impacts for small businesses. Furthermore, the legislation concentrates legal obligations on fewer sectors, with the expectation that its effects will filter through to other sectors through supply-chain pressures. However, these obligations are waived for companies joining an industry-led ‘Dual System’ for collecting, sorting and recycling used packaging. In contrast with the British competitive model, the Dual System Deutschland (DSD) co-ordinates all sales packaging collection in Germany, and the activities of the entire packaging chain, to achieve national recycling targets, which are set towards the maximum stipulated in the Directive (Bailey, 1999). Again, economic instruments are essential to policy implementation in Germany, though there is little evidence of a market-based approach. The DSD’s operations are financed by licence agreements with companies, with fees paid on each unit of packaged product, based on packaging material, weight, area and volume. The fees

242

I. Bailey / Applied Geography 22 (2002) 235–251

entitle manufacturers to mark their packaging with the DSD’s Green Dot logo to identify it to consumers as participating in the scheme (Dual System Deutschland, 1998). These provisions only apply to sales packaging; separate arrangements must be made by businesses for transport and other packaging. In contrast to the ‘marketpricing’ model, Green Dot fees are calculated by the DSD using life-cycle assessments for each packaging material and are, on average, ten times higher than PRN prices. Again the scheme’s principal purpose is to fund recycling; though, as in Britain, it is the only policy instrument in Germany to encourage waste prevention directly (Eichsta¨ dt, Carius, & Kraemer, 1999). Instead of competition between reprocessors, materials organizations were founded to act as the DSD’s guarantors by producing global recycling certificates (the Mass Flow Verification) and raising finance for reprocessing. The fundamental orientation of the system, therefore, is towards inter-sectoral co-ordination and economic instruments that prioritize compliance with challenging environmental targets before cost-effective implementation.

Assessing the impact of economic instruments: national indicators A first indication of the effects of the British and German regulations and economic instruments comes from national data on packaging entering the waste stream. The DSD reported that per capita packaging consumption in Germany fell by 13.4% between 1991 and 1998 (Dual System Deutschland, 1998). However, projections for Britain show sizeable variations between different packaging materials, with an overall increase in waste generation between 1998 and 2001 (Table 2). Whilst this suggests that higher packaging charges in Germany may have contributed towards reduced packaging consumption, it would be unwise to overstate the incentive effect of the Green Dot system from this information. First, the DSD only collects sales packaging and the German environment ministry does not publish figures for secondary and transport packaging. Numerous German companies have, in fact, begun subTable 2 Predicted and actual growth in UK packaging (103 t) Material

1998

2000

2001 (estimate)

Paper Glass Aluminium Steel Plastics Total excluding wood and other Wood Other Total

2946 1859 109 735 1317 6966 728 17 7711

3855 2155 110 750 1600 8470 670 40 9180

3855 2200 120 750 1679 8604 670 40 9314

Source: Department of the Environment, Transport and the Regions (2001: 10–11); Department for Environment, Food and Rural Affairs (2001: 5).

I. Bailey / Applied Geography 22 (2002) 235–251

243

stituting sales packaging with transport packaging because the latter can be more readily recovered (Perchards, 1998). In some cases, this has increased overall waste arisings whilst nonetheless facilitating individual corporate compliance. Moreover, both governments deployed numerous regulatory tools to combat packaging waste, including economic instruments, legal targets, and the Directive’s ‘Essential Requirements’ concerning packaging design. Further testing is therefore required at the level of the individual firm to isolate the effects of economic instruments from those produced by other instruments.

Corporate perceptions of economic instruments To explore the relationship between economic instruments and packaging consumption further, surveys were conducted with British and German firms affected by national regulations. The aim was to identify whether these companies felt economic instruments had encouraged significant changes in corporate waste management by measuring four primary variables: 앫 whether companies affected by national packaging policies had instigated defined waste-management plans; 앫 types of waste management adopted, including waste reduction, re-use, collection for reprocessing, and the amount of recycled packaging used by companies; 앫 waste-management targets set in relation these objectives, measured as a percentage of total business packaging consumption, and 앫 Green Dot or PRN charges incurred. Two omissions from these objectives require justification. First, although the waste-management options examined all relate to key objectives of the Packaging Directive, it proved impossible to quantify respondents’ compliance with statutory recovery and recycling targets. Pilot studies showed that companies were not prepared to divulge such sensitive information, even with reassurances of anonymity. Second, only direct compliance costs (PRN or Green Dot charges) were considered. Indirect compliance costs, such as data collection, staff training, modifications to information technology, and consultancy fees, were omitted because they tend to be business specific and, therefore, could not be reliably compared. Additionally, although indirect costs may contribute significantly to compliance costs, they stem principally from legal obligations rather than economic instruments per se, and are therefore peripheral to the analysis. Finally, many companies do not monitor indirect costs and, consequently, data of this type were likely to be unreliable. Using stratified random sampling from registers provided by the Environment Agency and German corporate directories, 900 businesses from each country were surveyed. Replies were received from 469 British (52.1% response) and 309 German companies (34.3% response). Filter questions were used to eliminate businesses not affected by national packaging regulations: this reduced the useful responses to 450 (50%) for the UK and 236 (26.2%) for Germany. Data concerning company turnover

244

I. Bailey / Applied Geography 22 (2002) 235–251

and sector were also obtained to establish whether responses were significantly affected by particular corporate characteristics. However, these influences were found to be negligible and are therefore not reported in this paper. Corporate waste management The first element of the surveys identified the percentage of British and German firms that had established strategies to promote each form of waste management examined (Table 3). For all indicators, the number of German companies with defined waste management plans far exceeded those in Britain. This was especially pronounced for waste prevention, with 57.1% of German respondents having instituted waste-prevention plans compared with only 12.7% of British firms. There was less discrepancy in re-use strategies, despite the re-use provisions of the Packaging Directive, because of the inclusion of wooden pallets in the UK Regulations. In fact, wood was by far the most commonly re-used packaging material reported by British respondents. The greatest similarities between British and German firms were observed for waste collection, where most respondents routinely collect waste arising at company sites, because large quantities of readily recoverable materials are available, but avoid reclaiming packaging from customers, since this involves significantly higher collection costs. However, the mere fact that firms have introduced waste management plans provides little indication of the scale of their involvement. For example, businesses collecting a small percentage of office paper cannot be equated with those reclaiming large volumes of residual materials from production or transport processes. The extent of corporate waste management was assessed by measuring targets set as a percentage of total packaging consumption for 1998 and predicted performance in 2001 (Table 4). These data again indicate German businesses as having generally set more ambitious objectives than their British counterparts. For example, the mean waste reduction target amongst British respondents between 1998 and 2001 was 2%, compared with over 10% for German firms. Whilst there are indications that British Table 3 Waste management actions: British and German companies Action

Reduction in consumption Re-use Collection from business premises Collection from customers Purchase of recycled packaging Note: n = 450 (UK), 236 (Germany).

Firms engaged in waste management activities (%) UK

Germany

12.7 23.8 64.5 13.4 24.5

57.1 52.4 85.4 18.4 53.2

I. Bailey / Applied Geography 22 (2002) 235–251

245

Table 4 Waste management performance and targets Target

Period

Mean target (% of packaging consumption) UK

Reduction Re-use Collection Purchase recycled

1998–2001 1998 2001 1998 2001 1998 2001

2.0 10.5 15.8 21.1 27.5 14.4 20.5

Germany 10.8 24.3 32.1 40.3 45.6 37.2 47.4

industry should secure greater relative improvements over the period (chiefly because recycling is expanding rapidly from a low starting point, whilst recycling networks were well developed in Germany and further expansion might be constrained by diminishing returns) the general impression remains that recycling in Britain will lag behind that in Germany for the foreseeable future. Economic instruments and packaging waste management Clarifying the precise link between environmental taxes and business behaviour is extremely difficult since, as noted previously, economic instruments are rarely deployed without accompanying legislation and other policy devices. Furthermore, as businesses must consider numerous endogenous and exogenous pressures when responding to environmental policies, including the prospect of imperfect enforcement by government agencies, it is often impossible to discern the exact relationship between economic instruments and polluter behaviour (Jones, 1999). Recognizing these difficulties and the implied restrictions on data interpretation, each corporate waste management target was correlated against respondents’ Green Dot or PRN costs. To reduce discrepancies caused by varying business size and intensity of packaging use, correlations were performed against environmental charges calculated as a proportion of company turnover and packaging consumption. Even following these modifications, this method provides, at best, a crude evaluation of the link between economic instruments and business behaviour, and few economists would claim the relationship is this straightforward, especially where economic instruments are not employed primarily for incentive purposes. The working hypotheses were, therefore, that 1. the relationship between environmental charges and waste management would not be strong in either country, but 2. the relationship would be greater in Germany because Green Dot charges are substantially higher than PRN costs.

246

I. Bailey / Applied Geography 22 (2002) 235–251

Table 5 Waste management targets and environmental charge costs Target

Collection Reduction 1998–2001 Re-use 1998 Re-use 2001 Buy recycled 1998 Buy recycled 2001 Index of combined targets ∗

Germany

UK

Spearman correlation

One-tail significance

Spearman correlation

One-tail significance

0.215 0.014 0.107 0.014 0.101 0.077 0.023

0.021∗ 0.446 0.154 0.448 0.173 0.244 0.403

0.098 0.043 0.049 0.018 0.013 0.039 0.033

0.049∗ 0.214 0.206 0.388 0.416 0.271 0.270

Significant at 95% confidence level.

The results partly corroborated these hypotheses but less clearly than anticipated (Table 5). Although there were stronger correlations between recycling charges and actions in Germany for some measures, these differences were fairly superficial, whilst statistically significant (but weak) correlations were only observed for waste collection. This suggests that economic instruments per se have not encouraged major changes in corporate waste management in either country, despite higher German recycling charges. Consequently, it would appear that the reductions in packaging consumption highlighted by national data stem mainly from other regulatory pressures, particularly legislative targets or indirect compliance costs. Equally, whilst both schemes were designed principally as cost-covering rather than incentive charges, this does not explain why major variations in packaging waste charges failed to alter waste management practices at the business level.

The relationship between environmental charges and business behaviour The obvious explanation for the lack of relationship between economic instruments and business waste management is that the costs imposed on industry by these charges are insufficient to encourage changes in behaviour beyond those prescribed by legislation. In both cases, the ‘optimum’ cost-covering charges to finance collection and reprocessing appear to be significantly lower than those required for a discernible pollution-reducing incentive. Economic theory suggests that the optimum rate of incentive taxes occurs when the marginal cost of further increases in pollution (in this case, packaging waste) equals the marginal private benefit gained from this activity. In fact, this point would be difficult to define with recycling charges, since the value of packaged products clearly exceeds the tax rate, which is only levied on the packaging waste produced (Pearce & Turner, 1992). Any incentive effect is therefore likely to be minor. Furthermore, packaging has become an increasingly essential commodity for firms seeking to market their products and rationalize logistics net-

I. Bailey / Applied Geography 22 (2002) 235–251

247

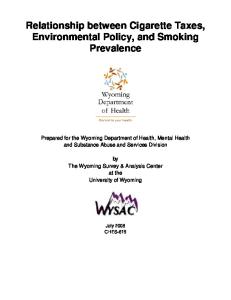

works. The price elasticity of packaging has accordingly diminished, such that even major iterations in market-based mechanisms appear to prompt negligible reductions in demand. In such instances, attempts to induce abatement incentives could probably prove counterproductive by precipitating inflationary pressures, and competitive effects between sectors and member states. There are numerous examples where even punitive economic instruments have failed to restrict demand for price-inelastic commodities (Beder, 1996; Pearce & Barbier, 2000). For instance, the British government introduced a fuel duty escalator in 1993 to discourage road traffic on environmental grounds; this was initially set at 3% above annual inflation and increased to 5% in 1997. By the time the escalator was abandoned in 2000, taxes (serving both revenue-raising and incentive functions) comprised 81.5% of total fuel prices, prompting blockades of oil refineries by haulage firms (British Broadcasting Corporation, 2000). In this example, the cost of an exceptionally price-inelastic ‘essential’ product became unacceptable before appreciable reductions in demand were induced. In addition to highlighting how high environmental taxes do not always stimulate abatement, the case also suggests that the availability of alternatives (in the fuel case, affordable and convenient public transport) is critical in determining the incentive impact of environmental taxes. Though the example of packaging waste is less extreme, logistics and marketing considerations do impose comparable constraints on the abatement options available to firms operating national and international supply chains. One method for overcoming this obstacle is to hypothecate environmental charges to stimulate technological innovation or capacity-building (Carraro, 2001). Indeed, both the British and German governments have used economic instruments to this effect. Of the DSD’s income of DM4.0 billion in 2000, 88.9% was spent purchasing waste management services, enabling an increase in household and small business recycling from 12.5 to 84% between 1992 and 2000 (Dual System Deutschland, 2000) (Fig. 1). In the UK, approximately £60.4 million of PRN revenue was made

Fig. 1.

Packaging recovery rates in Germany and the UK.

248

I. Bailey / Applied Geography 22 (2002) 235–251

available to reprocessors in 2000, though only a proportion has actually been earmarked for infrastructure development (Advisory Committee on Packaging, 1998). This has encouraged packaging recovery to rise from 33 to 42% between 1998 and 2000, though compliance with the Directive’s recovery target may not be achieved until 2002/3 (Department for Environment, Food and Rural Affairs, 2001). Both hypothecation schemes have experienced significant problems, however, which again highlight noteworthy strengths and weaknesses of command-and-control and market-based instruments. Although the DSD has achieved high recycling rates, it has consistently been the most expensive recycling system in Europe, both in relative and absolute terms (Commission of the European Communities, 2000). This has been caused in part by the DSD’s decision to fund costly kerbside collection to achieve the high recycling rates demanded by the Ordinance. Prohibitive Green Dot fees have also encouraged free riding (companies using the logo without paying licence fees), which has further increased costs to DSD members (Perchards, 1998). Finally, despite incremental increases in efficiencies, the DSD’s de facto monopoly has hindered competition in the collection and reprocessing markets. Indeed, contractors’ awareness that the DSD is under continual pressure to meet government targets has encouraged the over-pricing of recycling services. By contrast, competition between reprocessors in Britain has increased recycling capacity at lower relative cost, but investment in new recycling infrastructure has emerged more slowly than envisaged. The principal reason for this was the British government’s failure to introduce adequate controls from the outset of the Regulations by stipulating how reprocessors should spend PRN proceeds. Consequently, many reprocessors simply saw PRNs as a windfall profit (Bailey, 1999). Investment in collection suffered particularly badly, forcing the government to introduce new reporting requirements and instruct the Environment Agency to de-register reprocessors that failed to comply with the spirit of the scheme. A trade-off therefore appears to have emerged between the economic efficiency of cost-covering charges and the environmental standards achieved by government policy. The DSD remains extremely expensive but has achieved the maximum recycling rates expected by the EU, whereas the PRN scheme has promoted cost-effective recycling but struggled to meet EU environmental objectives because of an initial failure to control the details of revenue hypothecation. Overall, however, Britain’s market-led approach to hypothecation appears to offer greater long-term benefits over the command-and-control approach, as packaging recovery is increasing at lower relative cost to industry. In cases where environmental charges fail to induce reduced demand for environmentally damaging products and processes, therefore, marketbased hypothecation offers considerable potential for economically efficient improvements in environmental protection, provided adequate regulatory checks are incorporated into policy design. Conclusions What are the broader lessons for market-based mechanisms derived from this study? They have become an increasingly important feature of environmental policy

I. Bailey / Applied Geography 22 (2002) 235–251

249

in recent years, as governments have sought innovative methods for integrating environmental costs into market prices and decisions. By the same token, translating economic theory into practice is a complex process, involving significant trial and error. Examination of the operation of policies such as the Packaging Waste Directive can provide important lessons for environmental taxation to augment theories developed by more abstract disciplines. Whilst geographical input into such debates has not, thus far, been extensive, the call for empirical studies is likely to intensify as governments seek guidance on practical applications for market-based mechanisms and their transfer between different spheres of environmental policy. The study has, first, reaffirmed the importance of market-based mechanisms for environmental policy. Although increased recycling in Britain and Germany cannot be attributed directly to economic instruments – in both countries, command-andcontrol standards provided the main policy momentum – they have increased industry awareness of waste issues and facilitated investment in recycling infrastructure. However, the study has also highlighted the extent to which incentive market-based mechanisms are constrained by demand price inelasticity. Although, this issue has been documented in the economics literature (Pearce & Barbier, 2000), the Green Dot’s failure to reduce packaging consumption despite imposing punitive charges implies that demand for price-inelastic products can resist even major iterations in marketbased mechanisms. Moreover, where economic instruments target a single component of broader ‘pollution chains’, in this case, the packaging element of products, their impact on demand and abatement options remains minimal, unless economically damaging charges are applied. In which case, the negative distributive and inflationary impacts of market-based mechanisms may intensify and, in a European context, distortions in competition may also arise. Nonetheless, mixed systems of economic instruments and legislative standards can expedite desired environmental objectives whilst still promoting cost-effective implementation. As the PRN scheme has demonstrated, judicious regulation can also reduce the distributional and competitive impacts of market-based mechanisms by ensuring industry responsibilities are apportioned equitably and the needs of smaller businesses are catered for. Where incentive taxes prove environmentally ineffective or economically damaging because of price-elasticity factors, cost-covering charges can still supplement regulatory standards by encouraging investment in pollution abatement. Environmental hypothecation has, in fact, gained increased currency in recent years. The Landfill Tax Credit Scheme, for example, uses revenue from disposal charges to finance research examining the environmental impacts of landfill sites. Similarly, the British and German governments have begun earmarking a proportion of new taxes on fossil-fuel energy to subsidize renewable energy production. As with the Green Dot and PRN schemes, these policies have addressed the criticism that hypothecation introduces excessive fiscal rigidity by adopting ‘closed-loop’ systems, drawing expenditure entirely from particular environmental levies without impacting on ‘mainstream’ spending commitments. The study has also underlined the economic benefits of market-based environmental charges. Whilst recycling in Germany has undoubtedly benefited from high Green Dot charges and the co-ordinating powers of the DSD, the absence of competitive

250

I. Bailey / Applied Geography 22 (2002) 235–251

pressures in the system has exacerbated economic inefficiencies. By contrast, Britain has increased recycling at significantly lower relative cost by adopting market-based pricing. Despite these economic benefits, the British and German schemes have both adopted largely end-of-pipe approaches to hypothecation, which rely on packaging waste being produced to raise funds. There is therefore a case for more preventative hypothecation that addresses profligate demand for packaging production rather than focusing predominantly on remediation. Whilst this would undoubtedly reduce the funds available for investment in recycling, it offers more sustainable long-term solutions to waste management problems. Despite evidence that energy taxes in Britain and Germany are being used to reduce long-term reliance on fossil fuels, preventative hypothecation generally remains an under-utilized policy option, which warrants further theoretical and empirical investigation. By developing similar methodologies to those proposed in this paper, geographers can play a pivotal role in contemporary environmental policy debates.

Acknowledgements The author would like to thank Mark Cleary, Andrew Jordan, Jon Shaw and the anonymous referees for their insightful comments on earlier versions of this paper. Thanks also to the Cartographic Resources Unit at the Department of Geographical Sciences, University of Plymouth and to the Institute of Wastes Management, which generously sponsored this research. Responsibility for any remaining errors and omissions rests entirely with the author.

References Advisory Committee on Packaging (1998). Report on review of the Producer Responsibility Obligations (Packaging Waste) Regulations. London: ACP. Bailey, I. G. (1999). Flexibility, harmonization and the Single Market in European Union environmental policy: evidence from the Packaging Waste Directive. Journal of Common Market Studies, 37, 549–572. Baranzini, A., Goldemberg, J., & Speck, S. (2000). A future for carbon taxes. Ecological Economics, 32, 395–412. Barde, J.-P. (1997). Environmental taxation: experience in OECD countries. In T. O’Riordan (Ed.), Ecotaxation (pp. 223–245). London: Earthscan. Beder, S. (1996). Charging the Earth: the promotion of price-based measures for pollution control. Ecological Economics, 16, 51–63. British Broadcasting Corporation (2000). UK fuel tax: the facts. http://news.bbc.co.uk/ hi/english/in depth/world/2000/world fuel crisis/newsid 933000/933648. Carraro, C. (2001). Environmental technological innovation and diffusion. In H. Folmer, H. L. Gabel, S. Gerking, & A. Rose (Eds.), Frontiers in environmental economics (pp. 342–370). Cheltenham: Edward Elgar. Commission of the European Communities (1992). A Community programme of policy and action in relation to the environment and sustainable development. Brussels: CEC (COM(92)23 final). Commission of the European Communities (2000). Cost-efficiency of packaging recovery systems: the case of France, Germany, the Netherlands and the United Kingdom. Brussels: Taylor Nelson Sofres.

I. Bailey / Applied Geography 22 (2002) 235–251

251

Department of the Environment (1996). The Producer Responsibility Obligations (Packaging Waste) Regulations: a consultation paper. London: HMSO. Department for Environment, Food and Rural Affairs (2001). Consultation paper on recovery and recycling targets for packaging waste 2002. London: HMSO. Department of the Environment, Transport and the Regions (1999). Increasing recovery and recycling of packaging waste in the United Kingdom – the challenge ahead: a forward look for planning purposes. London: HMSO. Dual System Deutschland (1998). Packaging recycling: techniques and trends. Bonn: DSD. Dual System Deutschland (2000). Packaging recycling: sorting, processing, recycling. Bonn: DSD. Eichsta¨ dt, T., Carius, A., & Kraemer, R. A. (1999). Producer responsibility within policy networks: the case of German packaging policy. Journal of Environmental Planning and Policy, 1, 133–153. Ekins, P. (1999). European environmental taxes and charges: recent experience, issues and trends. Ecological Economics, 31, 39–62. Ekins, P., & Speck, S. (2000). Proposals of environmental fiscal reforms and the obstacles to their implementation. Journal of Environmental Policy and Planning, 2, 93–114. European Environment Agency (2000). Environmental taxes: recent developments in tools for integration. Copenhagen: European Environment Agency. Gibbs, D. (1996). Integrating sustainable development and economic restructuring: a role for regulation theory? Geoforum, 27, 1–10. Goddard, H. C. (1995). The benefits and costs of alternative solid waste management policies. Resources, Conservation and Recycling, 13, 183–213. Jacobs, M. (1991). The green economy. London: Pluto. Jones, E. (1999). Competitive and sustainable growth: logic and inconsistency. Journal of European Public Policy, 6, 359–375. Official Journal of the European Communities (1994). European Parliament and Council Directive 94/62/EC of 20 December 1994 on packaging and packaging waste. L 365/10–23. Pearce, D., & Barbier, E. (2000). Blueprint for a sustainable economy. London: Earthscan. Pearce, D., & Turner, R. K. (1992). Packaging waste and the polluter pays principle: a taxation solution. Journal of Environmental Planning and Management, 35, 5–15. Pearce, D., Markyanda, A., & Barbier, E. (1989). Blueprint for a green economy. London: Earthscan. Perchards (1998). Packaging legislation in Europe. St Albans: Perchards. Spackman, M. (1997). Hypothecation: a view from the Treasury. In T. O’Riordan (Ed.), Ecotaxation (pp. 45–51). London: Earthscan. Umweltbundessamt (1991). Ordinance on the Avoidance of Packaging Waste of 12 June 1991. Bonn: Umweltbundessamt (in German).